TREATMENT OF NORMAL LOSS AND ABNORMAL LOSS IN PROCESS COSTING

In manufacturing processes, entire input is not getting converted into output. A certain part of input is lost while processing which is inevitable. Certain production techniques are of such a nature that some loss is inherent to the production. Wastages of material, evaporation of material are un- avoidable in some process. But sometimes the Losses are also occurring due to negligence of Labourer, poor quality raw material, poor technology etc. These are normally called as avoidable losses. Basically, process losses are classified into two categories

(a) Normal Loss

(b) Abnormal Loss

Treatment of Normal Loss in Process Costing

Normal losses in process costing arises because of the normal wastage. Normal wastage is the quantity od wastage which is unavoidable and is bound to take place. It cannot be avoided though efforts can be made to minimise it. Normal wastage generally arises on account of the nature of materials used or the nature of the manufacturing process involved. The extent of normal wastages can be ascertained on the basis of past experience.

The cost of normal wastage or loss in the process is borne by the goods units produced in the process. The quantity of normal wastage or loss is shown in the ‘units column’ on the credit side of the Process Account. If the normal loss or wastage has some realisable value, the process account is credited with such realisable value. Thus, the total process cost less any realisable value or scrap value of normal wastage divided by the number of good units produced in the process, shall give us the cost per unit.

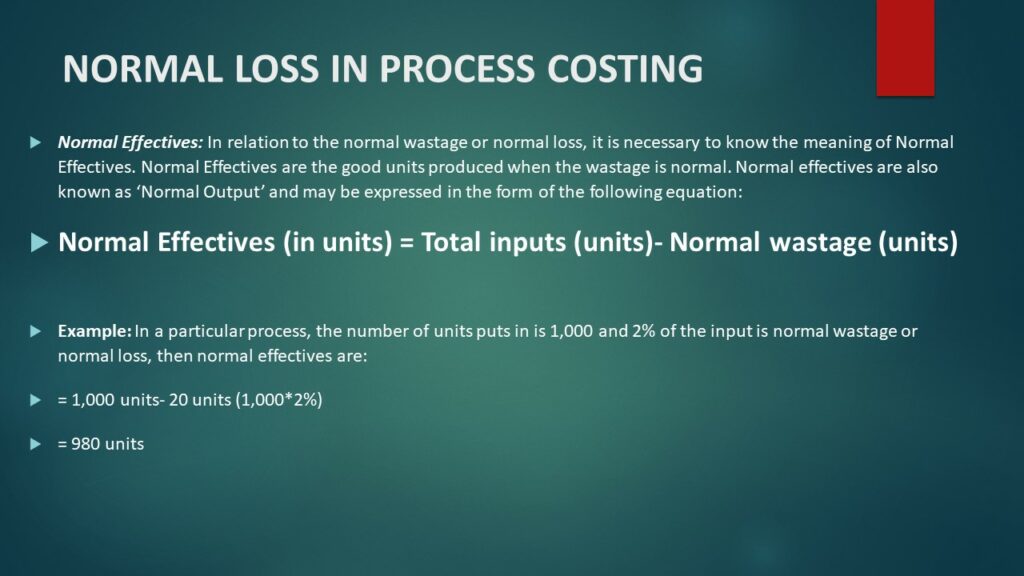

Normal Effectives: In relation to the normal wastage or normal loss, it is necessary to know the meaning of Normal Effectives. Normal Effectives are the good units produced when the wastage is normal. Normal effectives are also known as ‘Normal Output’ and may be expressed in the form of the following equation:

Normal Effectives (in units) = Total inputs (units)- Normal wastage (units)

Example: In a particular process, the number of units puts in is 1,000 and 2% of the input is normal wastage or normal loss, then normal effectives are:

= 1,000 units- 20 units (1,000*2%)

