Calculation of Profits in Contract Costing

The contracts may be complete or incomplete contracts. Profits are calculated in both cases differently which is as follows:

ASCERTAINMENT OF PROFITS ON COMPLETED CONTRACTS

Profit on Completed Contracts: In case of contracts completed during the accounting year, the contract price, whether payable in lump sum on the completion of contract or payable by instalments, all be debited to the Contractée’s Personal Account and credited to the Contract Account. The difference between the total of the two sides of Contract Account shall be transferred to Profit the Loss Account of the contractor by way of profit or loss.

Sometimes, under the terms of the agreement, the contractor undertakes to rectify the defects, if any, in the contract work which may arise during a specified period (known as Maintenance Period) after the date of the completion of the contract. The amount of profit or loss on contracts in such a case should be scertained only after making a sufficient provision for cost of maintenance expected to be incurred during be maintenance period.

The ascertainment of profits on completed contracts in contract costing involves determining the actual profit earned on a specific contract once it has been completed. It is an essential process in evaluating the financial performance of a project and assessing the profitability of a contractor’s operations. Here are the key steps involved:

- Cost Allocation: Calculate the total costs incurred in executing the contract. This includes direct costs, such as labor, materials, subcontractor expenses, and equipment, as well as indirect costs, such as overhead expenses and administrative costs. Proper allocation of costs to the specific contract is crucial to accurately determine the profitability.

- Revenue Recognition: Identify the total revenue generated from the contract, which may include progress billings, milestone payments, or final payment upon completion. Ensure that all relevant revenue is correctly accounted for and attributed to the specific contract.

- Adjustments: Make any necessary adjustments to the costs or revenue recognized during the contract period. This may involve accounting for changes in scope, variations, or any other contract amendments that impact the overall financials. Adjustments may also include accounting for claims, warranties, or penalties, if applicable.

- Profit Calculation: Subtract the total costs allocated to the contract from the total revenue recognized to obtain the gross profit for the completed contract. The gross profit represents the financial gain or loss resulting from the project.

- Profit Margin Analysis: Evaluate the gross profit as a percentage of the total revenue to determine the profit margin on the completed contract. This metric provides insights into the profitability and efficiency of the project execution.

- Comparison and Analysis: Compare the actual profit earned on the completed contract with the estimated or targeted profit initially set for the project. Analyze the reasons for any variances and assess the effectiveness of cost control measures, pricing strategies, and project management practices.

- Reporting and Documentation: Document the results of the profit ascertainment process in financial reports, project evaluations, or management reviews. These reports provide crucial information for decision-making, performance assessment, and future contract bidding or pricing strategies.

The ascertainment of profits on completed contracts in contract costing helps contractors assess the financial success of their projects, identify areas for improvement, and inform future business decisions. It allows for a comprehensive evaluation of the financial performance of individual contracts, as well as overall profitability at the project or company level.

