OVERHEAD

Overhead is the aggregate of indirect material costs, indirect labor costs and indirect expenses.

These are those costs which cannot be allocated accurately but can be apportioned and absorbed to the cost centers or cost units. Overheads costs are also known as ‘ Supplementary costs’, ‘Non-productive costs’, ‘Indirect costs’ etc.

ACCORDING TO BLOCKER AND WELMER

“Overhead costs are the operating cost of a business enterprise which cannot be traced directly to a particular unit of output.”

ACCORDING TO WHELDON

“Overhead may be defined as the cost of indirect materials and such other expenses, including services as cannot conveniently be charged directly to specified cost units. Alternatively, overheads are all expenses other than direct expenses.”

CLASSIFICATION OF OVERHEADS

The overheads are of various types on various bases. The classification of overhead on various bases is as follows:

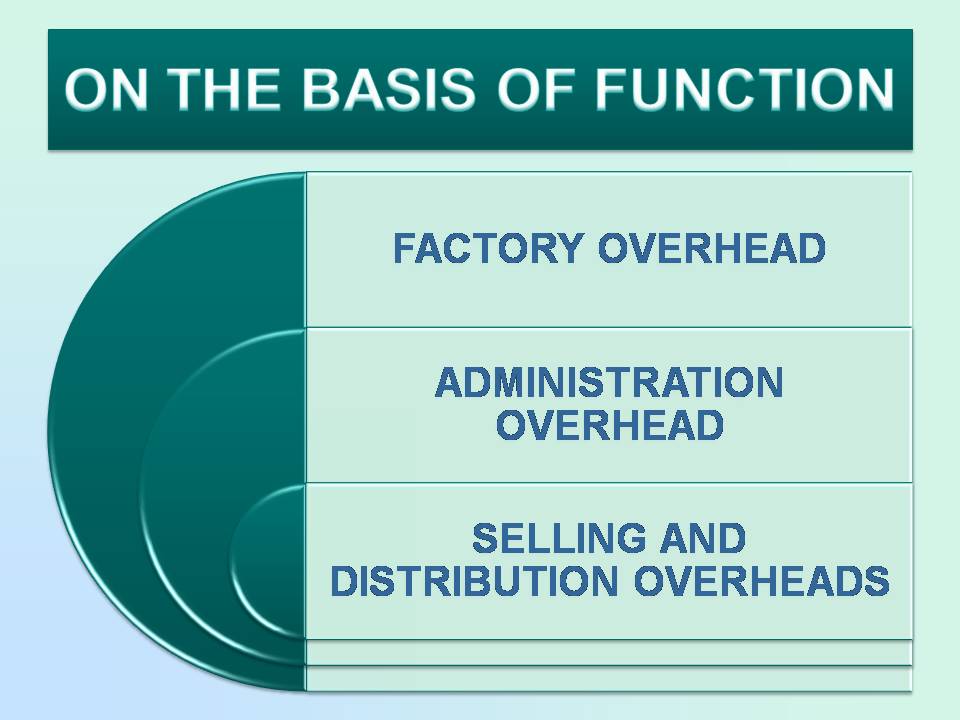

ON THE BASIS OF FUNCTION

1.Factory overheads: It includes all the indirect costs incurred in factory in respect of manufacturing operations. It includes the cost of indirect materials and indirect labor.

Example: Cost of lubricating oil, coal, gas and fuel, wages of store-keeper, salaries of foremen, supervisors, factory rent etc.

2.Office and Administration Overhead: It refers to the general expenses and expenses of administration and control of business. It includes all the indirect costs relating to direction, guidance, management, control and administration of business concern.

Example: Salary of general manager, insurance expenses, office rents, office rates, office lighting etc.

3.Selling and Distribution overheads: These include all the indirect costs which are incurred for

- Promoting the sales

- Retaining the customers

- Providing after sale services to the consumers

- Raising the market share of the concern.

Example: Advertisement, salary of sales manager etc.

These costs play an important role in growing the business and its goodwill.

