MEANING

Perpetual Inventory System refers to a system of maintaining such records as will reflect the receipts, issues and balance of all items of materials in store all the times. It is a material control technique.

ACCORDING TO ICMA (Institute of Cost and Management Accountants), UK

“Perpetual Inventory System is a system of records maintained by the controlling department, which reflects the physical movement of stock and their current balance.”

Under this system, an entity continually updates its inventory records to account for additions to and subtractions from inventory for such activities as:

- Received inventory items

- Goods sold from stock

- Items moved from one location to another

- Items picked from inventory for use in the production process

- Items scrapped

The widespread use of computers after 1970’s has increased this system popularity because businesses were able to more easily keep track of inventory as it sold. The barcodes, radiofrequency identification scanners and point of sale systems provided support for this system by quickly inputting inventory information as customers purchase items.

The formula for perpetual inventory system is as follows:

Beginning Inventory+ Reciepts- Shipments= Ending/ Closing Inventory

FEATURES OF PERPETUAL INVENTORY SYSTEM

The following are the features of perpetual inventory system:

- This system traces every single movement of inventory.

- It is prepared on the basis of book records.

- The records maintained in this are updated continuously.

- It tells the information about inventory and cost of sales.

- It assists in inventory control.

- This system has no impact on the business operation.

RECORDS KEPT UNDER PERPETUAL INVENTORY SYSTEM

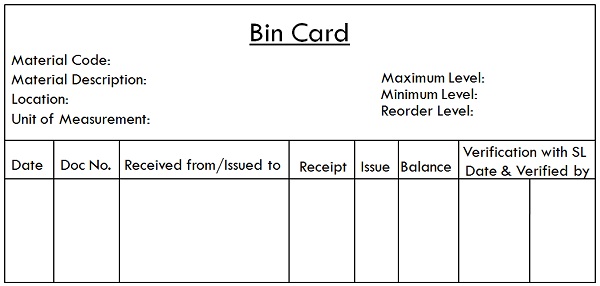

1.BIN CARD

It is maintained in the stores department and shows the quantities of materials received, issued and balance in hand after each receipt and issue. It is also known as stock card or bin tag. It is featured as follows:

- It is the statement if all the receipts and issues of material from stock from the stores department.

- It is maintained by the store-in-charge or store keeper.

- It is kept inside the store department.

- It records only quantity of materials not the value.

- It is updated when receipts and issues are made in the store department.

- Transactions are updated individually because at every point of time, store keeper needs to be aware of the actual position of the stock.

The format of Bin Card is as follows:

The following are the advantages of the Bin Card:

- Bin Card is maintained for each item in the stock, in this way it facilitates individual record keeping.

- It also provides information about the minimum level or maximum level of stock.

- Bin Card is flexible to use as its format is not standard or rigidly specified.

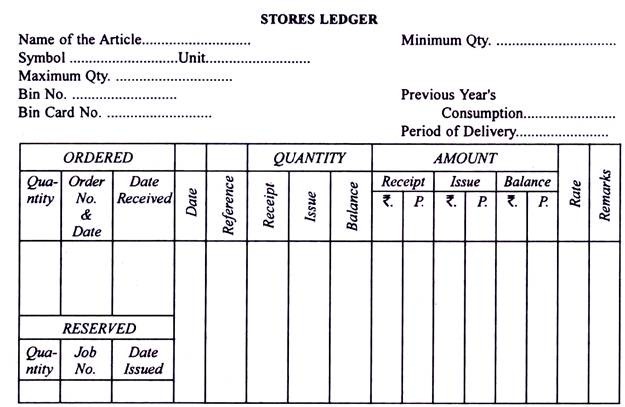

2.STORES LEDGER

It is maintained by costing office and deals with the quantities and values of materials received, issued and balance in hand. It is an assemblage of cards or sheets, which are maintained to keep a record of quantity and cost of material received, transferred and remained in stock. It comprises if an account for each item in the stock room and keeps the record of:

- Quantity

- Type

- Rate

- Amount

It is featured as follows:

- It is subsidiary ledger to the cost ledger.

- It is an accounting record.

- It is maintained by cost accounting department.

- It is kept outside the stock room.

- It contains both quantitative and monetary details.

- It records inter-departmental transfer.

- The summary of transactions is recorded in this.

The format of stores ledger is as follows:

The advantages of stores ledger is as follows:

- It works greatly as internal control system.

- It may be made in manual or in computerized form.

- It tells the quantity as well as value of the materials.

However, stores ledger suffers from some drawbacks which are as follows:

- It contains the summary of the records not details.

- The transactions are not updated individually.

