PRODUCT DIFFERENTIATION STRATEGY

In this post you will learn about Product differentiation strategy under Monopolistic competition

Product differentiation is the means used by a firm in a monopolistic competitive market with many firms selling similar products to differentiate its product from that of other firms. Product Differentiation strategy is adopted to capture more market share and to maximize profits.

Product differentiation can be real or fancied. It is real when there are slight differences in the product of the firm as in taste if it is a foodstuff, or in quality etc. It is fancied if the difference is just to attract the customer and not real differentiation, for example, differences in packaging, design etc. Firms in such markets engage in active advertising to attract customers and to market their products.

Product differentiation may take place in the form of:

1.Brand Name:

Products are known by their Brand names. Over the years certain

firms acquire goodwill in the market. Firm’s name itself becomes a brand name

for its product. Godrej cupboards, Phillips TV are some of the examples. Some

products get established in the market by the product’s name as in the case of

Colgate Tooth Paste, Parker Pen , Tata Tea etc.

2.Size:

Products are manufactured in different sizes. Economy, Family,

Large, Extra large are some of the sizes in which the products are available.

Certain firms may specialize in sizes like Family size or economy size. Thus the

Product is known in the market for its particular size.

3.Design:

Products could be differentiated on the basis of design.

Refrigerators, Cupboards, Scooters, Cars, are some of the products which are

considered by the buyers on the basis of design.

4.Color:

Color is one of the important factor on which goods are

differentiated. Textiles, Readymade Garments, Plastic Products, Automobiles,

are preferred by the Customer on the basis of their color.

5.Taste and Perfume:

Products like Confectioneries, toothpaste , soaps, cosmetics are

selected on the basis of taste or perfume

6.Good Salesmanship:

Customers may prefer the Products of a particular firm against

its rival firms simply because of good salesmanship, positive attitude,

approach and cooperation of the sales people.

7.After Sale Service:

Consumer Durable items have a warranty period during which free

service is offered. Services are offered thereafter on payment. Quality and

promotions of after sale service influence the customers while selecting the products.

EQUILIBRIUM/ PRICE AND OUTPUT DETERMINATION UNDER MONOPOLISTIC COMPETITION

A firm is said to be in equilibrium when it is incurring minimum costs and gaining maximum profits. Under monopolistic competition, the equilibrium is ascertained differently for industry and firm.

EQUILIBRIUM/ PRICE AND OUTPUT DETERMINATION FOR FIRM

For a firm, the equilibrium may be determined in both long run and short run.

SHORT RUN EQUILIBRIUM

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC.

CONDITIONS: The two conditions to be satisfied for the firm to be in equilibrium are as follows:

(1) MC = MR

(2) MC must cut MR from below.

Under monopolistic competition also, a firm will make the maximum profits when these two conditions are satisfied.

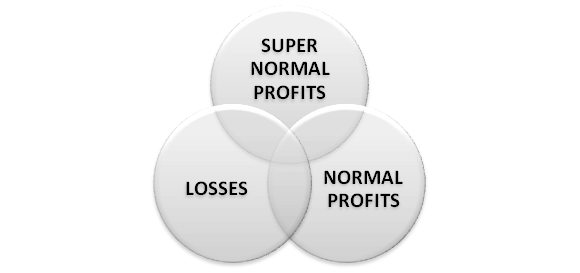

The firm may face any of three situations:

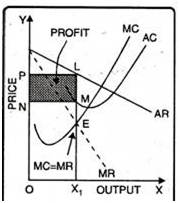

SUPER NORMAL PROFIT

Under monopolistic competition, a firm earns maximum profits or is in equilibrium when MC=MR and MC cuts MR from below. In the diagram the firm is in equilibrium at OX level of output and at the point E, at which MR and MC are equal and MC cuts MR from below.

The firm is earning super-normal profits or abnormal profits since average revenue is greater than average cost, i.e., AR > AC. The main reason for these abnormal profits is that, the other rival firms are not able to produce closely competitive substitutes. Hence, they are not able to attract consumers towards their product.

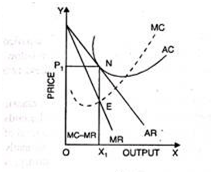

NORMAL PROFIT

If under monopolistic competition, the price of product is equal to AC, the firm will be earning normal profit. In Figure MC is equal to MR at point E. This is the equilibrium point. At equilibrium point, the equilibrium output is OX1 and price is OP1. At this point, AC is NX1 and AR is also NX1 i.e., AC=AR. Thus the firm will be earning only normal profits.

