PERFECT COMPETITION

A Perfect Competition market is that type of market in which the number of buyers and sellers is very large, all are engaged in buying and selling a homogeneous product without any artificial restrictions and possessing perfect knowledge of the market at a time.

ACCORDING TO MRS. JOAN ROBINSON

“Perfect Competition prevails when the demand for the output of each producer is perfectly elastic.”

ACCORDING TO BOULDING

“A Perfect Competition market may be defined as a large number of buyers and sellers all engaged in the purchase and sale of identically similar commodities, who are in close contact with one another and who buy and sell freely among themselves.”

CHARACTERISTICS OF PERFECT COMPETITION

The perfect competitive market possesses following features:

Large number of buyers and Sellers

In a perfectly competitive market, there will be a large number of buyers and sellers.

Large number here denotes that the number of producers is so numerous that they cannot combine and influence the market price by their combined action and decisions. The individual action will not affect the market price because, the quantity offered by the individual producer will be so small when compared to the total quantity offered in the market, that the action of the individuals will be very insignificant and it cannot influence the market price. Output of a single firm may not influence the demand and price to a great deal in market as it is only a small percentage of overall output.

Similarly, on the part of the buyers, the number is so large that there are no possibilities for them to dictate conditions in the market and influence the price by altering the demand. The individual demand will be so small that it will be insignificant if there is any change. So the market price cannot be altered either by sellers or by buyers by their actions individually; nor are there possibilities for a few of them to combine.

In a perfectly competitive market, the individual firm is only a ‘Price taker’ and not ‘Price maker’. They cannot have a price policy of their own and will pay attention mostly to reduce the cost of production. They will adjust output to the market price.

Homogeneous Product

The second condition in the perfect market is that the commodity offered should be homogeneous and identical in all respects. The identity should be from the buyer’s angle. The buyers should feel that the products offered by different sellers are the same in quality, size, taste, etc., so that the product of different firms are perfect substitutes in the eyes of the buyers and the cross elasticity is infinite. If this is so, then a single seller cannot charge a higher price, as he will lose all his customers.

Free entry and exit conditions

The Third important condition in perfect competition is that there are no artificial restrictions either preventing the entry of new firms into the market or compelling the existing firms to continue. The firms have full liberty to choose either to continue or go out of the industry. Entry and exit of firms purely depend on economic considerations only.

Perfect knowledge on the part of buyers and sellers

The fourth condition is the existence of perfect knowledge on the part of buyers and sellers about market conditions. The buyers know in full about the commodity sold and the price prevailing in the market.

Perfect mobility of factors of production

The existence of perfect competition depends on perfect mobility of factors of production. The factor should be free to move from one use to another easily depending on the remuneration they get.

Absence of transport cost

In a perfectly competitive market, it is assumed that there are no transport costs. If transport costs are incurred, prices should be different in different sectors of the market.

Absence of Government or artificial restrictions

Lastly it is assumed that there are no restrictions from any quarters hindering the smooth functioning of perfect competition. There is no government control or restriction on supply, pricing, etc, and the price should be free to change in response to changes in demand supply conditions. If all these conditions are fulfilled, then the market can be termed perfect.

One Price of the Commodity

There is always one price of the commodity available in the market.

Independent Relationship between Buyers and Sellers

There should not be any attachment between sellers and purchasers in the market. In real life “Perfect Competition is a pure myth.”

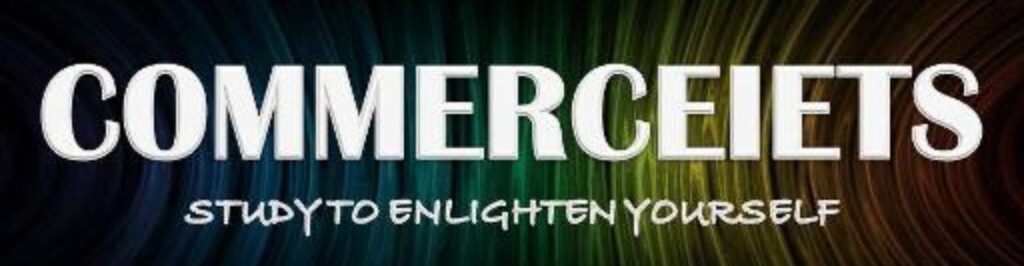

Revenue Curves

In perfect competition an individual firm is price taker, because the price is determined by the collective forces of market demand and supply which are not influenced by the individual. When price is the same for all units of a commodity, naturally AR (Price) will be equal to MR i.e., AR = MR.

