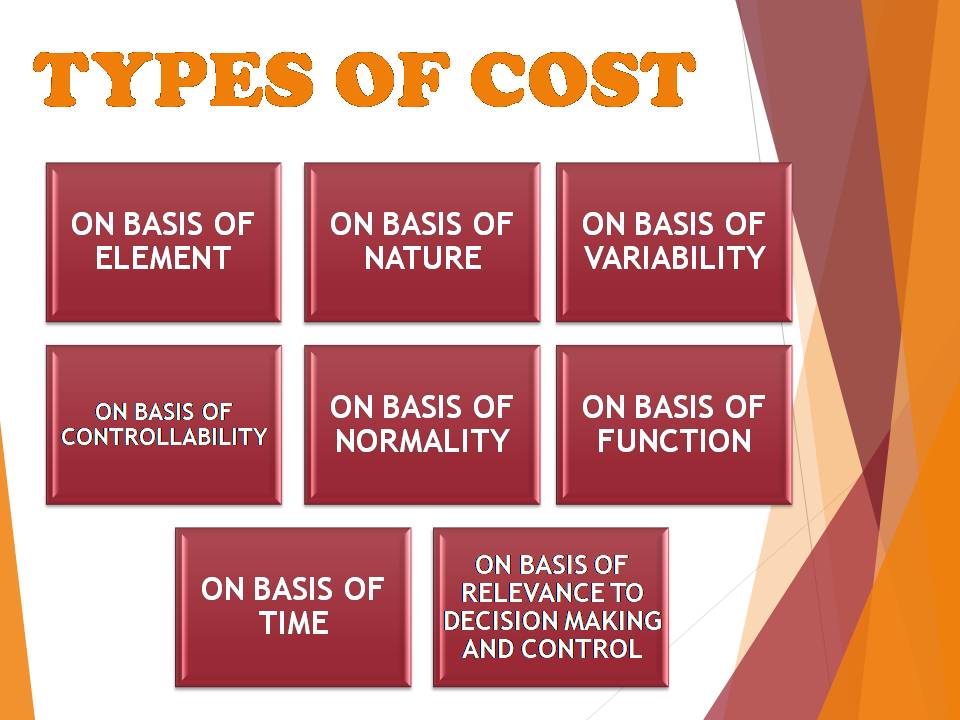

TYPES OF COST

There are various types of cost which can be classified on various bases such as element, nature, variability or behavior, controllability etc.

Cost refers to the expenditure incurred on producing the goods and services. It represents the sacrifice, foregoing or a release of something of value.

ACCORDING TO ICMA (Institute of Cost and Management Accountants), London

‘Cost is the amount of expenditure (actual or notional) incurred on or attributable to a given thing.”

Example: In manufacturing of automobiles, the expenditure incurred on its spare parts, painting and finishing, design, etc constitute the cost of the automobile.

Thus, cost can be said as the measure of resources given up to achieve an objective.

The various types of cost are:

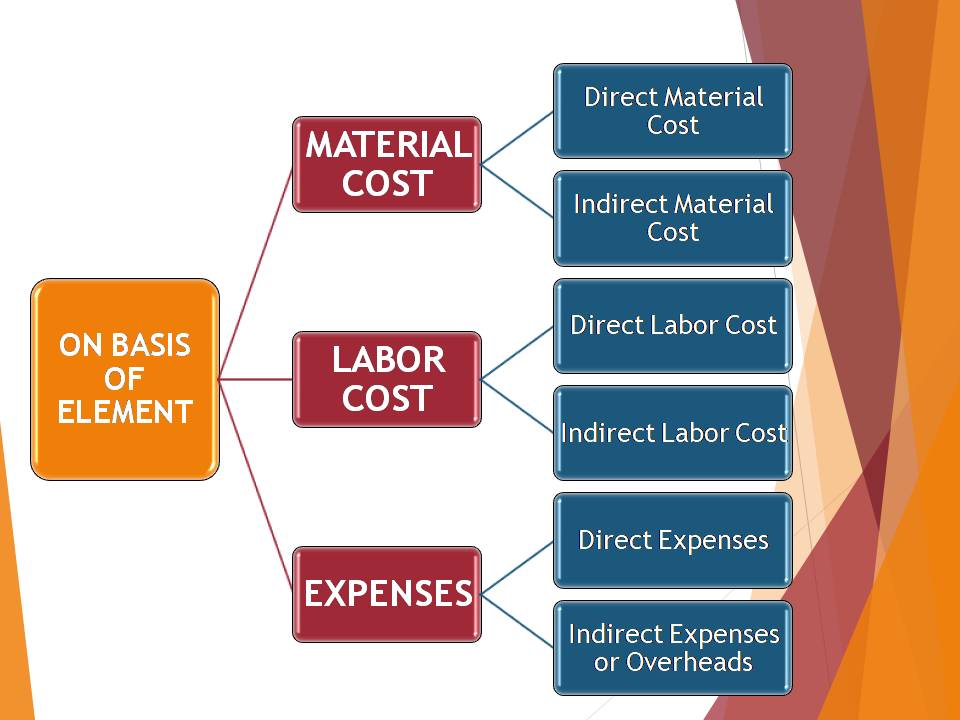

ON THE BASIS OF ELEMENT

On the bases of element, cost can be classified into three categories:

1.MATERIAL COST

It refers to the cost of the material that is supplied to the manufacturing unit for producing the finished product. Example: Cost of thread, nails, shoe polish, leather supplied to an undertaking engages in production of shoes constitute material cost.

Material cost can be classified as follows:

Direct material cost: Direct material cost is the cost of those materials that can be easily identifiable in the finished product. These costs can be attributable to the cost centers or cost units. The cost of such products is directly attributable to the cost of finished product.

Example:

- Cost of leather in shoes.

- Cost of glass in mirror.

- Cost of iron in machinery.

Indirect Material Cost: Indirect Material Cost is the cost which is not directly attributable to the finished product. These costs are not absorbed or apportioned by the cost units or cost centers directly. The cost of such material is not traceable in the finished product. These costs can also be known as non-identifiable or hidden costs.

Example:

- Cost of grease or lubricating oil used in maintenance of machinery.

- Fuel or electricity needed for generating power.

- Materials consumed for repair work.

- Dusters and brooms used for cleansing of factory.

2.LABOR COST

Labor cost refers to the cost of remuneration of the workers employed in an organization. It includes the amount of wages, salaries, perquisites, allowances etc. Labor cost is of two types:

Direct Labor Cost: These are also known as direct wages. This cost can be identified with and allocated to cost centers or cost units.

In case of manufacturing concern, it includes the remuneration paid for converting the raw material into finished products or for altering the construction, composition or condition of the product manufactured by an undertaking.

Example: wages paid for spinning yarn in a spinning mill.

In case of service concern, direct labor cost refers to the wages paid to those who directly carry out or operate the service.

Example: wages paid to the driver and conductor of a bus.

Indirect Labor Cost: These are also known as indirect wages. It refers to that part of labor cost which is not directly attributable to the cost centers or cost units. These are not apportioned to or absorbed by the cost centers or cost units.

Example: Salary paid to the manager, Salary paid to the guard of the office.

3.EXPENSES

Expenses refer to the cost of services provided to an undertaking and the notional costs of the use of the assets owned by the business house.

Example: Deprecation on building, plant and machinery etc.

The expenses are of two types:

Direct expenses: These expenses are also called chargeable expenses. These expenses can be directly identified to the cost centers or cost units.

Example:

- Carriage and freight paid on direct materials purchased.

- Import duty

- Octroi duty etc.

The aggregate of direct material cost, direct labor cost and direct expenses is known as Direct Cost.

Indirect Expenses or Overheads: Expenses which cannot be allocated to the cost centers or units but can be apportioned by them are known as overheads or indirect expenses.

Example:

- Rent, rates and taxes

- Repairs to machinery

- Factory lighting

- Office lighting

- Depreciation and insurance of showroom building etc.

The aggregate of indirect material cost, indirect labor cost and indirect expenses is known as Indirect Cost.

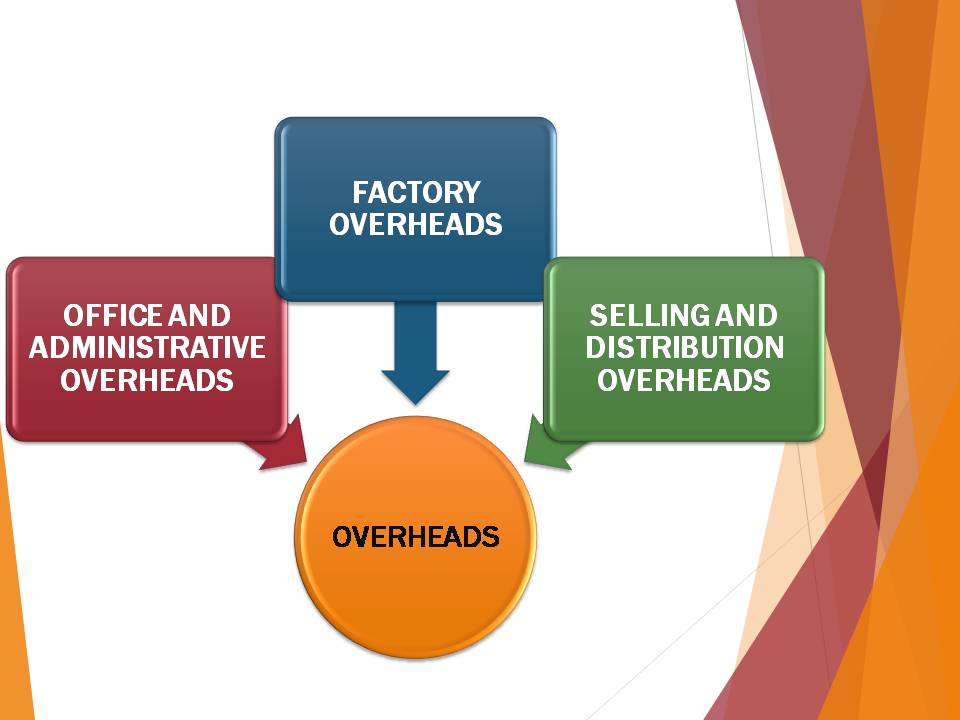

The indirect expenses or overheads can be further sub-divided into:

Factory overheads: It includes all the indirect costs incurred in factory in respect of manufacturing operations. It includes the cost of indirect materials and indirect labor.

Example: Cost of lubricating oil, coal, gas and fuel, wages of store-keeper, salaries of foremen, supervisors, factory rent etc.

Office and Administration Overhead: It refers to the general expenses and expenses of administration and control of business. It includes all the indirect costs relating to direction, guidance, management, control and administration of business concern.

Example: Salary of general manager, insurance expenses, office rents, office rates, office lighting etc.

Selling and Distribution overheads: These include all the indirect costs which are incurred for

- Promoting the sales

- Retaining the customers

- Providing after sale services to the consumers

- Raising the market share of the concern.

Example: Advertisement, salary of sales manager etc.

These costs play an important role in growing the business and its goodwill.

ON THE BASIS OF NATURE

On the basis of nature, the costs are classified according to their identifiability with the cost units or cost centers. The types of cost on the basis of nature are as follows:

1.DIRECT COSTS

These are the costs that are directly identifiable and traced with the cost units or cost centers. Direct material cost, direct expenses and direct labor cost are the constituents of the direct cost.

Example: Cost of iron in machinery, cost of leather in shoe etc.

2.INDIRECT COSTS

These are the costs that are not directly identifiable with the cost units or cost centers. The indirect materials cost, indirect expenses and indirect labor costs are the constituents of indirect cost.

