PROFIT VOLUME RATIO

The Profit Volume Ratio shows percentage of contribution to the sales value i.e. margin as percentage of sales out of it; the fixed cost is met and there is a profit. It is one of the tools used in marginal costing.

The Profit Volume (P/V) Ratio is the measurement of the rate of change of profit due to change in volume of sales. It is one of the important ratios for computing profitability as it indicates contribution earned with respect of sales.

Contribution = Sales Value × P/V Ratio

P/V ratio is a relative ratio. It cannot be adopted independently. If it is studied in an isolated way, it will not give much information. As fixed costs are not relevant in the calculation of P/V ratio, erroneous conclusions may be arrived.

FEATURES OF PROFIT VOLUME RATIO (P/V RATIO)

• It is the ratio of contribution to sales.

• This ratio is usually expressed in percentage.

• The higher the PV Ratio, the better it is.

• It indicates the effect on profit for a given change in the sales.

• It measures the profitability of each product, process, operation etc.

• It facilitates managerial decision making.

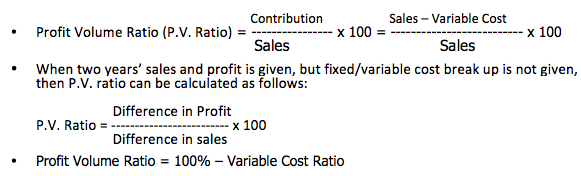

CALCULATION

The Profit Volume Ratio can be calculated as follows:

- PV Ratio = (Contribution/ Sales) x 100

- PV Ratio = (Changes in Profit/ Changes in Sales) x 100

- PV Ratio = 100 – Variable Cost Ratio

Based on the same the following formulas can be derived:

- Total Sales = Contribution / PV Ratio

- Desired Sales (in units) = Fixed Cost + Desired Profit / Contribution per unit

- Desired sales (in Rs.) = Fixed Cost + Desired Profit/ PV Ratio

WAYS TO IMPROVE PV RATIO

P/V Ratio can be improved by:

- By reducing variable cost, or

- By increasing the selling price, or

- By improving Sales mix

- Reducing direct and variable costs by effectively utilizing men, machines and materials.

- Switching the production to more profitable products showing a higher P/V ratio.

USES OF PROFIT-VOLUME RATIO

P/V ratio is one of the most important ratios to watch in business. It is an indicator of the rate at which profit is being earned. A high Profit volume ratio indicates high profitability and a low ratio indicates low profitability in the business. The profitability of different sections of the business, such as sales areas, classes of customers, product lines, methods of production, etc., may also be compared with the help of profit-volume ratio. The PV ratio is also used in making the following type of calculations:

- Calculation of break-even point.

- Calculation of profit at a given level of sales.

- Calculation of the volume of sales required to earn a given profit.

- Calculation of profit when margin of safety is given

- Calculation of the volume of sales required to maintain the present level of profit if selling price is reduced.

- To determine the variable cost for any volume of sales,

- To fix the selling prices,

- To locate the break-even point and margin of safety,

CONCLUSION

As P/V ratio indicates the rate of profitability; any improvement in this ratio without increase in fixed costs, would result in higher profits. As a note of caution, erroneous conclusions may be drawn by mere reference to P/V ratio and, therefore, this ratio should not be used in isolation.

P/V ratio is the function of sales and variable costs. Thus it can be improved by widening the gap between sales and variable cost.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN

https://www.linkedin.com/in/kajal-mahajan-7549b2197/