BREAK EVEN POINT

Break-even point is a point where the total sales or revenue are equal to total costs. In breakeven point, there is no profit or loss in the volume of sales. In other words, it is a point at which no profit no loss situation prevails in the operating activity of a business firm. This indicates that the breakeven point is the minimum level of production at which total cost is recovered and no profit or no loss is sustained.

ACCORDING TO CHARLES T. HORNGREEN

“The break-even point is that point of activity (sales volume) where total revenue and total expenses are equal; it is the point of zero profit and zero loss.”

ACCORDING TO G. R. CROWNING SHEILD

“Break-even point is the point at which sales revenue equals the cost to make and sell the product and no profit or loss is reported.”

The following fundamental formula is used to calculate break-even point:

Break-even Point = Fixed Cost/ PVratio

Break-even Point (in units) = Fixed cost / Contribution per unit

Breakeven Point (Sales Volume)

Breakeven point in sales can be found out by two methods.

1. Selling Price Method

2. PV Ratio Method

1. Selling Price Method: Under this method Break-even sales volume in rupees is found out through the product of Breakeven Point in units and selling price per unit.

BEP (Rs.) = Break-even Point (units)= Selling price per unit

2. PV Ratio Method: Under this method, break-even sales volume in rupees can be determined through the following ratio

BEP (Rs.) = Fixed Cost/ PV ratio

where PV Ratio = Sales- Variable cost /SALES

OR

Contribution / Sales

RELEVANCE OF BREAK EVEN POINT

The breakeven point is useful in the following situations:

- To determine the amount of remaining capacity after the breakeven point is reached, which tells you the maximum amount of profit that can be generated.

- To determine the impact on profit if automation (a fixed cost) replaces labor (a variable cost)

- To determine the change in profits if product prices are altered

- To determine the amount of losses that could be sustained if the business suffers a sales downturn

ANALYSIS OF BREAK EVEN POINT

Management should constantly monitor the breakeven point, particularly in regard to the last item noted, in order to reduce the breakeven point whenever possible. Ways to do this include:

- Cost analysis: Continually review all fixed costs, to see if any can be eliminated. Also review variable costs to see if they can be eliminated, since doing so increases margins and reduces the breakeven point.

- Margin analysis: Pay close attention to product margins, and push sales of the highest-margin items, to reduce the breakeven point.

- Outsourcing: If an activity involves a fixed cost, consider outsourcing it in order to turn it into a per-unit variable cost, which reduces the breakeven point.

- Pricing: Reduce or eliminate the use of coupons or other price reductions, since it increases the breakeven point. Also, increase price points whenever this is acceptable to customers.

To calculate the breakeven point, divide total fixed expenses by the contribution margin. Contribution margin is sales minus all variable expenses, divided by sales. The formula is:

Total fixed expenses/ Contribution margin %

The Break Even Point is shown as follows:

METHODS TO CALCULATE BREAK EVEN POINTS

The sales volume which equates total revenue with related costs and results in neither profit nor loss is

called break-even point (BEP). Break-even point can be determined by the following methods:

1. Algebraic methods:

(i) Contribution Margin Approach

(ii) Equation technique

2. Graphic presentation:

(i) Break-even chart

(ii) Profit volume chart

ALGEBRAIC METHODS

1. Contribution Margin Approach: The break-even point under this approach can be calculated as follows:

Break-even point (in units) = Total fixed costs/ (Selling price per unit -Variable cost per unit)

Or

Total fixed costs/ Contribution per unit

Break even point (In Rupees)= Fixed Cost/ PV Ratio

Or

Beak-even points (units) × Selling price per unit

2. Equation Technique: It is based on an income equation i.e.

Sales – Total costs = Net profit.

Breaking up total costs into fixed and variable,

Sales – Fixed costs – Variable cost = Net profit

Sales = Fixed costs + Variable cost + Net profit

i.e. SP(S) = FC + VC(S) + P

where

SP = Selling price per unit

S = Number of units required to be sold to break-even

FC = Total fixed costs

VC = Variable cost per unit

P = Net profit (Zero)

SP(S) = FC + VC(S) + Zero

SP(S) = FC + VC(S) + 0

SP(S) – VC(S) = FC

or

S(SP – VC) = FC

S= FC/ (SP-VC)

To calculate the level of sales required to earn a particular level of profit, the formula is:

Required Sales (In Rupees)= (Fixed Cost + Desired Profit)/ PV Ratio

GRAPHIC PRESENTATION

1. Break-even chart

ACCORDING TO THE CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS, LONDON

“The break-even chart means a chart which shows profit or loss at various levels of activity, the level at which neither profit nor loss is shown being termed as the break-even point”.

It is a graphic relationship between costs, volume and profits. It shows not only the BEP but also the effects of costs and revenue at varying levels of sales. The break-even chart can therefore, be more appropriately called the cost-volume-profit graph.

Assumptions regarding Break even charts

Assumptions regarding Break-Even Charts are as under:

(i) Costs are bifurcated into variable and fixed components.

(ii) Fixed costs will remain constant and will not change with change in level of output.

(iii) Variable cost per unit will remain constant during the relevant volume range of graph.

(iv) Selling price will remain constant even though there may be competition or change in volume of production.

(v) The number of units produced and sold will be the same so that there is no operating or closing stock.

(vi) There will be no change in operating efficiency.

(vii) In case of multi-product companies, it is assumed that the sales mix remains constant.

A break-even chart can be presented in different forms.

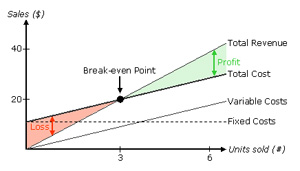

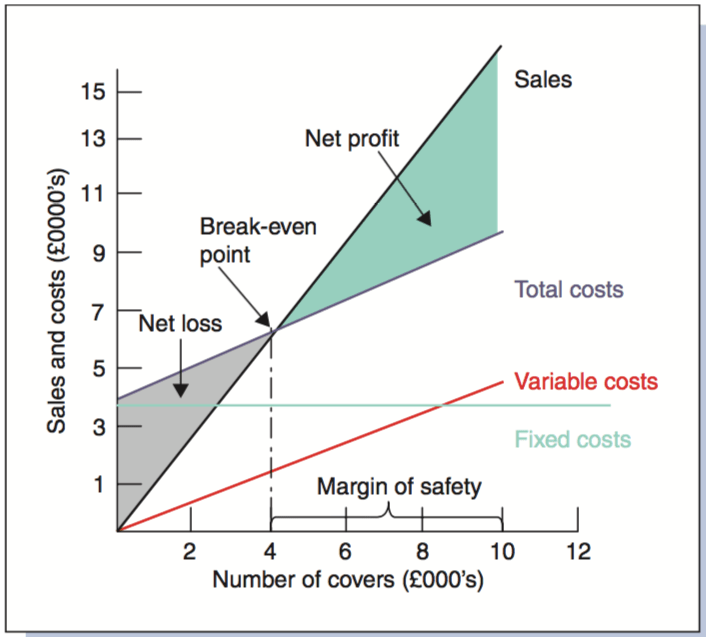

First Method of Break even chart

On the X-axis of the graph is plotted the volume of productions or the quantities of sales and on the Y-axis (vertical line) costs and sales revenues are represented. The fixed costs line is drawn parallel to X-axis. The variable costs for different levels of activity are plotted over the fixed cost line, which shows that the cost is increasing with the increase in the volume of output. The variable cost line is joined to fixed cost line at zero volume of production.

This line is regarded as the total cost line. Sales values at various levels of output are plotted from the origin and joined is called the sales line. The sales line will cut the total cost line at a point where the total costs equal to total revenues and this point of intersection of two lines is known as breakeven point or the point of no profit no loss. The lines produced from the inter-section to Y-axis and X-axis may give sales value and the number of units produced at break-even point respectively.

Loss and profit are as have been shown in the chart which shows that if production is less than the break-even point, the business shall be running at a loss and if the production is more than the breakeven level, there will be profit. The angle which the sales line makes with total cost line while intersecting it at BEP is called angle of incidence. A large angle of incidence denotes a good profit position of a company.

Second Method of Break even chart

This is variation of the first method in which variable cost line is drawn first and thereafter drawing the fixed cost line above the variable cost line. The later line will be the total cost line. The sales line is drawn as usual. The added advantage of this method is that contributions at various levels of output are automatically depicted in the chart.

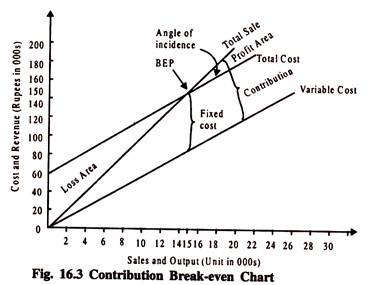

Contribution break-even chart

The chart helps in ascertaining the amount of contribution at different levels of activity besides the break-even point. In this method, the fixed cost line is drawn parallel to the X-axis. The contribution line is then drawn from the origin which goes up with the increase in output. The sales line is plotted as usual, but the question of intersection of sales line with cost line does not arise.

The contribution line crosses the fixed cost line and the point of intersection is treated as break-even point. At this point, contribution is equal to fixed expenses and there is no profit or loss. If the contribution is more than the fixed expenses, profit will arise and if the contribution is less than the fixed expenses, loss will arise.

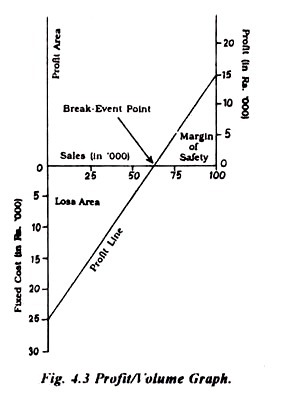

2. Profit-volume Graph

Profit volume graph is the graphical representation of the relationship between profit and volume. Separate lines for costs and revenues are eliminated from the P/V graph as only profit points are plotted. It is based on the same information as is required for the traditional break-even chart and is characterized by the same limitations. The steps in the construction of profit volume graph are as follows:

- Profit and fixed costs are represented on the vertical axis.

- Sales are shown on the horizontal axis.

- The sale line divides the graph into two parts both horizontally and vertically. The area above the horizontal line is the ‘profit area’ and that below it is the ‘loss area’ at which fixed costs are represented on the vertical axis below the sale line and profits on the same axis above the sale line.

- Profits and fixed costs are plotted for corresponding sales volume and the points are joined by a line which is the profit line.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN

https://www.linkedin.com/in/kajal-mahajan-7549b2197/