= 980 units

JOURNAL ENTRIES FOR NORMAL LOSSES

| Debit | Credit | |

| For scrap value of normal loss | Normal loss A/c | Process A/c |

| For adjustment of the short fall in the sale of normal loss | Normal Gain A/c | Normal Loss A/c |

| For realisation of scrap value of normal loss | Cash A/c | Normal Loss A/c |

Treatment of Abnormal loss in process costing

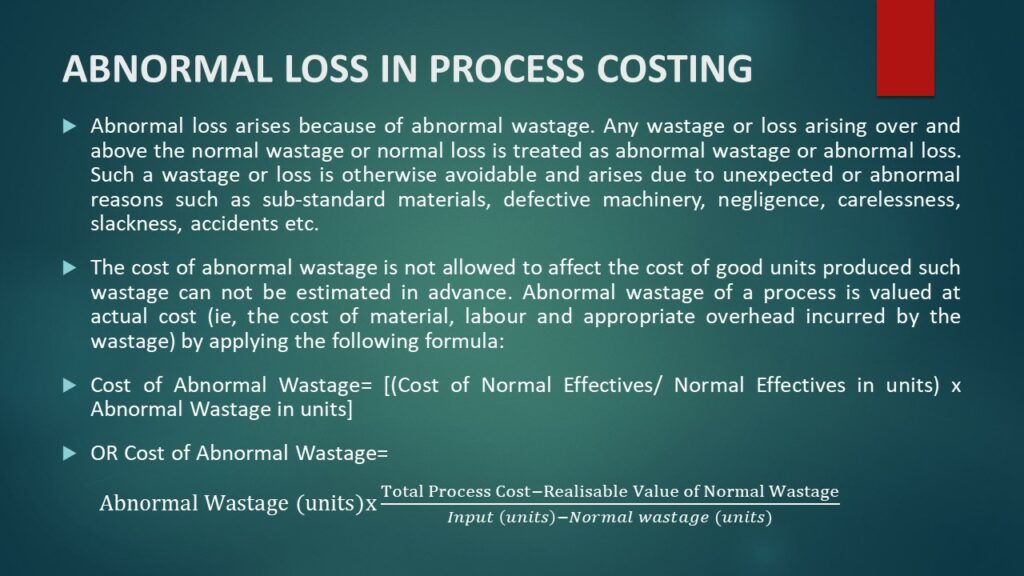

Abnormal loss arises because of abnormal wastage. Any wastage or loss arising over and above the normal wastage or normal loss is treated as abnormal wastage or abnormal loss. Such a wastage or loss is otherwise avoidable and arises due to unexpected or abnormal reasons such as sub-standard materials, defective machinery, negligence, carelessness, slackness, accidents etc.

The cost of abnormal wastage is not allowed to affect the cost of good units produced such wastage can not be estimated in advance. Abnormal wastage of a process is valued at actual cost (ie, the cost of material, labour and appropriate overhead incurred by the wastage) by applying the following formula:

Cost of Abnormal Wastage= [(Cost of Normal Effectives/ Normal Effectives in units) x Abnormal Wastage in units]