Example: Salary of workmen, salary of guard, fuel and power cost etc.

ON THE BASIS OF VARIABILITY OR BEHAVIOR

The costs can be divided into three parts on the basis of change in the volume of activity. The types of cost are:

1.FIXED COST

A fixed cost is a cost which is incurred for a particular period of time and which, within certain activity levels, is unaffected by changes in the level of activity. These costs mainly depends upon the effluxion of time and do not vary directly with the changes in the volume or output or sales. Example: rent of the building, insurance of the building etc.

2.VARIABLE COST

A variable cost is a cost which tends to vary with the level of activity. These costs tend to increase or decrease with the rise and fall in the production or sales. These costs vary in total but per unit cost remains the same. Example: cost of raw material used in producing finished product.

3.SEMI VARIABLE COST

This is the cost that contains both a fixed cost and a variable cost component. The part of semi-variable costs remains constant inspite of changes in the volume of output or sales, while the other part varies in proportion to changes in volume of output or sales. Example: Repairs and maintenance cost of plant, salary of supervisor etc.

ON THE BASIS OF CONTROLLABILITY

As per this, the types of cost are:

1.CONTROLLABLE COST

Each department in the concern is placed under the direct control of some supervisor. The costs associated with such departments are directly under the control of the supervisor, hence known as controllable costs.

2.UNCONTROLLABLE COST

These refer to those costs which cannot be influenced by the action of a specified member of an undertaking.

ON THE BASIS OF NORMALITY

As per this basis, the costs can be classified which are normally occurred at a given level of output in conditions in which that level of output is normally attained. These costs can be:

1.NORMAL OR UNAVOIDABLE COSTS

These are those costs which are normally attained at a given level of output in the conditions in which that level of output is normally attained. These costs cannot be avoided at all. Example: Cost of normal spoilage of materials.

2.ABNORMAL OR AVOIDABLE COSTS

These are those costs which are not normally incurred at a given level of output in the conditions in which that level of output is attained. These costs can be avoided if proper care can be taken. Example: Cost of the material lost by theft.

ON THE BASIS OF FUNCTION

The types of cost on the basis of function are:

1.PRODUCTION COSTS

The costs incurred on the production activity i.e. from acquiring the raw material and conversion into finished products. Example: Cost of packaging, Cost of labor etc.

2.ADMINISTRATION COSTS

The costs which are incurred for formulating the business policies for directing the organization and controlling the operations of an undertaking. These cots should not be related to the research and development purposes etc.

3.SELLING COSTS

The costs incurred on selling the products are selling costs. Example: Cost on advertisement.

4.DISTRIBUTION COSTS

The costs incurred on making the products available in the market are known as distribution costs. These costs are incurred on dispatching the products.

ON THE BASIS OF TIME

From the point of view of time, the types of cost are:

1.HISTORICAL COSTS

These are the costs that are ascertained after they have been incurred. These are determined after the goods have been manufactured or services have been rendered.

2.PRE-DETERMINED COSTS

These are the costs which can be computed in advance of production. These costs can be estimated costs or standard costs.

ON BASIS OF RELEVANCE TO DECISION MAKING AND CONTROL

On this basis, the types of cost are:

1.MARGINAL COST

This is the amount at any given volume of output by which aggregate costs are changed if the volume of output is increased or decreased by one unit.

2.SUNK COST

These refer to the costs which have already been incurred and cannot be altered by any decision in the future. These costs become irrelevant for later decisions.

3.OPPORTUNITY COSTS

These are the cost of the best alternative foregone. It is measured in terms of revenue which could have been earned by employing the resources in some other alternatives uses.

4.IMPUTED COSTS

These are those costs which are not included in the costs but are considered for making management decisions. These costs are hypothetical in nature. Example: Interest on capital, though not actually payable, is often required to be included in order to judge the relative profitability of two products involving unequal outlays of cash.