CONTRACT COSTING

Contract costing is also known as Terminal Costing.

It is one form of application of the principles of job order costing. Contract Costing is a type of costing used in constructional activities such as construction of buildings, roads, bridges etc. The person who takes contract for a price is called the Contractor and the person from whom it is taken is called the Contractee.

ACCORDING TO CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS, LONDON

“Contract costing is a form of specific order costing in which costs are attributed to individual contracts.”

In contract costing each contract is treated as a cost unit and costs are ascertained separately for each contract. Usually, there is a separate account for each contract.

FEATURES OF CONTRACT COSTING

EACH CONTRACT ITSELF A COST UNIT

In contract costing, every contract is a cost unit. Each contract has its own list of expenses and incomes.

WORK IS EXECUTED AT CUSTOMERS SITE

In case of contract costing, the work is performed at a place which is related to the consumer. For example: The building is constructed on the land of the consumer.

THE EXISTENCE OF SUB CONTRACT

Sometimes the contractor enters into contracts with another contractor to give a portion of work undertaken by him. In such cases the work performed by the subcontractor s forms a direct charge to the contract concerned. Sub contract cost will be shown on the debit side of the contract account.

Sub-contracting may be necessary under the following circumstances:

- Work of a specialized nature for which facilities are not internally available within the concern is offered to a sub-contractor.

- It may be advantageous to get a part or component from outside, if it is costlier to manufacture it.

- Consideration of opportunity cost; the management may not like to invest capital which may be utilized for other more profitable lines.

- The capacity of the firm may be limited and in order to keep time schedule, work may be speeded by offering it to sub-contractors.

WORK IN PROGRESS

It is the unfinished contract at the end of the accounting period and it includes amount of work certified and amount of work uncertified. Work in progress is an asset, shown in the balance sheet by deducting there from any advance received from the contractee.

WORK CERTIFIED

The sales value of work completed as certified by the architect is known as ‘work certified’. In the case of contracts of long duration, the amount payable by the customer to the contractor is based on the sales value of work done as certified by the architect. At the end of the financial year, the total sales value of work done and certified by the architect is credited to the contract account.

PROFIT ON INCOMPLETE CONTRACT

At the end of an accounting period it may be found that certain contracts which have been completed while others are still in process and will be completed in the coming years. The profit on completed contracts may be safely taken to the credit of the profit and loss account. In the case of incompleted contracts there are unforeseen contingencies which may lead to heavy fluctuations in costs and profit. At the same time it does not also seem desirable to consider the profits only on completed contracts and ignore completely incomplete ones as this may result in heavy fluctuations in the future for profit from year to year. If profit or loss is not shown in the intermittent years for the work in progress, contract will show high figure of profit in the year of completion and reverse may be the case in the year in which a large number of contracts remain incomplete. Therefore, profits on incomplete contracts should be considered, of course, after providing adequate sums for meeting unknown contingencies.

WORK UNCERTIFIED

It means work which has been carried out by the contractor but has not been certified by the architect. Sometimes, work which is complete remains uncertified at the end of the financial year. The reasons for the same may be

- Work not sufficient enough to be certified

- Work has not reached the stipulated stage to qualify for certification

It is always valued at cost and credited to the contract account.

RETENTION MONEY

Regardless of the amount of work certified, the contractor is paid a specified percentage of the same and the balance is held or retained by the contractee. This is because of the fact that the contractee has to safe guard himself against any contingency arising from the non fulfillment of the terms of the contract by the contractor. The unpaid balance of work certified or the amount held back or retained by the contractee is known as ‘retention money’.

SUB CONTRACT

Sometimes the contractor enters into contracts with another contractor to give a portion of work undertaken by him. In such cases the work performed by the subcontractor s forms a direct charge to the contract concerned. Sub contract cost will be shown on the debit side of the contract account.

ESCALATION CLAUSE

This is clause which is provided in the contract to cover up any increase in the price of the contract due to increase in the prices of raw material or labour or in the utilization of any other factors of production. If material and labour utilization exceeds a particular limit, the customer agrees to bear the additional cost occasioned by excessive utilization. Here, the contractor has to satisfy the customer that excessive utilization is not the result of decreased efficiency.

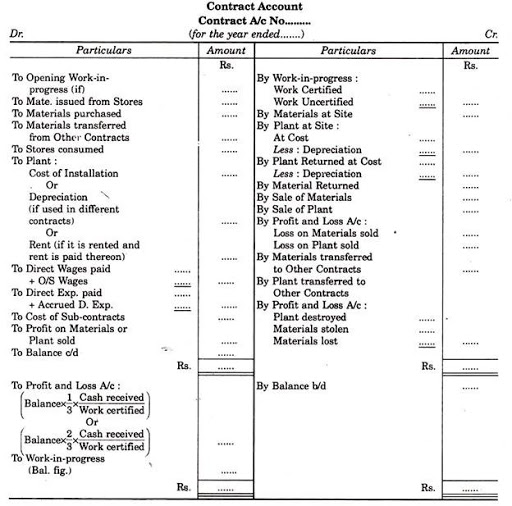

PREPARATION OF CONTRACT ACCOUNT

A contract account is a nominal account in nature. It is prepared to find out the cost of contract and to know profit or loss made on the contract. A contractor may undertake a number of contracts at a time. For each contract a separate account is opened. In the contract account all direct cost such as material, labour and other direct expenses incurred during an accounting period are debited and the indirect expenses are apportioned on an equitable basis. The differences between the two sides are known as Notional profit or notional loss.