OR Cost of Abnormal Wastage=

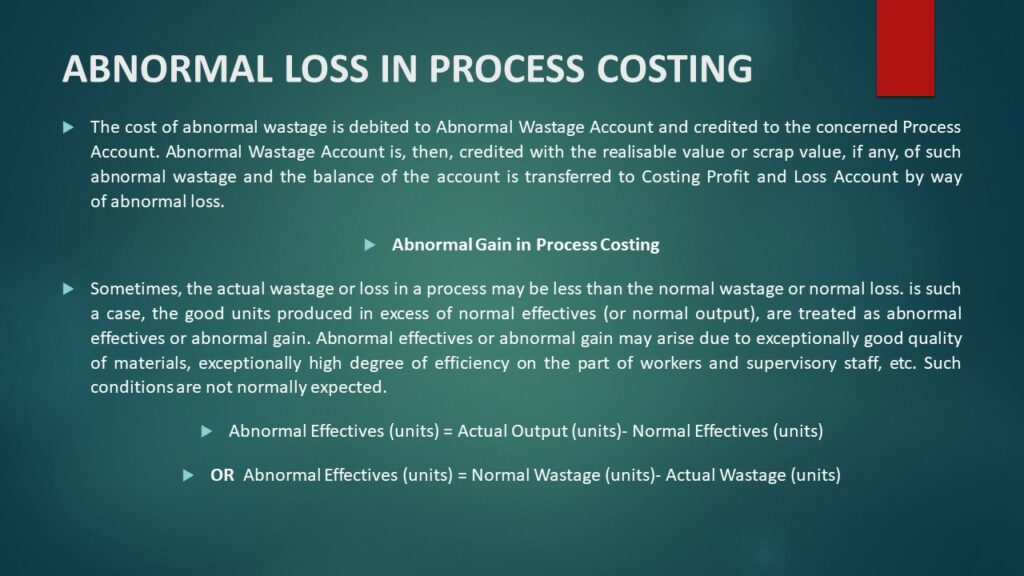

The cost of abnormal wastage is debited to Abnormal Wastage Account and credited to the concerned Process Account. Abnormal Wastage Account is, then, credited with the realisable value or scrap value, if any, of such abnormal wastage and the balance of the account is transferred to Costing Profit and Loss Account by way of abnormal loss.

JOURNAL ENTRIES FOR ABNORMAL LOSSES

| Debit | Credit | |

| For value of abnormal loss | Abnormal loss A/c | Process A/c |

| For realisation of scrap value | Cash A/c | Abnormal Loss A/c |

| For transfer of balance to Costing profit and loss account | Costing profit and loss A/c | Abnormal Loss A/c |

Treatment of Abnormal Gain in Process Costing

Sometimes, the actual wastage or loss in a process may be less than the normal wastage or normal loss. is such a case, the good units produced in excess of normal effectives (or normal output), are treated as abnormal effectives or abnormal gain. Abnormal effectives or abnormal gain may arise due to exceptionally good quality of materials, exceptionally high degree of efficiency on the part of workers and supervisory staff, etc. Such conditions are not normally expected.

In the form of equation, abnormal effectives or abnormal gain may be expressed or follows:

Abnormal Effectives (units) = Actual Output (units)- Normal Effectives (units)

OR

Abnormal Effectives (units) = Normal Wastage (units)- Actual Wastage (units)

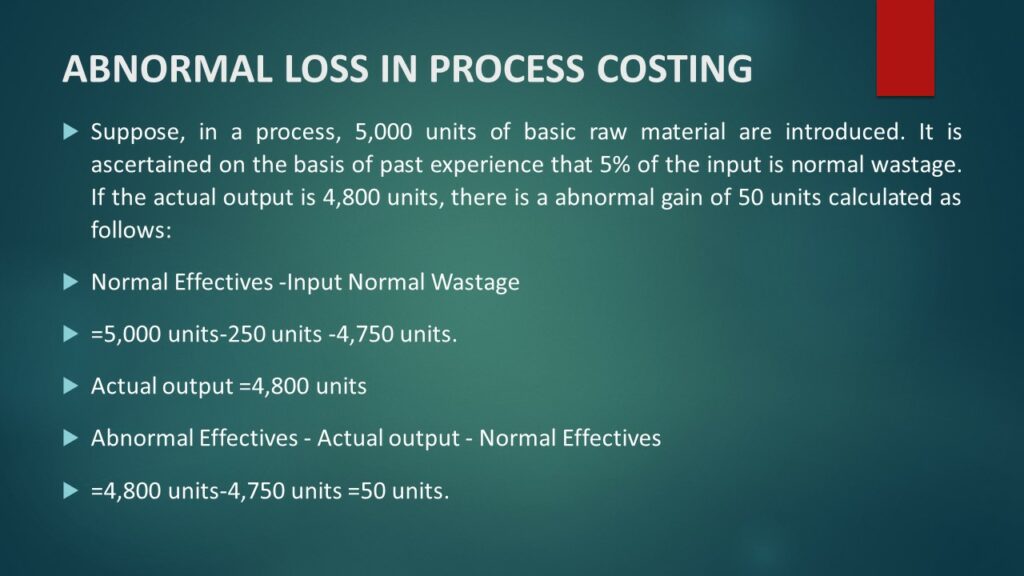

Suppose, in a process, 5,000 units of basic raw material are introduced. It is ascertained on the basis of past experience that 5% of the input is normal wastage. If the actual output is 4,800 units, there is a abnormal gain of 50 units calculated as follows:

Normal Effectives -Input Normal Wastage

=5,000 units-250 units -4,750 units.