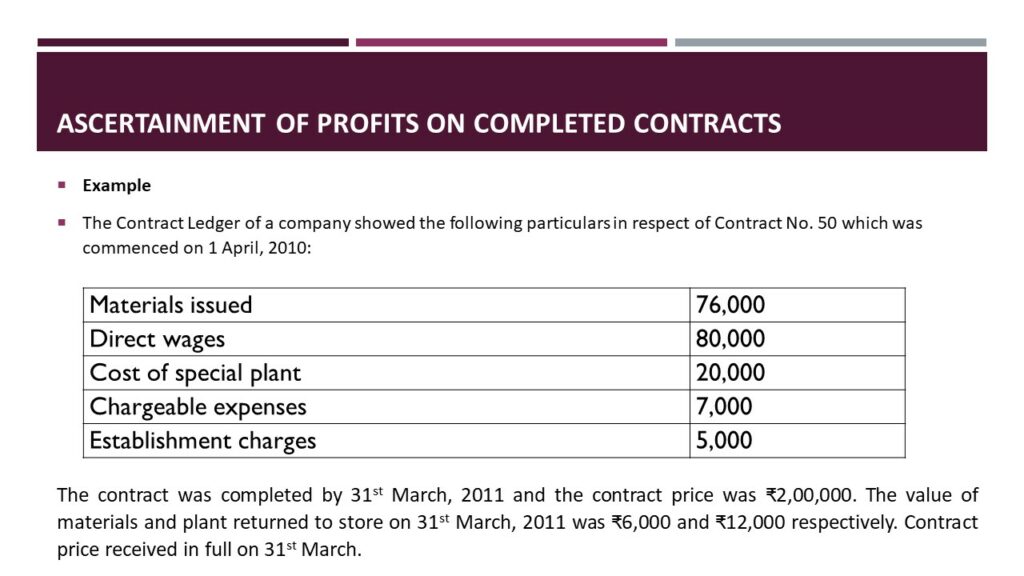

Example

The Contract Ledger of a company showed the following particulars in respect of Contract No. 50 which was commenced on 1 April, 2010:

| Materials issued | 76,000 |

| Direct wages | 80,000 |

| Cost of special plant | 20,000 |

| Chargeable expenses | 7,000 |

| Establishment charges | 5,000 |

The contract was completed by 31st March, 2011 and the contract price was ₹2,00,000. The value of materials and plant returned to store on 31st March, 2011 was ₹6,000 and ₹12,000 respectively. Contract price received in full on 31st March.

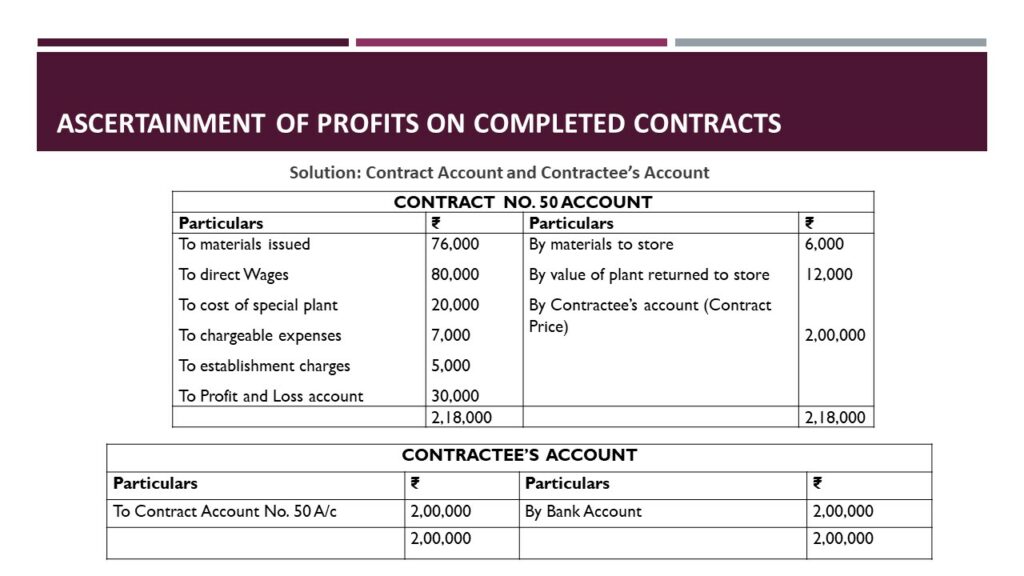

Solution: Contract Account and Contractee’s Account

| CONTRACT NO. 50 ACCOUNT | |||

| Particulars | ₹ | Particulars | ₹ |

| To materials issued To direct Wages To cost of special plant To chargeable expenses To establishment charges To Profit and Loss account | 76,000 80,000 20,000 7,000 5,000 30,000 | By materials to store By value of plant returned to store By Contractee’s account (Contract Price) | 6,000 12,000 2,00,000 |

| 2,18,000 | 2,18,000 | ||

| CONTRACTEE’S ACCOUNT | |||

| Particulars | ₹ | Particulars | ₹ |

| To Contract Account No. 50 A/c | 2,00,000 | By Bank Account | 2,00,000 |

| 2,00,000 | 2,00,000 | ||

ASCERTAINMENT OF PROFITS ON INCOMPLETE CONTRACTS

As a rule, profits on incomplete contracts should not he take credit for. A number of arguments are given against the calculation of profits on incomplete contracts. the anticipation of profits is against the general accounting principles. Secondly, the true profit on a contract cannot be ascertained until a contract is finished since a contract which appears to be profitable in its early stages may finally result into a loss on account of unexpected losses. Lastly, income tax will be paid profits a at an earlier date than would otherwise be necessary.