TYPES OF CONTRACTS

Generally there are three types of contracts:

- Fixed price contracts: Under these contracts both parties agree to a fixed contract price.

- Fixed price contract with Escalation clause

- Cost plus contract: Under this contract no fixed price could be settled for a contract.

TREATMENT OF PROFIT ON INCOMPLETE CONTRACTS

At the end of an accounting period it may be found that certain contracts which have been completed while others are still in process and will be completed in the coming years. The profit on completed contracts may be safely taken to the credit of the profit and loss account. In the case of incompleted contracts there are unforeseen contingencies which may lead to heavy fluctuations in costs and profit. At the same time it does not also seem desirable to consider the profits only on completed contracts and ignore completely incomplete ones as this may result in heavy fluctuations in the future for profit from year to year. If profit or loss is not shown in the intermittent years for the work in progress, contract will show high figure of profit in the year of completion and reverse may be the case in the year in which a large number of contracts remain incomplete. Therefore, profits on incomplete contracts should be considered, of course, after providing adequate sums for meeting unknown contingencies.

There are no hard and fast rules regarding calculation of the figures for profit to be taken to the credit of profit and loss account. However, the following rules may be followed:

(i) Profit should be considered in respect of work certified only, work uncertified should always be valued at cost.

(ii) No profit should be taken into consideration if the amount of work certified is less than 1/4th of the contract price because in such a case it is not possible to foresee the future clearly.

(iii) If the amount of work certified is 1/4th or more but less than 1/2 of the contract price, 1/3rd of the profit disclosed as reduced by the percentage of cash received from the contractee, should be taken to the profit and loss account or

Profit =1/3 x Notional Profit x {Cash received / Work certified}

The balance be allowed to remain as a reserve.

(iv) If the amount of work certified is 1/2 or more of the contract price, 2/3rd of the profit disclosed, as reduced by the percentage of cash received from the contractee, should be taken to the profit and loss account.

Profit= 2/3 x Notional Profit x {Cash received / Work certified}

The balance should be treated as reserve.

(v) In case the contract is very much near to completion, if possible the total cost of completing the contract should be estimated. The estimated total profit on the contract then can be calculated by deducting the estimated cost from the contract price. The profit and loss account should be credited with that proportion of total estimated profit on cash basis, which the work certified bears to the total contract price.

Profit=Estimated total profit x {Work certified / Contract price}

(vi) The whole of loss, if any, should be transferred to the profit and loss account.

That part of the profit which is not credited to the profit and loss account is treated as a reserve against contingencies and is deducted from the amount of work-in-progress for balance sheet purpose. It is carried down as a credit balance in the contract account itself, the work-in-progress being represented by the debit balance in the contract account.

The treatment of profit on incomplete contract will be computed as per specific instruction of problem. If there is no specific instruction then above rules should be applied.

COST PLUS CONTRACT

Cost plus contract is a contract in which the value of the contract is ascertained by adding a certain percentage of profit over the total cost of the work. This is used in case of those contracts whose exact cost cannot be correctly estimated at the time of undertaking a work. The profit to be paid to the contractor may be a fixed amount or it may be a particular percentage of cost or capital employed. These type of contracts are undertaken for production of special articles not usually manufactured and is generally employed, when Government happens to be a contractee. Generally, in such contract, contractor and contractee have clear agreement about the items of cost to be included, type of material to be used, labour rates for different grades, normal wastages to be permitted and the rate or amount of profit.

Advantage of cost plus contract

- Cost plus contract ensures that a reasonable profit accrues to the contractor even in risky projects.

- It simplifies the work offering tenders and quotations.

- It provides escalation clauses and thus covers the contractor from fluctuations in price and utilisation of elements of production.

- The customer is assured of paying only reasonable amount of profit.

- The customer has the right to conduct cost audit so that he can ensure that he is not being cheated by the contractor.

Disadvantages of cost plus contract system

Inspite of the advantages mentioned above cost plus contract system has the following disadvantages:

- Since the contractor is assured of profit margin, he may not take initiative for cost reduction by affecting economies of production and reducing wastages.

- The ultimate price to be paid by the customer cannot be exactly ascertained until the work is completed and this creates delay in preparing purchase budget by the customer.

- The customer has to pay not only the resultant high cost but also the resultant high profit. Thus, customer has to pay substantially for lack of proper attitude (towards cost and efficiency) on the part of contractor.