Actual output =4,800 units

Abnormal Effectives – Actual output – Normal Effectives

=4,800 units-4,750 units =50 units.

Accounting Treatment of Abnormal Gain or Abnormal Effectives:

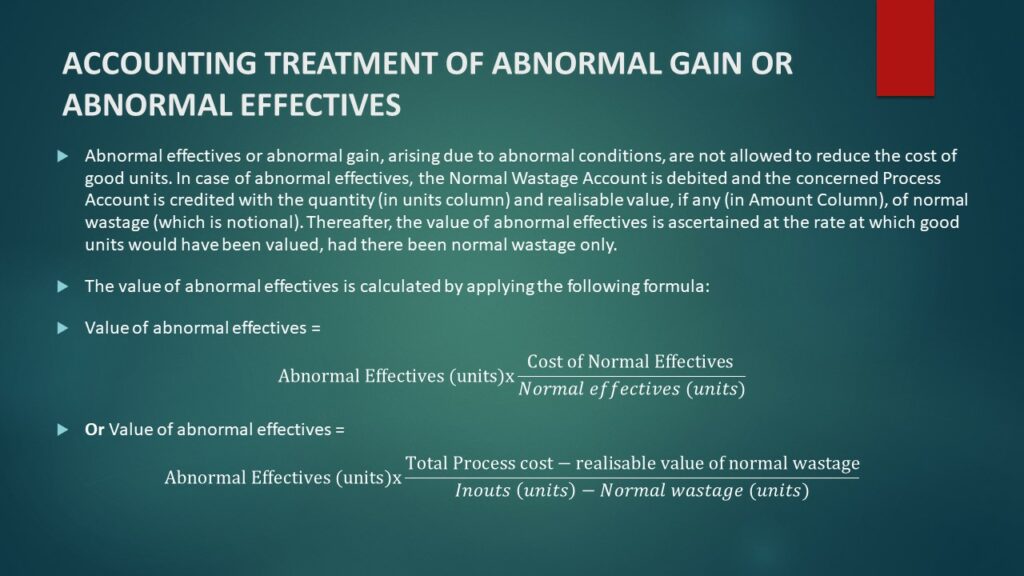

Abnormal effectives or abnormal gain, arising due to abnormal conditions, are not allowed to reduce the cost of good units. In case of abnormal effectives, the Normal Wastage Account is debited and the concerned Process Account is credited with the quantity (in units column) and realisable value, if any (in Amount Column), of normal wastage (which is notional). Thereafter, the value of abnormal effectives is ascertained at the rate at which good units would have been valued, had there been normal wastage only. The value of abnormal effectives is calculated by applying the following formula:

Value of abnormal effectives =

Or

Value of abnormal effectives =

The value of abnormal effectives thus determined will be debited to Process Account concerned and credited to Abnormal Effectives Account (or Abnormal Gain Account). The realisable value of actual wastage (which is less than the notional quantity of normal wastage) is credited to the Normal Wastage Account. The debit balance of Normal Wastage Account, denoting the excess of quantity and value of notional normal wastage over the quantity and value of actual wastage, is transferred to the Abnormal Effectives Account. Thereafter, the credit balance of Abnormal Effectives Account is closed by transfer to Costing Profit and Loss Account by way of abnormal gain or profit.

JOURNAL ENTRIES FOR ABNORMAL GAINS

| Debit | Credit | |

| For value of abnormal gain | Process A/c | Abnormal gain A/c |

| For realisation of scrap value | Abnormal gain A/c | Normal Loss A/c |

| For transfer of balance to Costing profit and loss account | Abnormal gain A/c | Costing profit and loss A/c |