But it is counter-argued that by including profit on incomplete contracts in the Profit and Loss Account, undue fluctuations in the profits and dividends paid can be avoided. Secondly, some contracts may ale several years to complete and if profits are calculated on such contracts on completion, it shall appear the entire amount of profit has been earned in one year, which is not correct. Therefore, profits on complete contracts should be calculated very cautiously and only a portion of it may be credited to Profit and Loss Account.

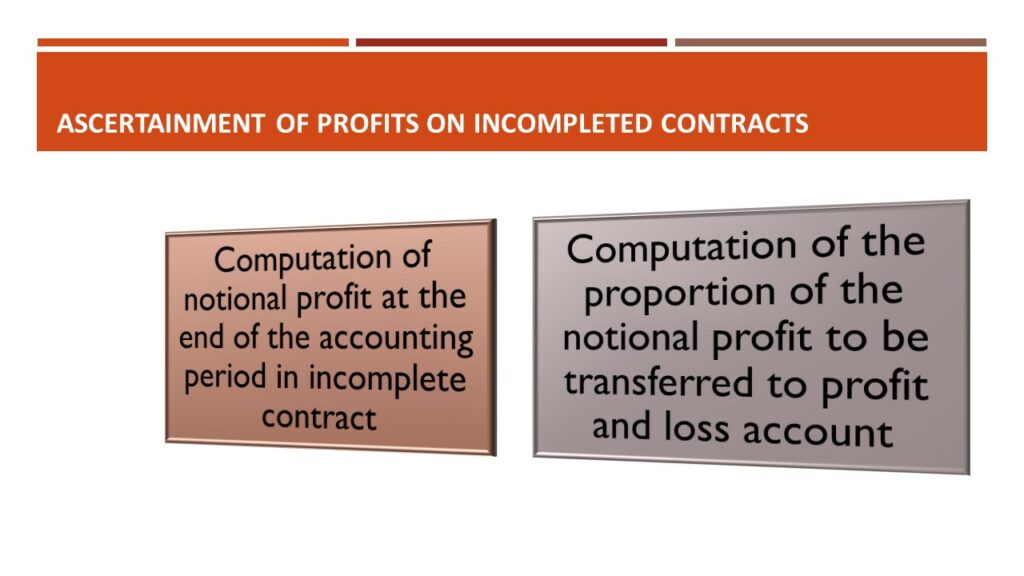

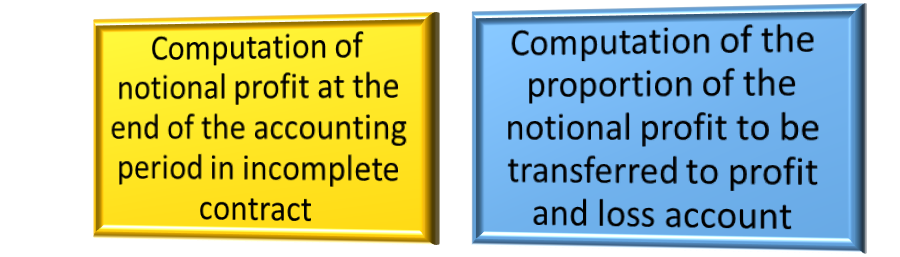

The computation of profit on incomplete contracts has two aspects:

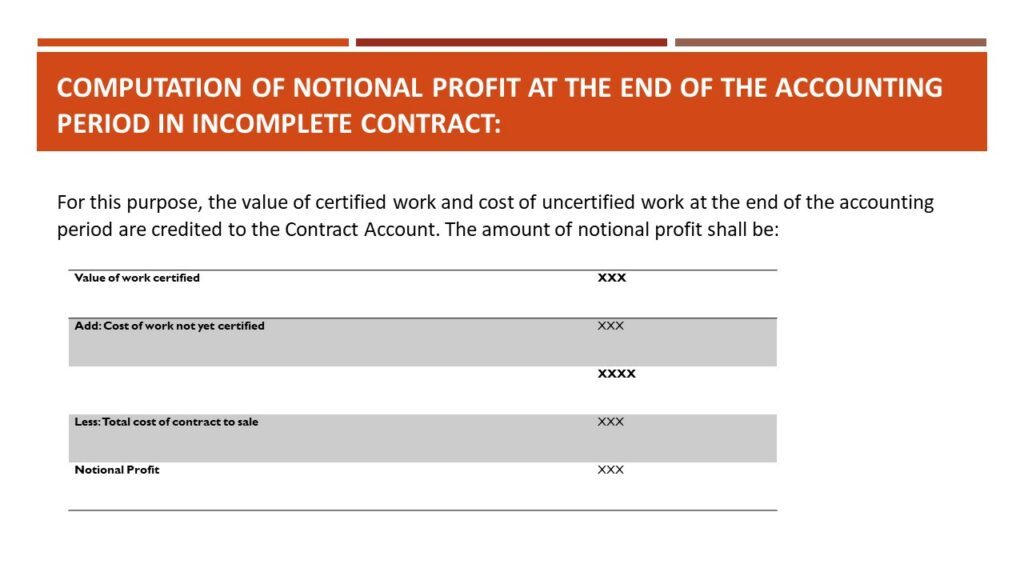

Computation of notional profit at the end of the accounting period in incomplete contract: For this purpose, the value of certified work and cost of uncertified work at the end of the accounting period are credited to the Contract Account. The amount of notional profit shall be:

| Value of work certified | XXX |

| Add: Cost of work not yet certified | XXX |

| XXXX | |

| Less: Total cost of contract to sale | XXX |

| Notional Profit | XXX |

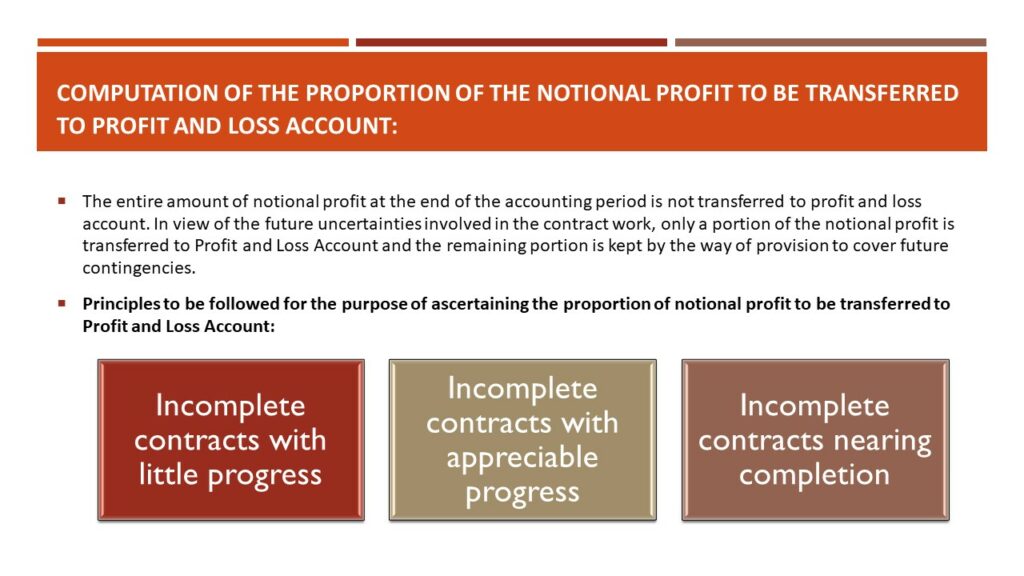

Computation of the proportion of the notional profit to be transferred to profit and loss account:

The entire amount of notional profit at the end of the accounting period is not transferred to profit and loss account. In view of the future uncertainties involved in the contract work, only a portion of the notional profit is transferred to Profit and Loss Account and the remaining portion is kept by the way of provision to cover future contingencies.