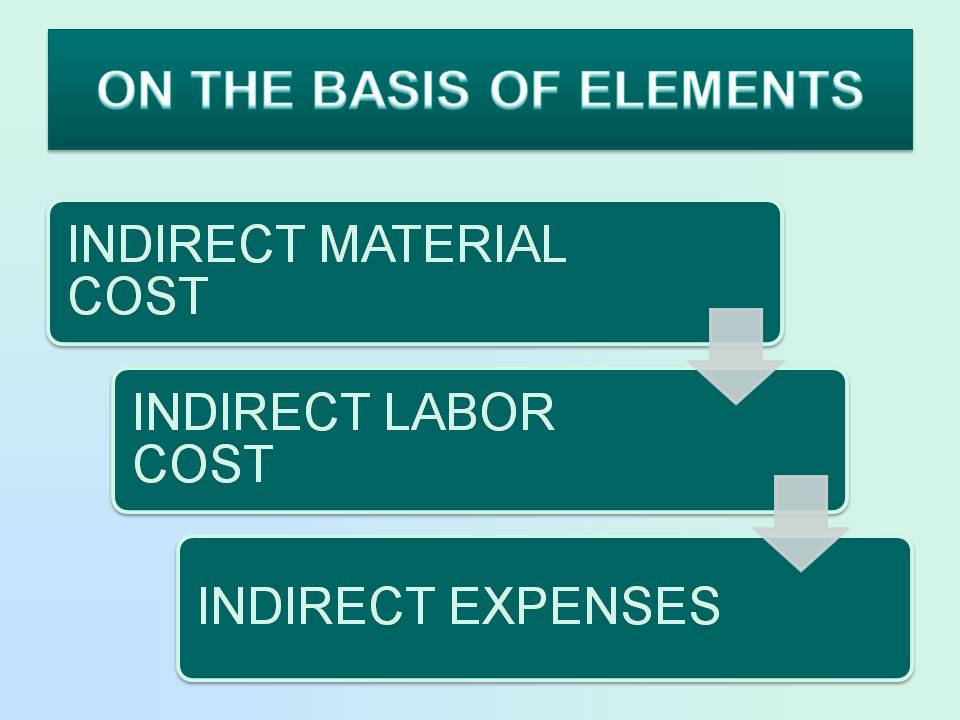

ON THE BASIS OF ELEMENTS

1.Indirect Material Cost: Indirect Material Cost is the cost which is not directly attributable to the finished product. These costs are not absorbed or apportioned by the cost units or cost centers directly. The cost of such material is not traceable in the finished product. These costs can also be known as non-identifiable or hidden costs.

Example:

- Cost of grease or lubricating oil used in maintenance of machinery.

- Fuel or electricity needed for generating power.

- Materials consumed for repair work.

- Dusters and brooms used for cleansing of factory.

2.Indirect Labor Cost: These are also known as indirect wages. It refers to that part of labor cost which is not directly attributable to the cost centers or cost units. These are not apportioned to or absorbed by the cost centers or cost units.

Example: Salary paid to the manager, Salary paid to the guard of the office.

3.Indirect Expenses or Overheads: Expenses which cannot be allocated to the cost centers or units but can be apportioned by them are known as overheads or indirect expenses.

Example:

- Rent, rates and taxes

- Repairs to machinery

- Factory lighting

- Office lighting

- Depreciation and insurance of showroom building etc.

The aggregate of indirect material cost, indirect labor cost and indirect expenses is known as Indirect Cost.