ADVANTAGES OF PERPETUAL INVENTORY SYSTEM

The following are the advantages of perpetual inventory system:

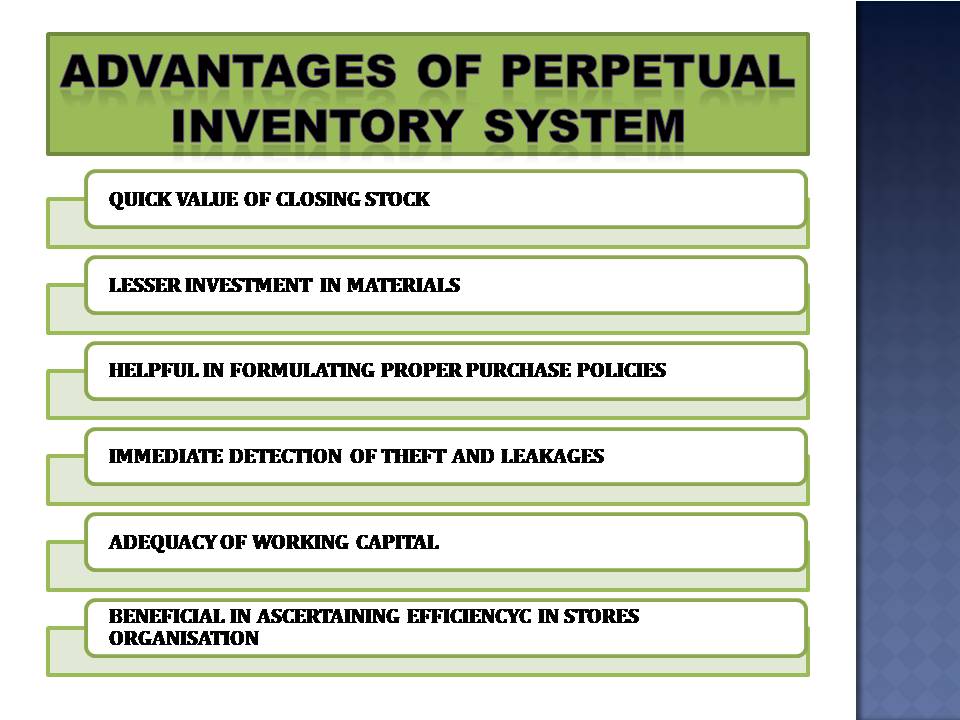

QUICK VALUE OF CLOSING STOCK: On account of continuous stock taking, the value of closing stock can be known at any time during the year. It greatly facilitates the preparation of profit and loss account and balance sheet at the end of the financial period.

LESSER INVESTMENT IN MATERIALS: By introducing the perpetual inventory system, a regular check on receipt and issue of materials and stores is undertaken. This considerably reduces the investment in materials and storage expenses are also minimized.

HELPFUL IN FORMULATING PROPER PURCHASE POLICIES: A storekeeper can easily know the time when quantity of materials will be required by each department of the factory. All this information is very useful in formulating proper purchase policies.

IMMEDIATE DETECTION OF THEFT AND LEAKAGES: with the help of a properly planned system of perpetual inventory control, wastages, leakages and thefts of materials are at once brought to light and causes for such discrepancies can be known without delay.

ADEQUACY OF WORKING CAPITAL: The system ensures an effective control over the storing, issuing and using of materials. This leads to avoidance of unnecessary locking up of capital in the stock. This makes available adequate supply of working capital which can be applied in other profitable spheres of the concern.

BENEFICIAL IN ASCERTAINING EFFICIENCY IN STORES ORGANISATION: Perpetual inventory control system acts as an important instrument to ascertain efficiency and working of stores in a production undertaking as it ensures continuous check on the working and operations of the stores.

OTHER ADVANTAGES: The other advantages of perpetual inventory system are:

- It ensures timely replenishment of stock.

- The records maintained are up-to-date.

- The fixing percentage of normal loss can be ensured by putting strict control over wastages and losses.

- Business operations need not to be closed on account of yearly stock taking.

DISADVANTAGES/ LIMITATIONS OF PERPETUAL INVENTORY SYSTEM

Despite so many advantages, this system also suffers from serious limitations, which are as follows:

HIGHER COST INVESTMENT: One disadvantage of perpetual inventory system involves the setup cost. Most systems require the purchase of new equipment and inventory software. This equipment includes point of sale scanners which read the bar code of each item. Scanners are also required when items are received into inventory. Perpetual inventory systems also add to labor costs since all the inventory must be entered into the system.

TRAINING ON EQUIPMENT: Another disadvantage to implementing a perpetual inventory system involves the increased level of training required. Employees need to know how to operate the various scanning equipment. Accounting personnel need training to navigate the inventory system.

FALSE RELIABILITY: Perpetual inventory systems can be misleading when reviewing inventory levels. Employees can make mistakes entering quantities or scanning the wrong inventory item. Shoplifters may steal merchandise.

INCREASED MONITORING: The need for increased monitoring because of employee errors or customer theft requires and additional financial investment. Security monitors typically need to be installed and some companies hire security personnel.