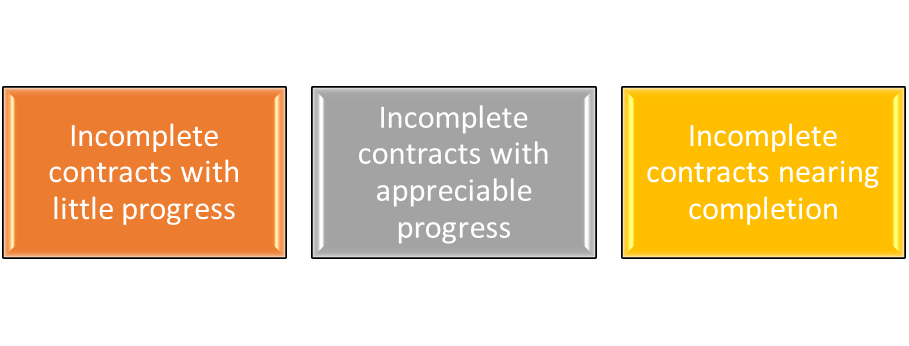

Principles to be followed for the purpose of ascertaining the proportion of notional profit to be transferred to Profit and Loss Account:

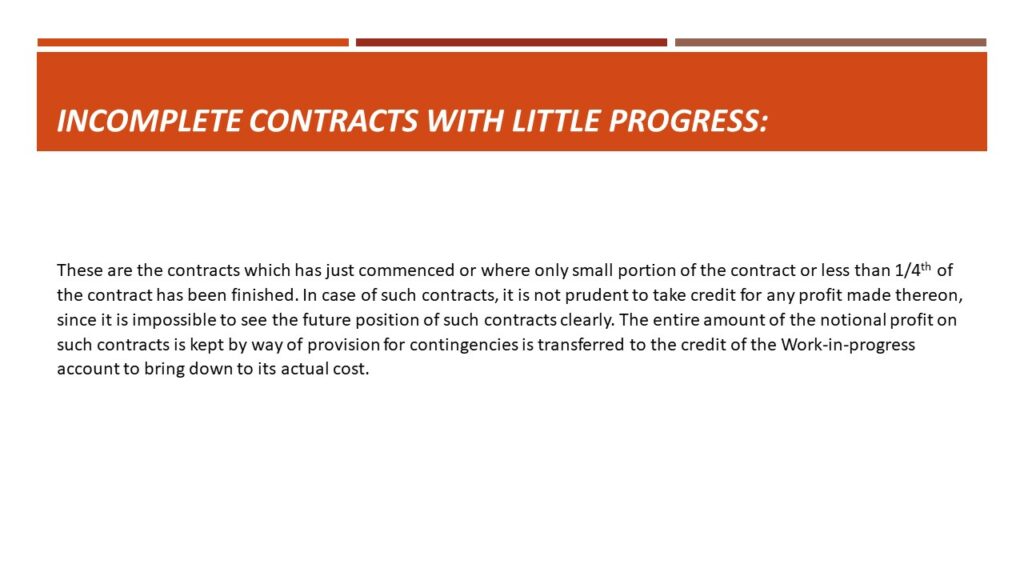

Incomplete contracts with little progress:

These are the contracts which has just commenced or where only small portion of the contract or less than 1/4th of the contract has been finished. In case of such contracts, it is not prudent to take credit for any profit made thereon, since it is impossible to see the future position of such contracts clearly. The entire amount of the notional profit on such contracts is kept by way of provision for contingencies is transferred to the credit of the Work-in-progress account to bring down to its actual cost.

On 1st April 2012 Contractors Ltd. commenced to build a cinema hall, the contract price being ₹6,00,000. During the year ended 31st March, 2013, they incurred the following expenses:

| Materials purchased directly | 50,000 |

| Materials issued form stores | 10,000 |

| Direct wages | 42,000 |

| Plant | 10,000 |

| Overhead charges | 3,000 |

Work to the value of ₹1,20,000 had been certified on 31st March, 2013 of which 75% had been received in cash. Cost of work completed but not certified was ₹10,500. Materials valued at ₹5,000 were on hand at site. After allowing depreciation @20% per annum on plant, prepare contract accounts.