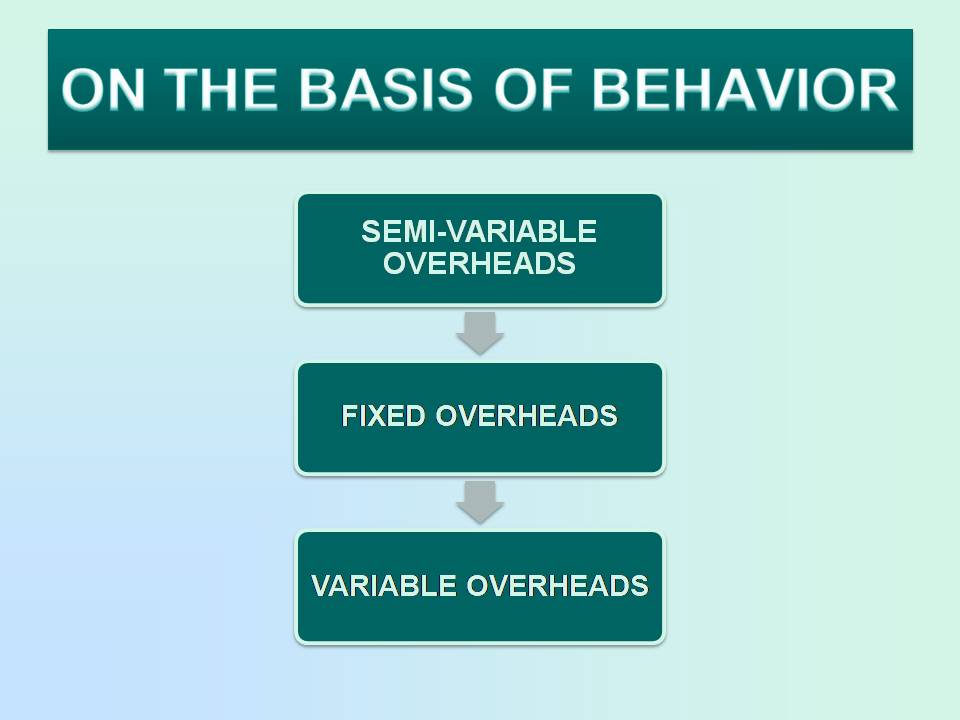

ON THE BASIS OF BEHAVIOR

1.FIXED OVERHEADS: A fixed cost is a cost which is incurred for a particular period of time and which, within certain activity levels, is unaffected by changes in the level of activity. These costs mainly depends upon the effluxion of time and do not vary directly with the changes in the volume or output or sales. Example: rent of the building, insurance of the building etc.

2.VARIABLE OVERHEADS: A variable cost is a cost which tends to vary with the level of activity. These costs tend to increase or decrease with the rise and fall in the production or sales. These costs vary in total but per unit cost remains the same. Example: cost of raw material used in producing finished product.

3.SEMI VARIABLE OVERHEADS: This is the cost that contains both a fixed cost and a variable cost component. The part of semi-variable costs remains constant in spite of changes in the volume of output or sales, while the other part varies in proportion to changes in volume of output or sales. Example: Repairs and maintenance cost of plant, salary of supervisor etc.

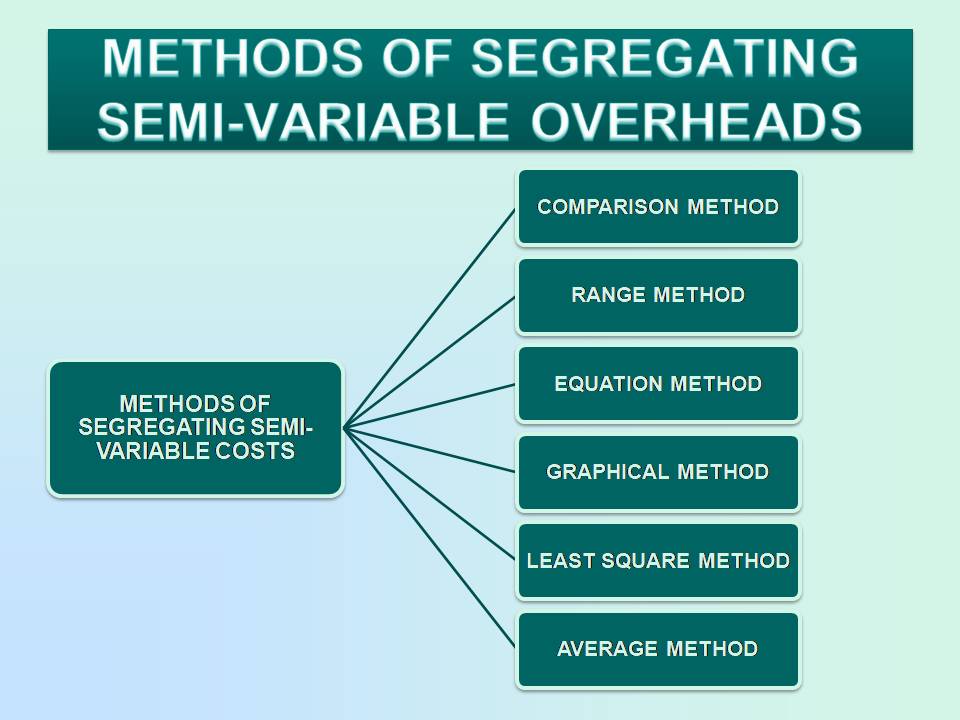

METHODS OF SEGREGATING SEMI-VARIABLE OVERHEADS

In case of classification of costs on the basis of the activity or behavior, the problem faced by the cost accountant is of segregating the semi-variable costs into fixed portion and variable portion. For this following methods can be used:

1.COMPARISON METHOD: The comparison method is followed to segregate the semi-variable overheads into fixed overheads and variable overheads. Under this method the quantity of output at two different levels is compared with the corresponding amount of expense. The amount of fixed overhead remains same and the amount of variable overhead is calculated as follows:

Variable cost per unit= Change in amount of expense/ Change in quantity or output

EXAMPLE: Segregate semi-variable costs as per comparison method:

| PERIOD | OUTPUT | SEMI-VARIABLE OVERHEAD |

| JULY | 350 | 3,100 |

| AUGUST | 420 | 3,520 |

| SEPTEMBER | 400 | 3,400 |

SOLUTION:

| MONTH | PRODUCTION | SEM-VARIABLE EXPENSE |

| July | 350 | 3,100 |

| September | 400 | 3,400 |

| Change | 50 | 300 |

Variable cost per unit= Change in expense/ Change in Output

Variable cost per unit= 300/50= Rs.6

In month of July

Variable Expense= 350*6= Rs. 2,100

Fixed Expense= 3,100-2,100= Rs.1, 000

This method of segregating semi-variable costs is easy but not scientific and accurate.

2.RANGE METHOD: This method is also known as High and Low Points method. Under this method, the amount of expense at the highest and lowest levels are compared and related to output attained at those levels. As the amount of fixed overheads remains the same, the change in indirect cost is due to the variable portion.

VARIABLE COST PER UNIT= Change in amount of expense/ Change in output.

EXAMPLE: Segregate semi-variable costs as per Range method:

| PERIOD | OUTPUT | SEMI-VARIABLE OVERHEAD |

| JULY | 350 | 3,100 |

| AUGUST | 420 | 3,520 |

| SEPTEMBER | 400 | 3,400 |

| OCTOBER | 430 | 3,580 |

| NOVEMBER | 380 | 3,280 |

| DECEMBER | 270 | 2,620 |

SOLUTION:

| PERIOD | OUTPUT | SEMI-VARIABLE OVERHEAD |

| OCTOBER (HIGHEST) | 430 | 3,580 |

| DECEMBER (LOWEST) | 270 | 2,620 |

| DIFFERENCE OR CHANGE | 160 | 960 |

VARIABLE COST PER UNIT= Change in amount of expense/ Change in output.

VARIABLE COST PER UNIT= 960/160= Rs. 6 per unit.

Overhead= 430*6= Rs. 2,580

Fixed Portion= 3,580-2,580= Rs. 1,000

3.EQUATION METHOD: Under this method, variable and fixed portions of overhead are ascertained by means of straight line equation. The straight line equation is:

Y= mx+ C

Where Y= Total semi-variable cost

C= Fixed costs included in semi-variable costs

m= Variable cost per unit

x= Output or number of units.

EXAMPLE:

| PERIOD | OUTPUT | SEMI-VARIABLE OVERHEAD |

| JULY | 350 | 3,100 |

| AUGUST | 420 | 3,520 |

| SEPTEMBER | 400 | 3,400 |

| OCTOBER | 430 | 3,580 |

| NOVEMBER | 380 | 3,280 |

| DECEMBER | 270 | 2,620 |

SOLUTION:

Taking the figures of July and August

July: 3,100=350m+C……………………………..(i)

August: 3,520= 420m+ C……………………….(ii)

Subtracting (i) from (ii) 420= 70m

M=420/70= Rs.6 per unit

Putting the value of ‘m’ in equation (i)

3,100= 350*6+ C

3,100= 2,100+C

Hence, C= 3,100-2,100= Rs. 1,000 (Fixed Cost)

4.AVERAGE METHOD: Under this method of segregation of fixed and variable elements is made by first taking the average of two selected groups and then applying the range method or equation method, as the case may be.

EXAMPLE:

| PERIOD | OUTPUT | SEMI-VARIABLE OVERHEAD |

| JULY | 350 | 3,100 |

| AUGUST | 420 | 3,520 |

| SEPTEMBER | 400 | 3,400 |

| OCTOBER | 430 | 3,580 |

| NOVEMBER | 380 | 3,280 |

| DECEMBER | 270 | 2,620 |

SOLUTION:

| AVERAGE OUTPUT | AVERAGE SEMI-VARIABLE OVERHEAD | |

| First two methods (July and August) | 385 (350+420)/2 | 3,310 (3,100+3,520) |

| Last two months | 325 (380+270)/2 | 2,950 (3,280+2,620)/2 |

| Change | 60 | 360 |

Variable overhead per unit= Change in amount/ Change in output

Variable overhead per unit= 360/60= Rs.6 per unit.