In above figure, on the X-axis, quantity is taken whereas on Y-axis, there is revenue. At price OP, the seller can sell any amount of the commodity. In this case the average revenue curve is the horizontal line. The Marginal Revenue curve coincides with the Average Revenue.

It is because additional units are sold at the same price as before. In that case AR = MR.

PRICE AND OUTPUT DETERMINATION UNDER PERFECT COMPETITION OF INDUSTRY

Under perfect competition, the buyers and sellers cannot influence the market price by increasing or decreasing their purchases or output, respectively. The market price of products in perfect competition is determined by the industry. This implies that in perfect competition, the market price of products is determined by taking into account two market forces, namely market demand and market supply.

ACCORDING TO MARSHALL

“Both the elements of demand and supply are required for the determination of price of a commodity in the same manner as both the blades of scissors are required to cut a cloth.”

Market demand is defined as a sum of the quantity demanded by each individual organizations in the industry.

On the other hand, market supply refers to the sum of the quantity supplied by individual organizations in the industry.

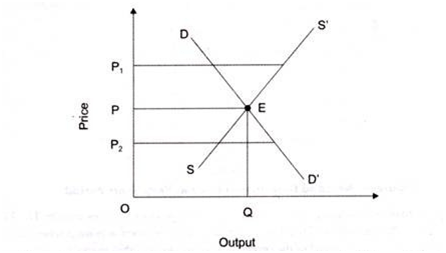

In perfect competition, the price of a product is determined at a point at which the demand and supply curve intersect each other. This point is known as equilibrium point as well as the price is known as equilibrium price. In addition, at this point, the quantity demanded and supplied is called equilibrium quantity.

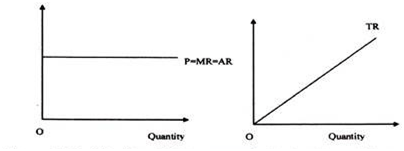

DEMAND UNDER PERFECT COMPETITION

Demand refers to the quantity of a product that consumers are willing to purchase at a particular price, while other factors remain constant. A consumer demands more quantity at lower price and less quantity at higher price. Therefore, the demand varies at different prices.

As shown in Figure, when price is OP, the quantity demanded is OQ. On the other hand, when price increases to OP1, the quantity demanded reduces to OQ1. Therefore, under perfect competition, the demands curve (DD’) slopes downward.

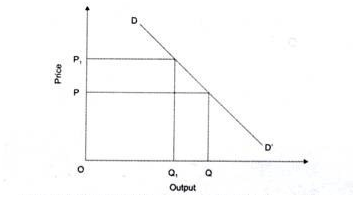

SUPPLY UNDER PERFECT COMPETITION

Supply refers to quantity of a product that producers are willing to supply at a particular price. Generally, the supply of a product increases at high price and decreases at low price.

In Figure, the quantity supplied is OQ at price OP. When price increases to OP1, the quantity supplied increases to OQ1. This is because the producers are able to earn large profits by supplying products at higher price. Therefore, under perfect competition, the supply curves (SS’) slopes upward.

EQUILIBRIUM UNDER PERFECT COMPETITION

In perfect competition, the price of a product is determined at a point at which the demand and supply curve intersect each other. This point is known as equilibrium point. At this point, the quantity demanded and supplied is called equilibrium quantity.

In Figure, it can be seen that at price OP1, supply is more than the demand. Therefore, prices will fall down to OP. Similarly, at price OP2, demand is more than the supply. Similarly, in such a case, the prices will rise to OP. Thus, E is the equilibrium at which equilibrium price is OP and equilibrium quantity is OQ.

PRICE AND OUTPUT DETERMINATION UNDER PERFECT COMPETITION OF FIRM

A firm is in equilibrium when it maximizes its profits. Hence, the output that offers maximum profit to a firm is the equilibrium output. When a firm is in equilibrium, there is no reason to increase or decrease the output.

In a competitive market, firms are price-takers. The reason being the presence of a large number of firms who produce homogeneous products. Therefore, firms cannot influence the price in their individual capacities. They have to follow the price determined by the industry.

Conditions for the equilibrium of a firm

To attain an equilibrium position, a firm must satisfy the following two conditions:

They must ensure that the marginal revenue is equal to the marginal cost (MR = MC).

- If MR > MC, the firm has an incentive to expand its production and sell additional units.

- If MR < MC, the firm must reduce the output since additional units add more cost than revenue.

- The firm gets maximum profits only when MR = MC.

- The MC curve must have a positive slope and cut the MR curve from below.

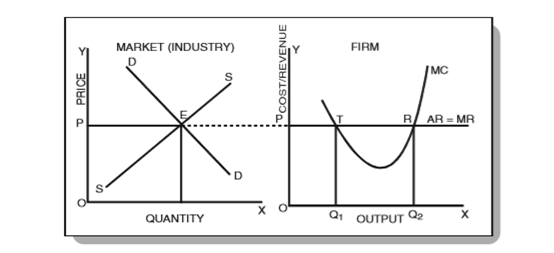

In Figure above, DD is the demand curve and SS is the supply curve. They equilibrate at point E and set the market price as OP. Under perfect competition, firms adopt OP as the industry price and consider the P-line as the demand curve or AR – average revenue curve (perfectly elastic at P).

Since all units are equally priced, the MR curve is a horizontal line and is equal to the AR line. Observe that the curve MC cuts the MR curve at two points – T and R. At point T, the MC curve cuts the MR curve from above whereas at point R it cuts the MR curve from below. Therefore, according to the conditions of equilibrium of a firm, point R is the point of equilibrium and OQ2 is the equilibrium level of output.

PRICE AND OUTPUT DETERMINATION UNDER SHORT RUN

Short period is the span of time so short that existing plants cannot be extended and new plants cannot be erected to meet increased demand. However, the time is adequate enough for producers to adjust to some extent their output to the increase in demand by overworking their fixed capacity plants. In the short run, therefore, supply curve is elastic.

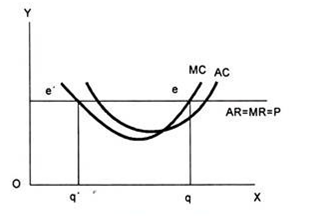

The average and marginal cost curves of the firm together with its demand curve determine equilibrium in short run.. Demand curve, in a perfectly competitive market, is also the average revenue curve and the marginal revenue curve of the firm. The marginal cost intersects the average cost at its minimum point. The U-shape of both the cost curves reflects the law of variable proportions operative in the short run during which the size of the plant remains fixed.

For the equilibrium of a firm the two conditions must be fulfilled:

(a) MR=MC: The marginal cost must be equal to the marginal revenue. However, this condition is not sufficient, since it may be fulfilled and yet the firm may not be in equilibrium. The above figure shows that marginal cost is equal to marginal revenue at point e’, yet the firm is not in equilibrium as Oq output is greater than Oq’.

(b) MC CUTS MR FROM BELOW: The second and necessary condition for equilibrium requires that the marginal cost curve cuts the marginal revenue curve from below i.e. the marginal cost curve be rising at the point of intersection with the marginal revenue curve.

Thus, a perfectly competitive firm will adjust its output at the point where its marginal cost is equal to marginal revenue or price, and marginal cost curve cuts the marginal revenue curve from below.

RETURNS IN SHORT RUN

The fact that a firm is in equilibrium does not imply that it necessarily earns supernormal profits. In the short-run equilibrium firms may earn supernormal profits, normal profits or may incur losses.

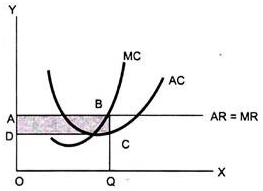

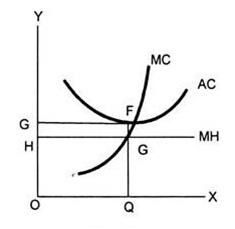

SUPER NORMAL PROFITS: Whether the firm makes supernormal profits, normal profits or incurs losses depends on the level of the average cost at the short run equilibrium. If the average cost is below the average revenue, the firm earns supernormal profits. The following figure illustrates that the average cost QC is less than average revenue QB, and the firm earns profits equal to the area ABCD.

LOSS: If the average cost is above the average revenue the firm makes a loss. The following figure shows that the Average cost QF is higher than QG average revenue and the firm is incurring loss equal to the shaded area EFGH. In this case the firm will continue to produce only if it is able to cover its variable costs. Otherwise it will close down, since by discontinuing its operations the firm is better off; it minimizes its losses. The point at which the firm covers its variable costs is called ‘the closing-down point’. If the price falls below or average costs rise, the firm does not cover its variable costs and is better off if it closes down.