Solution:

CONTRACT ACCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To materials purchased | 50,000 | By materials at site | 5,000 |

| To materials issues from stores | 10,000 | By plant at site | 8.000 |

| To direct wages | 42,000 | By work in progress account: Value of work certified= 1,20,000 Cost of uncertified work= 10,500 | 1,30,500 |

| To plant (cost) | 10,000 | ||

| To overhead charges | 3,000 | ||

| To work-in-progress account (Profit reserved) | 28,500 | ||

| 1,43,500 | 1,43,500 |

WORK-IN-PROGRESS ACCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To contract account: Value of work certified= 1,20,000 Cost of uncertified work= 10,500 | 1,30,500 | By contract account (Profit reserved) | 28,500 |

| By balance c/d | 1,02,000 | ||

| 1,30,500 | 1,30,500 |

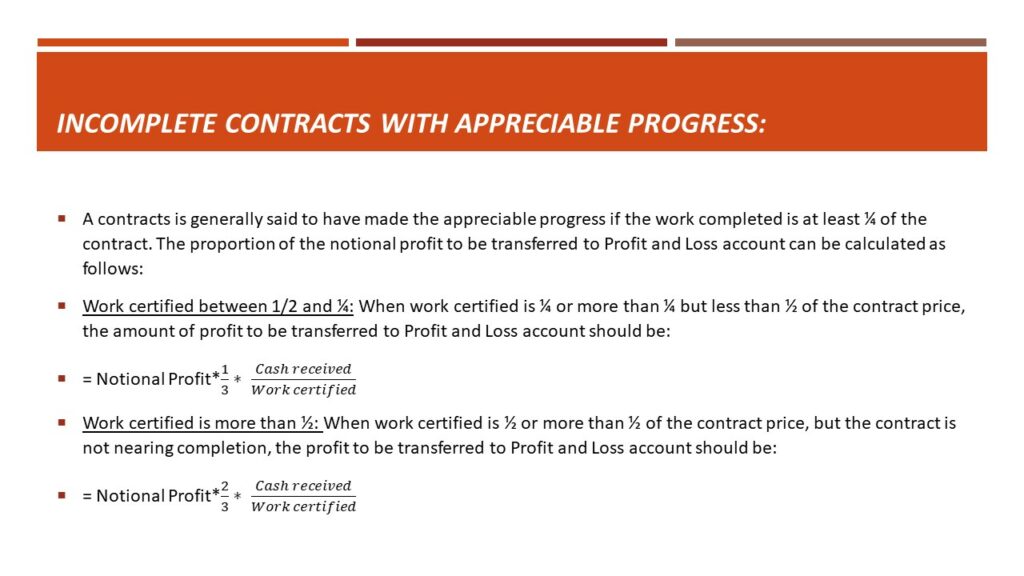

Incomplete contracts with appreciable progress:

A contracts is generally said to have made the appreciable progress if the work completed is at least ¼ of the contract. The proportion of the notional profit to be transferred to Profit and Loss account can be calculated as follows:

Work certified between 1/2 and ¼:When work certified is ¼ or more than ¼ but less than ½ of the contract price, the amount of profit to be transferred to Profit and Loss account should be:

Work certified is more than ½: When work certified is ½ or more than ½ of the contract price, but the contract is not nearing completion, the profit to be transferred to Profit and Loss account should be:

Incomplete contracts nearing completion:

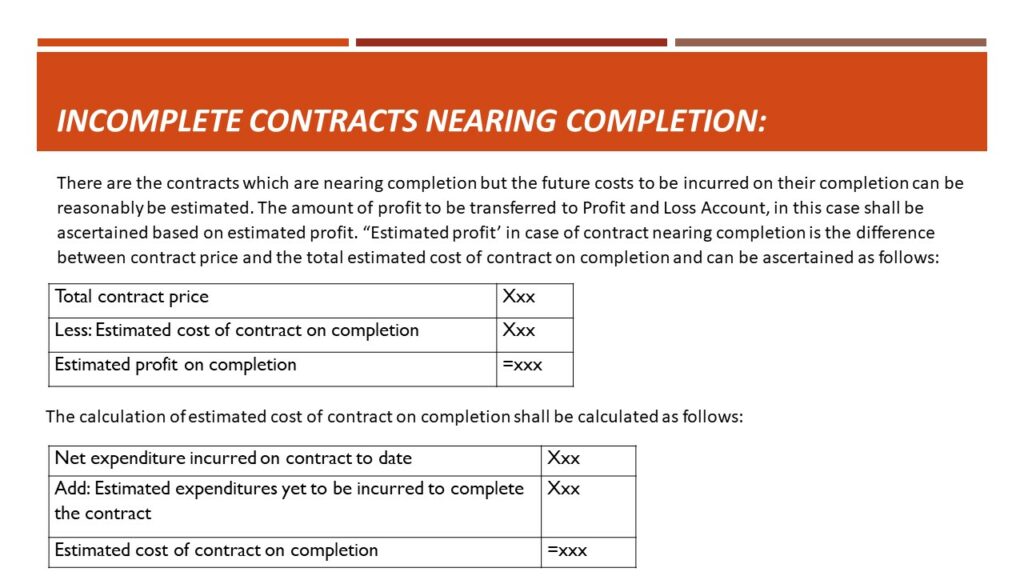

There are the contracts which are nearing completion but the future costs to be incurred on their completion can be reasonably be estimated. The amount of profit to be transferred to Profit and Loss Account, in this case shall be ascertained based on estimated profit. “Estimated profit’ in case of contract nearing completion is the difference between contract price and the total estimated cost of contract on completion and can be ascertained as follows:

| Total contract price | Xxx |

| Less: Estimated cost of contract on completion | Xxx |

| Estimated profit on completion | =xxx |

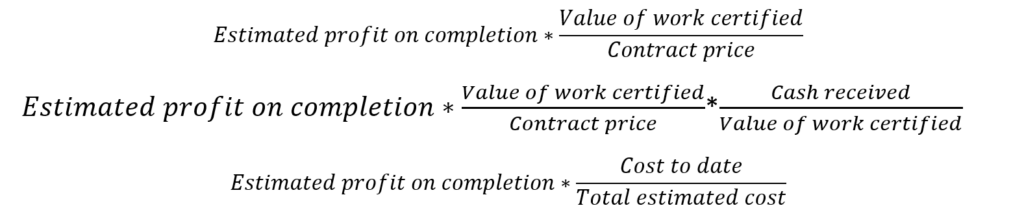

The calculation of estimated cost of contract on completion shall be calculated as follows:

| Net expenditure incurred on contract to date | Xxx |

| Add: Estimated expenditures yet to be incurred to complete the contract | Xxx |

| Estimated cost of contract on completion | =xxx |

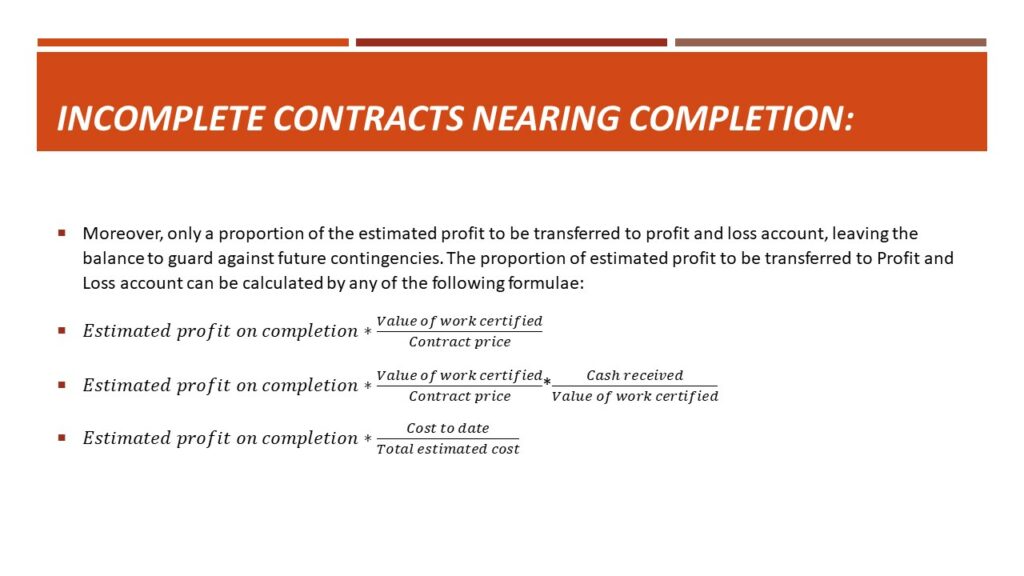

Moreover, only a proportion of the estimated profit to be transferred to profit and loss account, leaving the balance to guard against future contingencies. The proportion of estimated profit to be transferred to Profit and Loss account can be calculated by any of the following formulae: