PRICING OF MATERIALS

Pricing of materials refers to valuation of materials issued by the stores department for the production process.

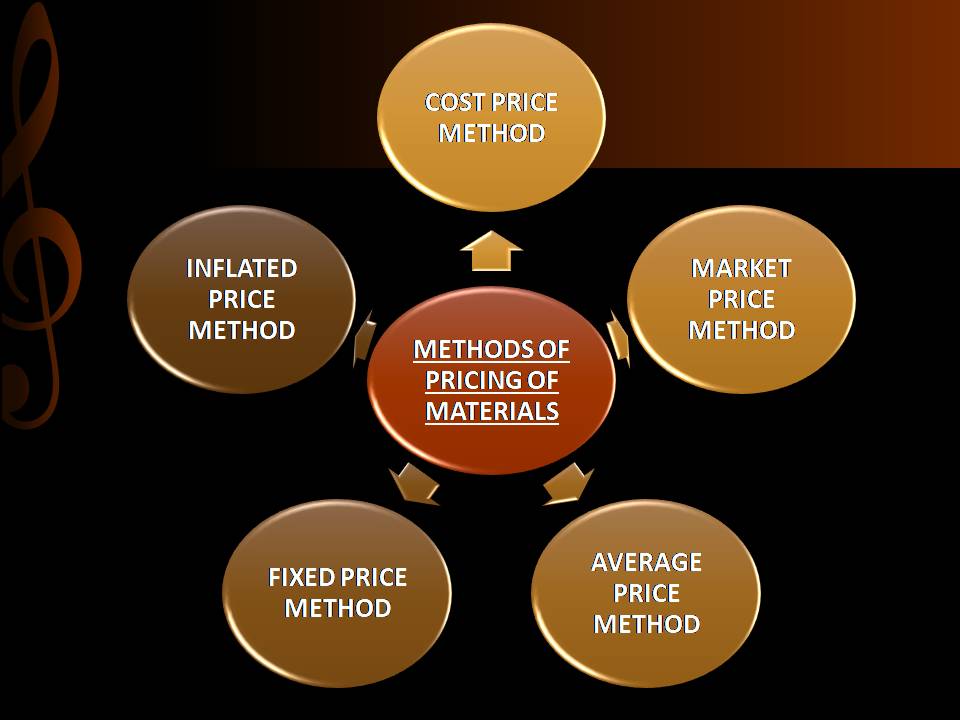

Pricing of materials should be done by adopting the method which is suitable for nature of materials and business itself. The methods applied for pricing of materials are as follows:

1.COST PRICE METHOD

Cost price method is widely adopted method of pricing of materials. It takes the actual cost of the materials for its valuation. The Actual cost is the cost at which the material is originally purchased. The actual cost of materials include amount of:

- Import duty

- Sales tax

- Commission on purchase

- Freight

- Carriage

- Cartage

- Transit insurance

- Octroi charges

The actual cost excludes the amount of:

- Trade discount

- Cash discount

- Quantity discount

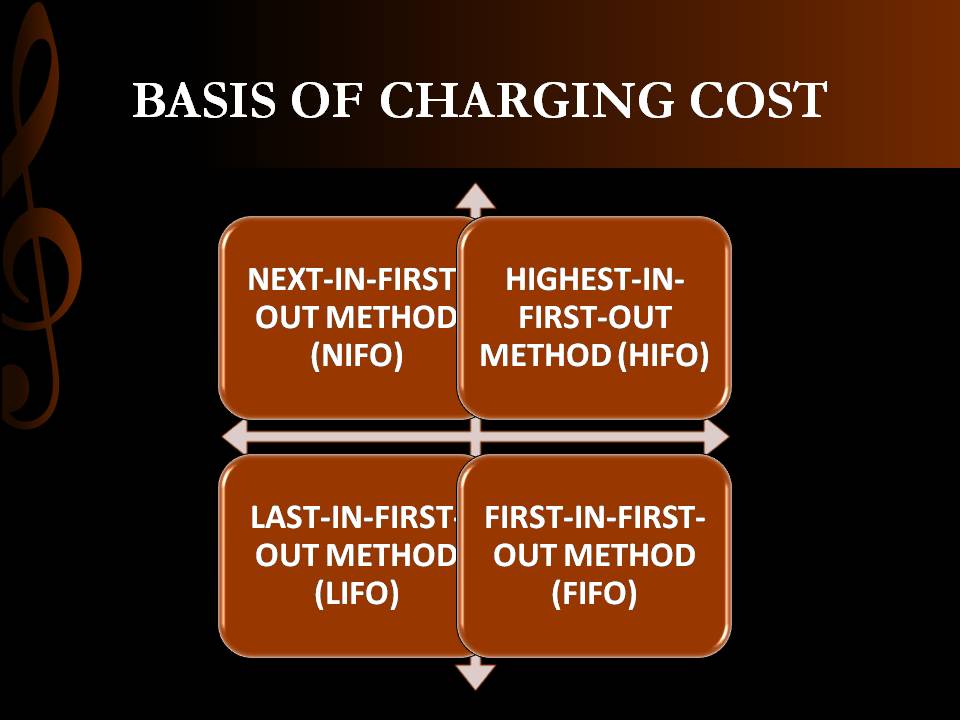

Under this method, the materials issued can be priced on any of the following basis:

FIRST-IN-FIRST-OUT METHOD (FIFO): Under this method, the materials received first are issued first. So the price paid for the earliest lot of materials in hand is taken as the basis of charging out the materials issued. This method is featured as:

- Receipt side of stock ledger is exhausted in chronological order.

- Stock in hand is valued at current or latest purchases.

- Maintenance of the record of quantity and value of every receipt of material.

The advantages of this method are as follows:

- It is simple to apply.

- It follows the principles of costing as in this method the closing materials are valued at current price.

- In this method, accounting flow and physical flow is the same.

- The closing value of materials in this method is close to the current market prices.

The disadvantages of this method are as follows:

- This method involves excessive labor.

- In times of inflationary periods, the cost as per FIFO method will not reflect the current market conditions.

LAST-IN-FIRST-OUT METHOD (LIFO): Under this method, the material received in last is issued first. The price of the latest consignment is taken as base for pricing of materials. This method requires the maintenance of record of quantity and value of every receipt of material.

The main advantages of this method are:

- This method is simple to apply.

- It follows the costing principles.

- The price charged reflects the current prices in the market.

- This method helps in preventing over-statement of profits.

The disadvantages of this method are:

- This method involves too much clerical labor.

- The stock may be under-valued or over-valued as the closing stock shall not reflect the current market prices.

- This pricing method does not conform to the physical flow of materials from the stores.

HIGHEST-IN-FIRST-OUT METHOD (HIFO): Under this method, the materials in hand purchased at the highest price are deemed to be issued first. This method is featured as follows:

- The main aim of adopting this method is to ensure that the values of stock in hand are kept at the lowest possible prices.

- It follows the costing principles.

- It helps in prevention of over-valuation of stocks.

- It is not very popular.

- This method involves tedious calculations.

NEXT-IN-FIRST-OUT METHOD (NIFO): Under this method, issues of material are charged out at the next price i.e. the price at which order for the purchase of materials has been placed but the actual delivery of the materials has not yet been received. This method is featured as follows:

- The aim is to price the materials at a price which is as close to market price.

- This method is not very popular.

- This method involves tedious calculations.

- This method employs excessive labor.

2.MARKET PRICE METHOD

Market price method takes the prevailing market price as a base for valuation of materials to be issued. This method follows the principle of valuation of stock at latest price.

This method has following advantages:

- The price at which the material is valued reflects the current prices.

- This method is suitable for application by the contractors and job order manufacturers.

- This method is simple to apply and does not involve tedious calculations.

- The adoption of this method gives correct financial position of the concern.

The disadvantages of this method are as follows:

- The price of materials issued may not be the true as the prevailing market price is not the real cost of materials.

- There are fluctuations in the market price which makes the issue price of materials fluctuating.

- The adoption of this method poses a serious problem relating to reconciliation of costing and financial records.

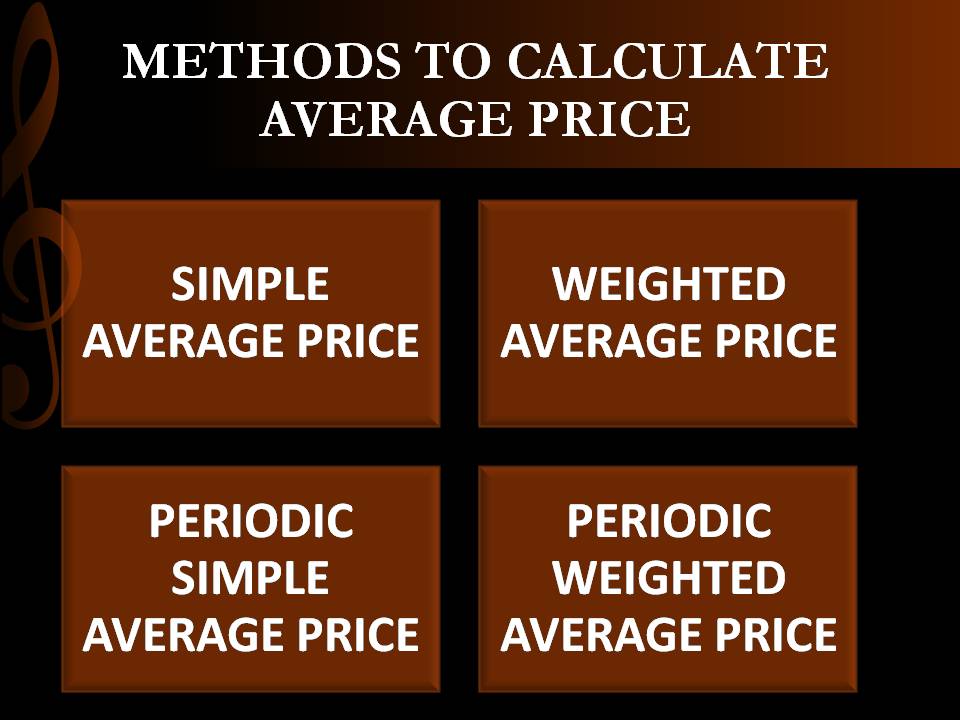

3.AVERAGE PRICE METHOD

This method operates on the basis of calculation of averages. Under this method, the materials in hand are so intermingled that the issues of materials are priced at average cost price of materials in hand; a new average is calculated whenever a fresh purchase is made.

To calculate the average, various methods are adopted:

SIMPLE AVERAGE PRICE: Simple average price is the price calculated by dividing the total of purchase price of materials in hand on the date of issue by the number of prices.

The advantages of this method are:

- This method is simple in operation

- It gives reliable results under stable prices.

- It minimizes the variances in the cost and the market prices.

The disadvantages under this method are as follows:

- It does not project the accurate total cost.

- This method is unscientific in application.

- Under-charging and over-charging of material costs give inaccurate profit or loss.

- Valuation of stock is usually incorrect under this method.

WEIGHTED AVERAGE PRICE: It is the price which is calculated by dividing the cost of materials in stock from which materials to be priced could be drawn, by the total quantity of materials in the stock.

Weighted Average Price= Total cost of materials in stock/ Total units in stock

The advantages of this method are:

- It is simple to understand and easy to operate.

- The results of this method are more reliable and accurate.

- The total cost of materials is recovered from the total production under this method.

The disadvantages of this method are:

- This method involves tedious calculations.

- Closing stock price does not represent the current market prices.

- There are chances of profit or loss because of over-charging and under-charging of materials costs to jobs.

PERIODIC SIMPLE AVERAGE PRICE: This method is also known as End of Period method and End of Month method. Under this method, valuation of material issued is based on the simple average of all prices of materials purchased during a specific period of time, say a month.

Periodic Simple Average Issue Price= Total of prices of purchases during the period/ No. of prices during the period.

The advantages of this method are:

- This method is easier to operate and simple to understand.

- It is suitable for large scale undertakings.

- The average issue price representing different lots is more representative.

The disadvantages of this method are:

- The value of closing stock does not represent the current market price or cost of the product.

- The approximation of figures under this method may lead to under-absorption or over-absorption of costs.

- There are tedious calculations involved under this method.

PERIODIC WEIGHTED AVERAGE PRICE: It is calculated by dividing the total cost of materials purchased by the total quantity purchased. The weighted average price is calculated at the end of the year.

Periodic Weighted Average Price= Cost of materials received/ Quantity received.

Advantages of this method are as follows:

- The price is easy to calculate by this method.

- This method is suitable for the industries where there are wide fluctuations.

- It can be applied with greater success in case of processing industries.

Disadvantages of this method are:

- There is every possibility of under-recovery and over-recovery of cost of materials.

- The calculations are very lengthy and tedious.

4.FIXED PRICE METHOD

This method is also known as Standard Price Method. As per this method, the materials issued are priced as per the pre-determined price or fixed price. The standard price is set for a fixed period and all the materials issues are priced at that price for a fixed term.

The standard prices are of two types which are as follows:

Basic standard price which is fixed for longer period of time which is greatly helpful in future planning.

Current standard price which is fixed for a shorter period of time and can be adjusted in accordance with the changed circumstances.

The difference between the standard price and actual price is known as Variance.

- Actual price> Standard Price= Negative Variance

- Actual price<Standard Price= Positive Variance

Advantages of this method are:

- This method is simple to apply and easy to use.

- It considerably reduces the clerical work.

- It can be used as an effective tool to initiate effective control over purchases.

Disadvantages of this method are:

- The fixation of standard price is a cumbersome process.

- There exists the possibility of over-recovery and under-recovery of material costs.

5.INFLATED PRICE METHOD

This method is used when the materials are subject to normal wastage which is unavoidable. In order to recover the loss arising due to normal wastage, the material issues are priced at the higher rate known as inflated price.