MATERIAL CONTROL IN COST ACCOUNTING PDF

Material control is a system which ensures the provision of the required quantity of materials of the required quality at the required time with the minimum amount of capital investment. It can be defined as safeguarding of company’s property in the form of inventory and maintaining it at the optimum level, considering the operating requirements and financial resources of the business.

Material control is facilitated through maintaining periodical reports and records relating to purchasing, receiving, inspecting and issuing of direct and indirect materials.

NEED/ NECESSITY/ OBJECTIVES OF MATERIAL CONTROL

The main objectives of material control are as follows:

1.ENSURING UN-INTERRUPTED PRODUCTION

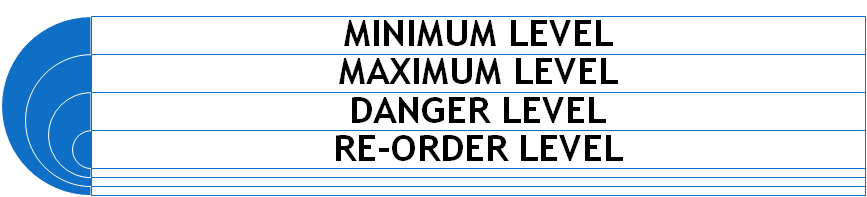

The main objective of the material control is to ensure the un-interrupted supply of materials for smooth flow of production. Material control helps in making available the right type of materials at right time. For this purpose, various material levels are set up such as:

- Maximum level

- Minimum level

- Re-order level

- Danger level, etc.

The setting up the materials levels and following them ensures the availability of materials at all the time and non-stoppage of production process.

2.PROVISION OF REQUIRED QUALITY OF MATERIALS

Material control is also associated with acquiring the quality material for production process. The material control department ensures the supply of quality material from the supplier which is to be used in the production process. As if the quality of material is not proper, it will ultimately affect the goodwill of the concern.

3.MINIMISATION OF WASTAGES AND LOSSES OF MATERIALS

Materials constitute the major source of cost to the enterprise. Material control system is being installed in the enterprise to ensure its minimal loss and wastages. For this purpose, various techniques are used such as:

- ABC analysis (Always Better Control)

- VED analysis (Vital Essential Desirable)

ABC analysis is used to classify the materials on the basis of its importance and then applying the required degree of control.

VED analysis categorize all the material of the business concern into three categories i.e. vital, essential and desirable and on the basis of this, the control is exercised on materials.

The minimization of losses and wastages of materials ultimately leads to cost reduction and cost control.

4.CONTROL INVESTMENT IN STOCK OF MATERIALS

Material control system ensures no under-investment or over-investment in stock keeping. The main aim is to make available only that amount of raw materials which are needed. There should be no holding of idle stock. This may lead to lock up of large amount of capital. Efficient material control system aims at keeping the optimum level of stock at all the times. This may be done by using the techniques like:

- Economic Order Quantity

- Material Levels

- Perpetual Inventory System

5.AIMS AT FIXING THE RESPONSIBILITY

In a materials control system, the personnel is required to perform the duties of keeping the records regarding materials receipt, issue, inspection etc. the material control system aims at fixing the responsibility of operating units and individuals connected with the handling of the materials.

6.TO KEEP THE RECORDS

Material control system ensures the proper record keeping of the materials purchased, stored, issued and received. This can be made possible by adopting the perpetual inventory system. For keeping the records, following systems are used:

- Bin Card

- Stores Ledger

TECHNIQUES OF MATERIAL CONTROL

The following are the main techniques of material control:

1.MATERIAL LEVELS

This technique is applied to maintain the various levels of stock to ensure that there is neither over-stocking nor under-stocking of materials. The various levels are set by taking into consideration the following points:

- Time involved in procurement or placing the order.

- Availability of floor space

- Quantity and types of materials used

- Consumption of materials per year in the factory.

- Minimum quantity of materials which can be advantageously purchased, etc.

The following are the various levels set:

MINIMUM LEVEL: It is the level that describes the minimum amount of stock which must be kept in the store all the times. This level acts as safety measure, which is why it is known as ‘buffer stock’ or ‘safety stock’. The fall in stock of the material below this level acts as a warning to the management to procure the materials as soon as possible, otherwise the production process will be stopped. The minimum level must be set up by taking into consideration the following things:

- Average rate of consumption of materials

- Re-order level

- Time required to obtain fresh supplies

- Production requirements as to materials.

The minimum level can be calculated as follows:

Minimum Level= Re-order level- (Normal Consumption*Normal Delivery Time)

Example: Suppose the normal consumption is 300 units per week, normal delivery time is 7 weeks, and re-order level is 2,400 units in a company. The minimum level will be calculated as:

Minimum Level= Re-order level- (Normal Consumption*Normal Delivery Time)

=2,400- (300*7)

= 2,400-2,100

=300 units.

MAXIMUM LEVEL: It is the highest level of stock that should be available with the company. The stocking of materials above this point indicates the locking up of capital and overstocking of materials in the concern. This level should be set by taking into consideration the following points:

- Normal consumption rate of material

- Time required to obtain new supplies

- Amount of working capital available.

- Availability of storage space

- Economic order quantity

- Cost of carrying inventory or cost of storage

- Seasonal considerations etc.