Total Overhead= 3,310

Less: Variable Overhead= (2,310)

Fixed Overhead= 1,000

The result obtained under this method may not be accurate.

5.GRAPHICAL METHOD: Under this method, the portion of variable and fixed overheads are ascertained by plotting the amounts of semi-variable or semi-fixed overheads incurred at various level of activity on graph paper and drawing the ‘line of best fit’.

Under the graphical method, volume of output is drawn on horizontal axis and semi-variable expenses on vertical-axis. Expenses corresponding to each volume are plotted on the graph paper and a straight line, ‘the line of best fit’ is drawn through the points plotted. This straight line represents the ‘total cost line.’ The point where the straight line intersects the vertical-axis is taken to be the amount of fixed expenses.

A parallel line from the intersecting point to the amount of fixed expenses. A parallel line from the intersection point to the horizontal axis gives the ‘fixed cost line’. Thereafter, the ascertainment of variable cost can be made by means of comparison of fixed cost and total cost.

6.LEAST SQUARE METHOD: Under this method, segregation of fixed and variable elements of semi-variable overhead is made by finding out a ‘line of best fit’ for a number of observations with the help of statistical methods:

Y= mx+ C

Where Y= Total semi-variable cost

C= Fixed costs included in semi-variable costs

m= Variable cost per unit

x= Output or number of units.

EXAMPLE:

| PERIOD | OUTPUT | SEMI-VARIABLE OVERHEAD |

| JULY | 350 | 3,100 |

| AUGUST | 420 | 3,520 |

| SEPTEMBER | 400 | 3,400 |

| OCTOBER | 430 | 3,580 |

| NOVEMBER | 380 | 3,280 |

| DECEMBER | 270 | 2,620 |

SOLUTION:

Taking the figures of July and August

July: 3,100=350m+C……………………………..(i)

August: 3,520= 420m+ C……………………….(ii)

Subtracting (i) from (ii) 420= 70m

M=420/70= Rs.6 per unit

Putting the value of ‘m’ in equation (i)

3,100= 350*6+ C

3,100= 2,100+C

Hence, C= 3,100-2,100= Rs. 1,000 (Fixed Cost)

NECESSITY FOR CLASSIFICATION OF OVERHEAD INTO FIXED AND VARIABLE OVERHEADS

The following are the reasons of necessity for classification of overhead into fixed and variable overheads:

EFFECTIVE COST CONTROL: To exercise the effective cost control, proper classification of overhead into fixed or variable is required. Fixed expenses are incurred by management decision and as such can be controlled by the top management while variable expenses can be controlled by lower management.

HELPFUL IN DECISION MAKING: The classification of fixed or variable overheads helps in taking the following decisions by management:

- Make or buy decision

- Selection of suitable sales mix

- Operate or shut down decisions

- Expansion or contraction of the production of various products, etc.

FIXATION OF SELLING PRICE: The classification of overheads into fixed or variable is very helpful in determining the selling price of the products or services. Sometimes, a manufacturer charges different prices for the same articles in different markets to meet varying degrees of competition.

However, the lowest selling price of any product should at least cover prime cost plus variable overhead. This classification also helps in determining the price during trade depression or in a special market.

MARGINAL COSTING AND COST-VOLUME ANALYSIS: The classification of fixed or variable overhead elements is very essential for the technique of marginal costing and break-even analysis. It helps in ascertaining the marginal cost i.e. the total variable cost attributable to one unit of output.

Further, it assists in determining the break-even point i.e. the volume of output where there is no profit and no loss.

HELPFUL IN BUDGETARY CONTROL: Classification of fixed or variable overhead is very helpful in preparation of flexible budgets. A flexible budget is a budget which is designed to change in accordance with the level of activity actually attained. Flexible budget for various levels of activity can be prepared with the help of this classification.

ABSORPTION OF OVERHEAD: This classification helps in the proper absorption of the different items of overhead. This method to be adopted for determining the absorption rates depends on the nature of overhead.