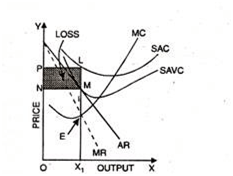

SUSTAINING LOSSES

It is also possible that the demand may not be favourable to firm under monopolistic competition, i.e., it may not be able to attract the consumers towards its product, if it fixes price equal to its SAC. But it is compelled to sell its product at the price which is less than even its short period average cost.

Hence, it may incur losses such firm, in the long-run may leave the industry, if it is not possible for it to change its demand relative to its cost conditions through product differentiation and advertisement. In figure the firm is in equilibrium at point E, where MC=MR. At this equilibrium level the output is OX1 at price OP. Corresponding to this, the average cost LX1 is greater than average revenue MX1, Since, revenue is less than cost, the firm will sustain losses equal to the shaded area PLMN.

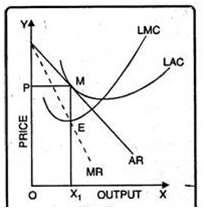

LONG RUN EQUILIBRIUM

Long period refers to that time period in which each firm can change its production capacity by changing the fixed as well as variable factors. New firms can enter the industry and old firms can exit it. Basically, the firms in the long run will get the normal profits.

If, the existing firms are making super normal profits, it will attract some of the new firms in the industry. The entry of new firms will result into over production which will have a depressing effect on price. Hence all the firms in the long run will get normal profits. In figure output is measured on X-axis whereas price on Y-axis. LAC is the long run average cost and LMC is the long fun marginal cost curve. The firm is in equilibrium because at point E, MC = MR. The equilibrium output is OX1 and price is OP. Since, at this equilibrium average revenue curve is tangent to long run average cost curve at point M; hence the firms are earning normal profits.

EQUILIBRIUM/ PRICE AND OUTPUT DETERMINATION FOR INDUSTRY

Under monopolistic competition, the word ‘group’ is used for industry. There is a difference between an industry and a group. An industry generally consists of firms which produce homogeneous product, whereas a group is composed of firms which produce a differentiated product. Thus group consists of a number of firms producing close substitutes. For example, shoe making firms like ‘Bata’, ‘Carona’, and ‘Liberty’ are a group.

Assumptions of equilibrium of industry:

(i) Demand and cost curves of all the firms are identical,

(ii) No firm can influence the price and output decisions of its rivals.

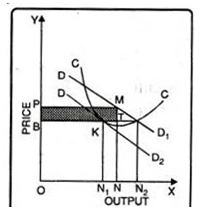

The Group Equilibrium is shown below with the help of following figure:

In the diagram, DD1 is the group demand curve and CC is the cost curve. Every firm would like to fix up OP price because at this price the difference between price and cost is the maximum and producer gets supernormal profit equal to PMTB. The other firms will be attracted to enter the market and now the market demand will be shared by a larger number of firms. In this situation demand curve will shift downwards and the new demand curve will be DD2.

The number of firms in the market will continue increasing till the new demand curve DD2 is tangent to the cost curve. In the Figure, at point ‘K’ demand curve is tangent to the cost curve. At this point firm will be earning only normal profit and this will be the equilibrium position of the firm. Thus under monopolistic competition, OB is the equilibrium price and ON is the equilibrium output.

ROLE OF PRODUCT DIFFERENTIATION IN DETERMINATION OF PRICE AND OUTPUT

Product differentiation as the basis for establishing a downward-falling demand curve was first introduced in economic theory by Sraffa.

Yet it was Chamberlin who elaborated the implication of product differentiation for the pricing and output decisions as well as for the selling strategy of the firm.

Chamberlin suggested that the demand is determined not only by the price policy of the firm, but also by the style of the product, the services associated with it, and the selling activities of the firm.

Thus Chamberlin introduced two additional policy variables in the theory of the firm:

- The product itself

- Selling activities.

The demand for the product of the individual firm incorporates these dimensions. It shows the quantities demanded for a particular style, associated services, offered with a specific selling strategy.

Thus the demand curve will shift if:

(a) The style, services, or the selling strategy of the firm changes;

(b) Competitors change their price, output, services or selling policies;

(c) Tastes, incomes, prices or selling policies of products from other industries change.

The effect of product differentiation is that the producer has some discretion in the determination of the price. He is not a price-taker, but has some degree of monopoly power which he can exploit. However, he faces the keen competition of close substitutes offered by other firms. Hence the discretion over the price is limited.

Product differentiation creates brand loyalty of the consumers and gives rise to a negatively sloping demand curve. Product differentiation, finally, provides the rationale of selling expenses. Product changes, advertising and salesmanship are the main means of product differentiation.