IMPORTANCE OF EQUIVALENT PRODUCTION IN VALUING WORK IN PROGRESS

EQUIVALENT PRODUCTION

Equivalent Production represents the production of a process in terms of completed units. In other words, it means converting the incomplete production units into its equivalent of complete units. In each process an estimate is made of the percentage completion of any work-in-progress. A production schedule and a cost schedule will then be prepared. The work-in-progress is inspected and an estimate is made of the degree of completion, usually on a percentage basis. It is most important that this estimate is as accurate as possible because a mistake at this stage would affects the stock valuation used in the preparation of final accounts. The formula for equivalent production is:

Equivalent units of work-in-progress = Actual no. of units in process of manufacture x Percentage of work completed

For example: If 20% work has been done on the average of 1,000 units still in process, then 1,000 such units will be equal to 200 completed units. The cost of work-in-progress will be equal to 200 completed units.

IMPORTANCE OF EQUIVALENT PRODUCTION IN VALUING WORK IN PROGRESS

Equivalent production is a concept used in managerial costing to measure the value of work in progress (WIP) in a production process. It is important because it allows for a more accurate valuation of WIP inventory and helps in making informed decisions about production efficiency, cost control, and pricing.

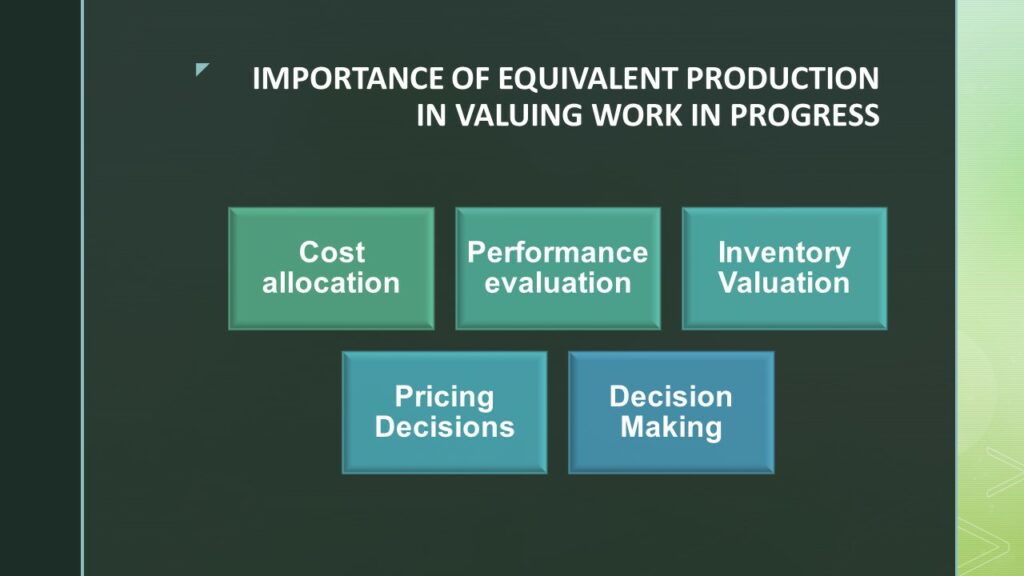

Here are some key reasons why equivalent production is important in valuing work in progress:

- Cost allocation: In a multi-step production process, it is often challenging to assign costs accurately to partially completed units. Equivalent production helps in allocating costs based on the proportion of completion, ensuring that costs are allocated to WIP inventory in a more accurate and meaningful manner. This leads to a more reliable valuation of WIP and enhances the accuracy of cost reports and financial statements.

- Performance evaluation: Equivalent production enables companies to assess their production efficiency and compare actual output to the ideal or standard output. By measuring the equivalent units produced, managers can evaluate how effectively the production process is converting raw materials into finished goods. This information is crucial for identifying inefficiencies, bottlenecks, and areas for improvement, ultimately leading to better decision-making and cost management.

- Inventory valuation: Accurate valuation of WIP inventory is essential for financial reporting and determining the true value of a company’s assets. Equivalent production provides a basis for valuing partially completed units based on the degree of completion. By valuing WIP accurately, companies can present a more realistic financial position and ensure compliance with accounting standards.

- Pricing decisions: Equivalent production plays a role in pricing decisions, especially in industries where WIP inventory is significant. When determining the selling price of a product, companies need to consider the cost of production, including the cost allocated to WIP. Equivalent production helps to calculate the total cost per unit more accurately, enabling companies to set competitive prices that cover both direct costs and allocated overheads, ultimately supporting profitability.

- Decision-making: Equivalent production information is valuable for managerial decision-making. It provides insights into the progress of production, the amount of inventory on hand, and the overall efficiency of the production process. Managers can use this information to make decisions regarding production schedules, resource allocation, capacity planning, and optimizing production costs.

In summary, equivalent production is important in valuing work in progress as it facilitates accurate cost allocation, performance evaluation, inventory valuation, pricing decisions, and overall decision-making. By considering the degree of completion of partially completed units, companies can better understand their production process, optimize resource allocation, and make informed business decisions.