MEANING

Bin card is the record maintained under the perpetual inventory system by the stores department and shows the quantities of materials received, issued and balance in hand after each receipt and issue. It is also known as stock card or bin tag. Bin Card helps to monitor the total inventory process. This card is similar to library card that shows total movements of the library books and keeps the tracking of those books. It is issued to track the number of items held in a warehouse or stock rooms.

FEATURES OF BIN CARD

- It is the statement if all the receipts and issues of material from stock from the stores department.

- It is maintained by the store-in-charge or store keeper.

- It is kept inside the store department.

- It records only quantity of materials not the value.

- It is updated when receipts and issues are made in the store department.

- Transactions are updated individually because at every point of time, store keeper needs to be aware of the actual position of the stock.

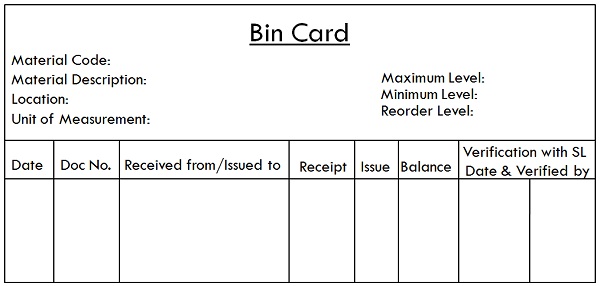

FORMAT

ADVANTAGES OF BIN CARD

- Bin Card is maintained for each item in the stock, in this way it facilitates individual record keeping.

- It also provides information about the minimum level or maximum level of stock.

- Bin Card is flexible to use as its format is not standard or rigidly specified.

- Bin card minimizes the chances of mistakes because the entries will be made at the same time as goods are received or issued by the person actually handling the materials.

- Control over stock can be more effective due to continuous updation.

- It reduces counting errors.

DISADVANTAGES OF BIN CARD

The following are the disadvantages:

- A large store space is required when the bin card is to be used.

- As cards are kept without any protection, it can be damaged.

- Maintaining bin cards can be more expensive.

- There are problems associated with training of the staff that has to keep the bin cards.

- There are chances of omission of receipts and issues of materials due to negligence of employees.