The maximum level can be calculated as follows:

Maximum Stock Level= Re-order level+ Re-order Quantity- (Minimum Consumption*Minimum time required for delivery)

It can also be calculated by using the following formula:

Maximum Level= Re-order level- Consumption during the time required to get supplies at minimum rate* Economic Order Size

Example: Suppose the re-order level is 54,000 units and re-order quantity is 36,000 units. The minimum consumption per week is 3,000 units and minimum re-order time is 4 weeks. The maximum stock level can be calculated as:

Maximum Stock Level= Re-order level+Re-order Quantity- (Minimum Consumption*Minimum time required for delivery)

= 54,000+36,000- (3,000*4)

=90,000-12,000

=78,000 units.

RE-ORDER LEVEL: It is the stock which is fixed between the maximum and minimum stock levels. It is the level at which the order for the purchase of materials is placed. It is set generally higher than the minimum level to cover any emergency which may arise as a result of abnormal usage of materials or unexpected delay in obtaining fresh supplies. The factors taken into account while fixing re-order level are:

- Consumption rate of material

- Margin of safety

- Minimum level decided to be maintained

- Cost of storage and interest on capital employed in materials.

- Provision for emergencies such as delay in supply and abnormal wastage etc.

The re-order level can be calculated as:

Re-order level= maximum stock + average consumption during normal delivery time

OR

Re-order level= Maximum consumption* Maximum delivery time.

Example: Suppose maximum consumption is 15,000 units per week and maximum delivery time is 10 weeks. The re-order level is calculated as follows:

Re-order level= Maximum consumption* Maximum delivery time.

Re-order Level= 15,000*10

=1, 50,000 units.

DANGER LEVEL: Danger level is fixed at a point below the minimum level and represents the limit at which special steps must be taken to obtain emergent supplies of materials.

It can be calculated as follows:

Danger Level= Normal consumption per day/week/month* Time required to obtain emergent supplies.

Example: Suppose the normal consumption of goofs in a week is 6,000 units and time required for emergent supplies is 1 week. The danger level can be calculated as follows:

Danger Level= Normal consumption per day/week/month* Time required to obtain emergent supplies.

Danger level= 6,000*1= 6,000 units.

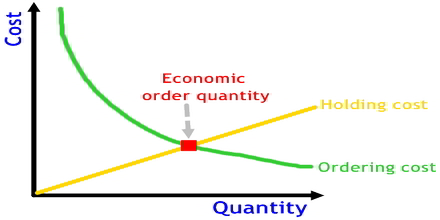

2.ECONOMIC ORDER QUANTITY

Economic order quantity is that size of the order which given maximum economy in purchasing any item of material. There are two main costs that are considered while determining the economic order quantity, these are:

Material Acquisition Costs are related to the number of orders placed during a given period. These costs are part of wages and operating expenses for departments like production control, purchasing, receiving and stores is incurred for purchasing and possessing the materials.

Material carrying costs includes the interest charges on investment in materials, insurance costs, storage costs etc. these costs may be variable or semi-variable in nature as they tend to change nearly in direct proportion to the level of stock carried in the manufacturing concern.

Calculation of Economic Order Quantity

3.PERPETUAL INVENTORY SYSTEM

Perpetual Inventory System refers to a system of maintaining such records as will reflect the receipts, issues and balance of all items of materials in store all the times.

ACCORDING TO ICMA (Institute of Cost and Management Accountants), UK

“Perpetual Inventory System is a system of records maintained by the controlling department, which reflects the physical movement of stock and their current balance.”

The records maintained in a manufacturing concern for material accounting are divided into two parts:

Bin Card: It is maintained in the stores department and shows the quantities of materials received, issued and balance in hand after each receipt and issue.

Stores Ledger: It is maintained by costing office and deals with the quantities and values of materials received, issued and balance in hand.

4.ABC ANALYSIS

ABC analysis is a technique that is followed for the purpose of exercising control over materials according to their importance or value.

Category ‘A’ consists of materials which consists 5% to 10% of the total items in a store and represent 70% to 85% of the total store value. It represents less items with high value.

Category ‘B’ consists of materials which consists of 10% to 20% of the total items in a store and represent 10% to 20% of the total store value. This category represents medium quantity and value.

Category ‘C’ consists of materials which consists of 70% to 855 of the total items in a store and represent 5% to 10% of the store value. This category represents high quantity but small value.

It is also known as Always Better Control method since it aims at obtaining maximum control over materials and minimum cost of control.

5.VED ANALYSIS

This technique of material control is used in connection with the spare parts. Under this

- ‘V’ stands for ‘Vital’

- ‘E’ stands for ‘Essential’

- ‘D’ stands for ‘Desirable’

Vital spare parts are those parts, the unavailability of which will interrupt the production process for quite some time.

Essential spare parts are those spares, the absence of which cannot be tolerated for more than few hours or a day.

Desirable spare parts are those spares which are needed but their non-availability for even a week or so will not lead to interruption in production.

6.MATERIALS TURNOVER

Turnover of materials refers to movement into and out of an organization. It can be calculated by comparing balance of stores with the total issues or withdrawal during a particular period of time.

Material Turnover Ratio= Value of materials consumed during the period/ value of average stock

Average stock= Opening stock+ Closing stock/ 2

High material turnover ratio indicates that the material item is fast moving and exhausts easily.

Low material turnover indicates that the material items are slow moving and organization should not go for over stocking of materials.

Example: Suppose the value of material consumed during the year is 12,000 and average stock available is 450 units, the material turnover ratio will be calculated as:

Material Turnover Ratio= Value of materials consumed during the period/ value of average stock

= 12,000/ 450

= 26.67 times.

MATERIAL CONTROL IN COST ACCOUNTING PDF