ZERO BASE BUDGETING PROCESS

Zero base budgeting process is process wherein each cost element for the period is clearly justified, in terms of cost benefits. The management analyses and prioritizes the activities, depending on the determinants like alignment with the organizational objectives, fund availability, etc.

Hence, all the activities are reassessed every time the budget is prepared. Its aim is to reduce the expenditure, by identifying the areas where cost can be cut.

ACCORDING TO ORIGINATOR PETER A PYHER

“A planning and budgeting process which requires each manager to justify his entire budget request in detail from scratch (hence zero base) and shifts the burden of proof to each manager to justify why he should spend any money at all. The approach requires that all activities be analyzed in ‘decision packages’ which are evaluated by systematic analysis and ranked in order of importance.”

ACCORDING TO CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS, LONDON

“Zero Base Budgeting is a method of budgeting whereby all activities are revaluated each time a budget is set. Discrete levels of each activity are valued and a combination chosen to match funds available”.

ACCORDING TO LEONARD MEREUNIT AND STEPHEN SOSMICK

“ZBB is a technique, which complements and links the existing planning, budgeting and review processes, it identifies alternative efficient methods of utilizing limited resources in effective attainment of selected benefits. It is a flexible management approach, which provides credible rationale for reallocating resources by focusing on the systematic review and justification of the funding and performance levels of current programmes or activities.

EVOLUTION OF ZERO BASE BUDGETING

In 1964, The United States Department of Agriculture introduced this system, but it was not found to be quite successful and, hence, abandoned. In the early seventies, however, it was Pytor, A. Pyhrr, a staff control manager of Texas Instrument Corporation, United States of America, who introduced and developed this technique through his writings.

Since then, a good number of private sector organisations have introduced ZBB in Budgetary Control, particularly in the U.S.A. And again, in 1972, the State of Georgia introduced the technique and the then governor of the State of Georgia, Jimmy Carter, recognised widely the relevance of ZBB and when he became the president of the U.S.A., he introduced this system in the Federal Govt., in 1977. The public sector undertaking also showed keen interest in ZBB and adopted the technique in budgeting.

FEATURES OF ZERO BASE BUDGETING

- Manager of a decision unit has to completely justify why there should be at all any budget allotment for his decision unit. This justification is to be made a fresh without making reference to previous level of spending in his department.

- Activities are identified in decision packages.

- Decision packages are ranked in order of priority.

- Packages are evaluated by systematic analysis.

- Under this approach there exist a frank relationship between superior and subordinates. Management agrees to fund for a specified service and manager decision of the decision unit clearly accepts to deliver the service.

- Decision packages are linked with corporate objectives, which are clearly laid down.

- Available resources are directed towards alternatives in order of priority to ensure optimum results.

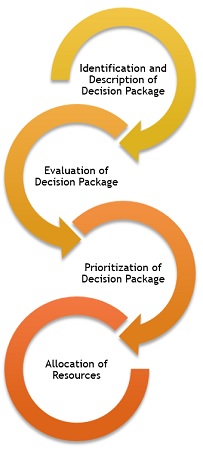

ZERO BASE BUDGETING PROCESS

To understand the stages of ZBB, first of all, it is needed to know the meaning of decision packages. Decision packages refer to the development of an operational plan for the activities for which decisions are to be made. The stages are given as under:

- Identification and Description of Decision Packages: Decision package ascertains a particular activity, so as to analyse and rank the activities against other activities, with respect to the use of scarce resources and make decisions thereon.

- Evaluation of Decision Packages: After identification and description, decision packages are evaluated considering the factors like alignment with the organizational objectives, regulatory requirement and availability of money.

- Prioritisation of the Decision Packages: Decision packages are ranked on the basis of activities.

- Allocation of Resources: Once the ranking is done, resources are allotted to the packages, which facilitates in the process of preparation of the budget, as it is done for the very first time, without any consideration to previous year’s budgets.

The decision packages provide you with the details such as the cost involved, return, objective, expected outcome, alternatives available and consequences of non-performance of the activity.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN

https://www.linkedin.com/in/kajal-mahajan-7549b2197/