RELATIONSHIP BETWEEN TP AP AND MP

Product or output refers to the volume of goods produced by a firm or an industry during a specified period of time. The concept of product can be considered from three different angles – Total Product, Marginal Product, Average Product.

TOTAL PRODUCT (TP)

Total Product (TP) refers to the total quantity of goods produced by a firm during a given period of time with the given number of inputs.

EXAMPLE: If 10 labourers produce 60 kg of rice, then the TP is 60 kg.

In the short run a firm can expand TP by increasing only the variable factors. However, in the long run, TP can be raised by increasing both fixed and variable factors. TP is also known as ‘Total Physical Product (TPP)’ or ‘Total Return’ or ‘Total Output’.

MARGINAL PRODUCT (MP)

Marginal Product (MP) refers to the addition to TP, when one more unit variable factor is employed. MP can be written as,

MPn = TPn – TPn-1

Where,

MPn = MP of nth unit

of variable factor

TPn = TP of n units of variable factor

TPn-1 = TP of (n-1) units of variable factor

n = number of units of variable factor

EXAMPLE: If 10 labourers make 60 kg of rice and 11 labourers make 67 kg of rice, then MP of the 11th labour will be

MP11 = TP11 – TP10

MP11 = 67-60 = 7 kg

MP is the change in TP when one more unit of variable factor is employed. However, when change in variable factor is greater than one unit, then MP can be calculated as,

MP = Change in TP/ Change in units of Variable Factor

MP = ΔTP/ΔN

EXAMPLE: Suppose 2 labourers produce 60 units and 5 labourers produce 90 units, then MP will be,

MP = 90-60/5-2

= 30/3

= 10 units

AVERAGE PRODUCT (AP)

Average product (AP) refers to output per unit variable input. For example, if TP is 60 kg of rice, produced by 10 labourers (variable input), then AP will be 60/10 = 6 kg.

AP is obtained by dividing TP by number of units of variable output. AP can be written as,

AP = TP/Units of variable factor (n)

RELATIONSHIP BETWEEN TP AP AND MP

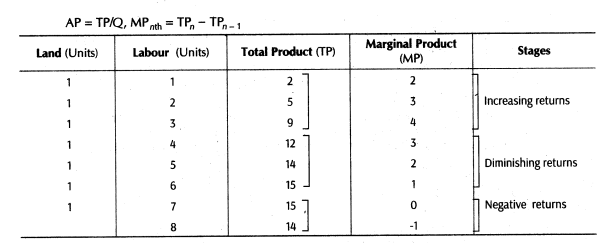

The relationship between TP and MP is explained through the Law of Variable Proportions. As long as the the TP increases at an increasing rate, the MP also increases. This goes on till MP reaches maximum. When TP increases at a diminishing rate, MP declines. This continues till the point where TP is at its highest. When TP reaches its maximum point, MP becomes zero. This concept can be explained with the help of the following schedule and diagram:

The above table shows fixed factor of production i.e. land and variable factor of production i.e. labor. The total product initially increases and marginal product decreases. But after applying 6 units of labor on the fixed factor land, it becomes maximum i.e. 15. Here the Marginal Product is zero. As 8 units of variable factor are applied with fixed factor land, the total product decreases and marginal product becomes negative.

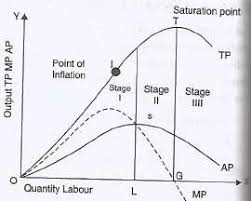

The diagram or curve shows three stages of production which are as follows:

- Stage I: MP > 0, AP is rising. Thus, MP > AP. This is increasing stage;

- Stage II. MP > 0, but AP is falling. Thus, MP < AP, but TP is increasing because MP > 0. This is diminishing stage.

- Stage III: MP < 0 and TP is falling. This is negative stage.

CONCLUSION

To conclude, the following findings are found:

- When TP increases at an increasing rate, MP increases.

- When TP increases at diminishing rate, MP declines

- When TP is maximum, MP is Zero

- When TP begins to decline, MP becomes negative

- When MP > AP, this means that AP is rising

- When MP = AP, this means that AP is maximum

- When MP < AP, this means that AP is falling