LAW OF CONSTANT RETURNS

The law of constant returns is also empirically valid and operates in the transitional stage between the Law of Diminishing Returns as well as The Law of Increasing Returns.

According to the Law, when in order to increase output, units of labour and capital are increased; output and cost also increase in the same proportion.

ACCORDING TO MARSHALL

“If the actions of law of increasing and diminishing returns are balanced we have the law of constant returns.”

ACCORDING TO STIGLER

“The law of constant returns states that when all the productive services are increased in a given proportion, the product is increased in the same proportion.”

ASSUMPTIONS OF LAW OF CONSTANT RETURNS

This law is based on the following assumptions:

- Some factors (labor and capital) are assumed to be variable.

- There is no increase in the price of raw materials.

- There is no change in the price of factors of production.

- The supply of various factors for an industry should be perfectly elastic.

- All units of variable factors of production are equally efficient.

EXPLANATION OF THE LAW

The law of constant returns can be explained in the forms:

(A) Law of Constant Returns and

(B) Law of Constant Costs.

(A) Law of Constant Returns:

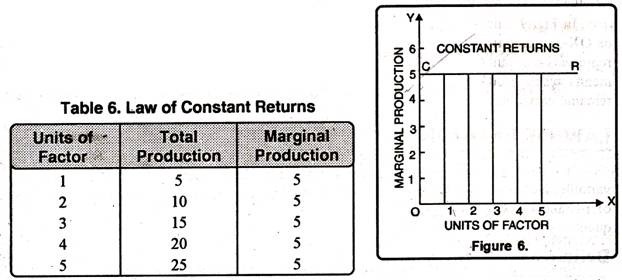

The law of constant returns can be illustrated with the help of following Table. This table indicates that production will be made by using different units of labour and capital.

Table reveals that production increases in the same ratio in which the factors of production are increased. When the factors of production are doubled, production is doubled from 5 meters to 10 meters. Likewise, it increases to 10, 15, 20, and 25 respectively. In this stage marginal and average production remains constant.

As seen in figure factors of production and marginal production are represented along OX-axis and OY-axis respectively. Curve CR is parallel to OX.

This shows that with the increase in the factors of production, marginal production increases in the same quantity that is 5 per unit. It means that production is increasing in the same ratio in which factors of production are increasing.

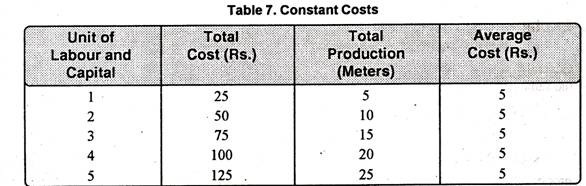

(B) Law of Constant Costs:

Law of Constant Returns can also be explained in term of costs. According to it average and marginal cost of production remain constant as a result of additional application of the variable factor along with the fixed factor of production. It means, whether production increases or decreases, no change occurs in average cost. The law of constant cost can be elaborated with the help of table below.

Table 7 shows that total production and total cost increase in the same proportion. As a result, there is no change in average cost due to increase in production. Average cost remains Rs. 5.00 per unit.

APPLICATION OF THE LAW

For the application of this law, the following points are very important:

- This law is applicable in those sectors where human and natural factors play their role, for example, in industry making blankets, pure natural wool is used while blankets are prepared in the presence of human factors.

- Such factors where economies of human and natural factors are presented which counter balanced each other and productivity is provided with constant rate.

- This law is more applicable in such sectors where labor’s role is greater than other factors of production. The law of constant returns operates by increasing the units of labor force.