PRICE AND OUTPUT DETERMINATION OR EQUILIBRIUM IN THE LONG RUN

The long run is a period of time long enough to permit changes in the variable as well as in the fixed factors. In the long run, accordingly, all factors are variable and non- fixed. Thus, in the long run, firms can change their output by increasing their fixed equipment. They can enlarge the old plants or replace them by new plants or add new plants.

Moreover, in the long run, new firms can also enter the industry. On the contrary, if the situation so demands, in the long run, firms can diminish their fixed equipments by allowing them to wear out without replacement and the existing firm can leave the industry.

Thus, the long run equilibrium will refer to a situation where free and full scope for adjustment has been allowed to economic forces. In the long run, it is the long run average and marginal cost curves, which are relevant for making output decisions. Further, in the long run, average variable cost is of no particular relevance. The average total cost is of determining importance, since in the long run all costs are variable and none fixed.

SUPER NORMAL PROFITS

In the short run a firm under perfect competition is in equilibrium at that output at which marginal cost equals price or Marginal Revenue. This is equally valid in the long run. But, in the long run for a perfectly competition firm to be in equilibrium, besides marginal cost being equal to price, price must also be equal to average cost. If the price is greater than the average cost, the firms will be making supernormal profits.

NORMAL PROFITS

Lured by these supernormal profits, new firms will enter the industry and these extra profits will be competed away. When the new firms enter the industry, the supply or output of the industry will increase and hence the price of the output will be forced down. The new firms will keep coming into the industry until the price is depressed down to average cost, and all firms are earning only normal profits.

LOSSES

On the other hand, if the price happens to be below the average cost, the firms will be incurring loses. Some of the existing firms will quit the industry. As a result, the output of the industry will decrease and the price will rise to equal the average cost so that the firms remaining in the industry are making normal profits. Hence, in the long run, firms need not be forced to produce at a loss since they can leave the industry, if they are having losses. Thus, for a perfectly competitive firm to be in equilibrium in the long run, price must equal marginal and average cost.

Now when average cost curve is falling, marginal cost curve is below it, and when average cost curve is rising, marginal cost curve must be above it. Hence, marginal cost can be equal to the average cost only at the point where average cost curve is neither falling nor rising, i.e. at the minimum point of average cost curve. Therefore, it is at the point of minimum average cost curve, and the two are equal there.

CONDITIONS FOR EQUILIBRIUM

The conditions for long run equilibrium of perfectly competitive firm can be written as:

Price = Marginal Cost = Minimum Average Cost.

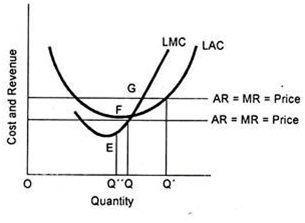

The conditions for the long run equilibrium of the firm under perfect competition can be easily understood from the diagram, where LAC is the long run average cost curve and LMC in the long run marginal cost curve. The firm under perfect competition cannot be in long run equilibrium at price OP’, because though the price OP’ equals MC at G (i.e., at output OQ) but it is greater than the average cost at this output and, therefore, the firm will be earning supernormal profits.

Since all the firms are assumed to be identical, all would be earning supernormal profits. Hence, there will be attraction for the new firms to enter the industry. As a result, the price will be forced down to the level Op at which price, the firm is in equilibrium at F and is producing OQ” output.

At point F or equilibrium output OQ”, the price is equal to average cost, and hence the firm will be earning only normal profits. Therefore, at price OP, there will be no tendency for the outside firms to enter the industry. Hence, the firm will be in equilibrium at OP price and OQ output.

On the contrary, a firm under perfect competition cannot be in the long run equilibrium at price OP”. Though price OP” is equal to marginal cost at point E, or at output OQ” but price OP” is lower than the average cost at this point and thus the firm will be incurring losses.

Since all the firms in the industry are identical in respect of cost curves, all would be incurring losses. To avoid these losses, some of the firm will leave the industry. As a result, the price will rise to OP, where again all firms are making normal profits. When the price OP is reached, the firms would have no further tendency to quit.

Thus, to conclude that at price OP, the firm under perfect competition is in equilibrium in the long run when:

Price = MC = Minimum AC

Now, at price OP, besides all firms being in equilibrium at output OQ, the industry will also be in equilibrium, since there will be no tendency for new firms to enter or the existing firms to leave the industry, because all will be earning normal profits. Thus, at OP price, full equilibrium, i.e. equilibrium of all the individual firms and also of the industry, as a whole, is achieved in the long run under perfect competition.