TRADITIONAL THEORY OF COST

Traditional theory distinguishes between the short run and the long run. The short run is the period during which some factors is fixed; usually capital equipment and entrepreneurship are considered as fixed in the short run.

The long run is the period over which all factors become variable.

SHORT-RUN TRADITIONAL THEORY OF COST

According to the traditional theory of the costs, the costs are divided into three types:

- Total Cost

- Average Cost

- Marginal Cost

TOTAL COST

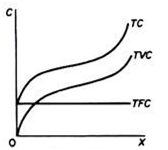

Total cost is the total expenditure incurred by a firm during the production process. Total cost will change with the change in the ratio of output to input. Such changes may be the result of the changes in the efficiency of conversion process or changes in the prices of inputs. Total cost is a positively sloped curve.

Total cost to a producer for the various levels of output is the sum of total fixed cost and total variable cost, i.e.,

TC = TFC + TVC.

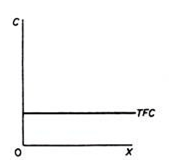

TOTAL FIXED COST: Total fixed costs refer to those costs which are unable to vary. For example: land, buildings, machinery etc. Even the output is zero fixed costs will be there. Because, this cannot be variable with respect to the level of production. So, it is also called invariable cost. Since fixed costs are fixed or rigid it can be represented through a curve having horizontal shape to output axis. This can be shown with the help of following diagram:

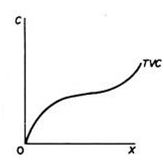

TOTAL VARIABLE COST: Variable cost is incurred on the employment of variable factors like raw materials, direct labour, power, fuel, transportation, sales commission, depreciation charges associated with wear and tear of assets, etc. It varies directly with output.The curve of variable cost can be shown as follows:

From the curves of fixed cost and variable costs, the total cost can be derived as follows:

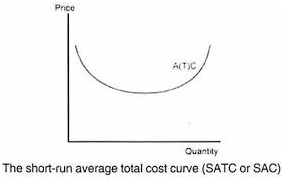

AVERAGE COST

Average total cost is the sum of the average fixed cost and average variable cost. Alternatively, ATC is computed by dividing total cost by the number of units of output.

Therefore,

ATC or AC = AFC + AVC

=TC/Q

Average cost is also known as unit cost, as it is cost per unit of output produced. It can be shown as follows:

Average cost is inclusive of Average Fixed Cost and Average Variable Cost.

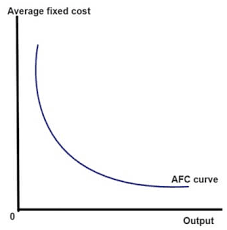

AVERAGE FIXED COST: AFC is the average of total fixed costs. AFC can be obtaining by dividing the total fixed cost by total quantity of output each time produced. Mathematically,

AFC = TFC /quantity

TFC will be always fixed. So AFC will reduce and never reaches zero. Its curve is as follows:

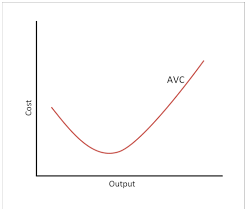

AVERAGE VARIABLE COST: AVC is the average of total variable cost. It can be find out by using the following formula.

AVC = TFC / quantity

AVC curve will be a ‘U’ shaped which is showing that when the output is raises the cost will decline, but after a certain level the cost starts to increases. That is why due to the variable proportion.

WHY AC IS U SHAPED?

In the short-run average cost curves are of U-shape. It means, initially it falls and after reaching the minimum point it starts rising upwards. It can be on account of the following reasons:

1. BASIS OF AVERAGE FIXED COST AND AVERAGE VARIABLE COST

Average cost is the aggregate of average fixed cost and average variable cost (AC = AFC + AVC). To begin with, as production increases, initially the average fixed cost and average variable cost falls. But after a minimum point, average variable cost stops falling but not the average cost. It is due to this reason that average variable cost reaches the minimum before AC.

The point, where AC is minimum is called the optimum point. After this point, AC begins to rise upward. The net result is the increase in AC. Therefore, it is only due to the nature of AFC and AVC that AC first falls, reaches minimum and afterwards starts rising upward and hence assume the U-shape.

2. BASIS OF THE LAW OF VARIABLE PROPORTION

The law of variable proportion also results in U-shape of short run average cost curve. If in the short period variable factors are combined with a fixed factor, output increases in accordance with the law of variable proportions. In other words, the law of ‘Increasing Returns’ applies.

Similarly, if employ more and more variable factors are employed with fixed factors the law of Diminishing Returns is said to apply. Thus, it is due to the law of variable proportions that the average cost curve assumes the shape of U.

3. INDIVISIBILITIES OF THE FACTORS

Another reason due to which the average cost curve forms U-shape is the indivisibilities of factors. When in the short-run a firm increases its production due to indivisibilities of fixed factors, it gets various internal economies. It is these economies which cause the average cost curve to fall in the initial stage. Generally, there are three types of internal economies which help to bring down the cost viz., technical economies, marketing economies and managerial economies.

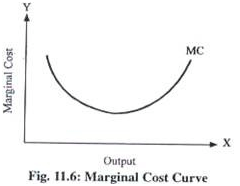

MARGINAL COST

It is the addition to total cost required to produce one additional unit of a commodity. It is measured by the change in total cost resulting from a unit increase in output. For example, if the total cost of producing 5 units of a commodity is Rs. 100 and that of 6 units is Rs. 110, then the marginal cost of producing 6th unit of. Commodity is Rs. 110 – Rs. 100 = Rs. 10. The formula for marginal cost is

MCn =TCn –TCn-1,

It means that marginal, cost of ‘n’ units of output (MCn) can be obtained by subtracting the total cost of production of ‘n-l’ units (TCn-1) from the total cost of production of ‘n’ units (TCn). Alternatively, marginal cost can be expressed as

MC=∆TC/∆Q.

Here, ∆TC stands for change in total cost and ∆Q stands for change in total output.

This can be shown as follows:

LONG RUN COSTS OF TRADITIONAL THEORY

In the long run all factors are assumed to become variable. Long-run cost curve is a planning curve, in the sense that it is a guide to the entrepreneur in his decision to plan the future expansion of his output. The long-run average-cost curve is derived from short-run cost curves.

The long run costs are categorised as follows:

- Long run total cost

- Long run average cost

- Long run marginal cost

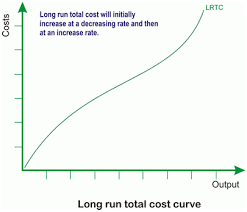

LONG RUN TOTAL COST

Long run Total Cost (LTC) refers to the minimum cost at which given level of output can be produced. According to Leibhafasky, “the long run total cost of production is the least possible cost of producing any given level of output when all inputs are variable.” LTC represents the least cost of different quantities of output. LTC is always less than or equal to short run total cost, but it is never more than short run cost.

This can be shown as follows:

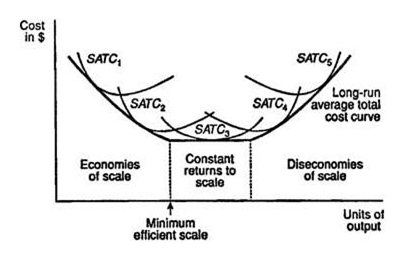

LONG RUN AVERAGE COST

Long run Average Cost (LAC) is equal to long run total costs divided by the level of output. The derivation of long run average costs is done from the short run average cost curves. In the short run, plant is fixed and each short run curve corresponds to a particular plant. The long run average costs curve is also called planning curve or envelope curve as it helps in making organizational plans for expanding production and achieving minimum cost.

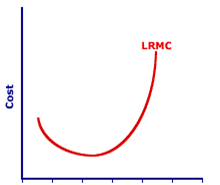

LONG RUN MARGINAL COST

Long run Marginal Cost (LMC) is defined as added cost of producing an additional unit of a commodity when all inputs are variable. This cost is derived from short run marginal cost. On the graph, the LMC is derived from the points of tangency between LAC and SAC.