OBJECTIVES AND ADVANTAGES OF COST ACCOUNTING

COST ACCOUNTING

Cost Accounting is an art or process of recording, analysing and classifying of expenditure for the purpose of product costing or service costing, ascertainment of profitability, operational planning and cost control.

It is a forward-looking approach which is related to the recording, analysing and classifying of expenditure with the objective of ascertaining the total and per unit cost of product or service.

ACCORDING TO ICMA (Institute of Cost and Management Accountants)

“Cost accounting is the process of accounting for cost from the point at which expenditure is incurred or committed to the establishment of its ultimate relationship with cost centers and cost units. In its widest usage, it embraces the preparation of statistical data, the application of cost control methods and ascertainment of the profitability of activities carried out or planned.”

ACCORDING TO RN CARTER

“It is a system of recording in accounts the materials used and labor employed in the manufacture of certain commodity or on a particular job.”

OBJECTIVES OF COST ACCOUNTING

Cost accounting is a branch of accounting that deals with the identification, measurement, and analysis of the costs associated with a business operation. The main objective of cost accounting is to provide accurate and reliable information to management that can be used for decision-making. The following are the detailed objectives of cost accounting:

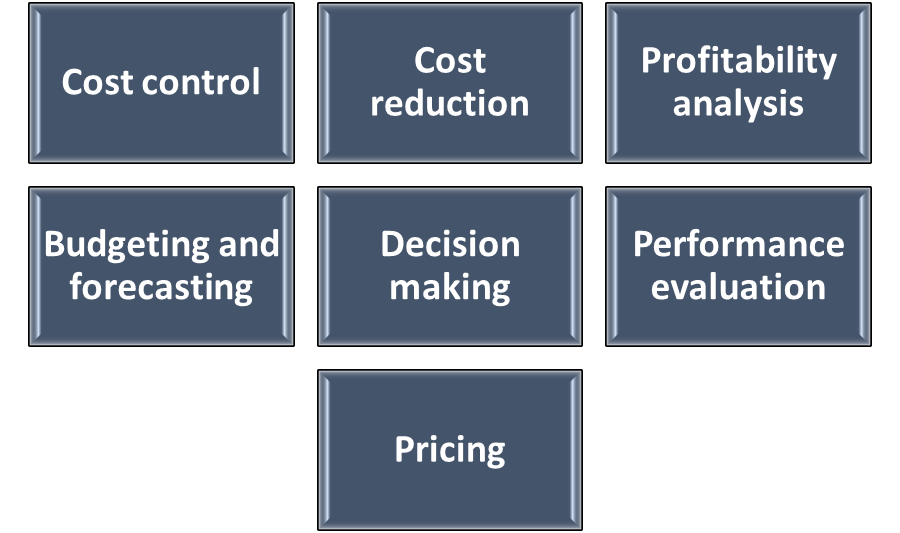

Cost Control: One of the primary objectives of cost accounting is cost control. Cost control is the process of identifying the various cost elements and controlling them through various techniques. Cost accounting helps in controlling the costs of production, identifying the cost of each process and identifying the inefficiencies in each process. This objective helps the management to understand the cost elements and take corrective actions to reduce them.

Cost Reduction: Cost reduction is another important objective of cost accounting. Cost accounting helps in reducing costs by identifying wastages, reducing idle time, and improving efficiency in the production process. Cost reduction is important for the survival of the business, especially in the current competitive business environment.

Profitability Analysis: Cost accounting helps in analyzing the profitability of the business. This objective involves identifying the sources of profit and loss in the business. Cost accounting helps the management to understand the profit margins and take necessary actions to increase profitability. Profitability analysis helps the management to understand the profitability of each product or service and take necessary actions to improve profitability.

Budgeting and Forecasting: Cost accounting provides the necessary data for budgeting and forecasting. Budgeting involves planning the future business operations and allocating resources to achieve the goals of the business. Forecasting involves estimating future trends in the market and the impact of those trends on the business. Cost accounting provides the necessary data for budgeting and forecasting, which helps in planning for future business operations.

Decision Making: Cost accounting provides accurate and reliable information that management can use to make informed decisions. Decision making involves analyzing the costs and benefits of different alternatives and choosing the best alternative. Cost accounting helps the management to make informed decisions by providing accurate data on the costs of different alternatives.

Performance Evaluation: Cost accounting helps in evaluating the performance of different departments, processes, and products. This objective involves comparing the actual costs with the budgeted costs and identifying the variances. Performance evaluation helps the management to understand the efficiency of each process and take necessary actions to improve efficiency.

Pricing: Cost accounting provides information on the cost of production, which is used in setting prices for products and services. Pricing involves setting the price of the product or service that covers the cost of production and provides a reasonable profit margin. Cost accounting helps the management to understand the cost of production and set the prices accordingly.

In conclusion, cost accounting plays a vital role in the success of a business. The objectives of cost accounting include cost control, cost reduction, profitability analysis, budgeting and forecasting, decision making, performance evaluation, and pricing. These objectives help the management to understand the cost elements, identify inefficiencies in the production process, and take necessary actions to improve the efficiency of the business.

ADVANTAGES OF COST ACCOUNTING

Cost Accounting system renders invaluable services to the manufacturers, management, employees, investors, consumers and government. The various advantages of cost accounting are as follows:

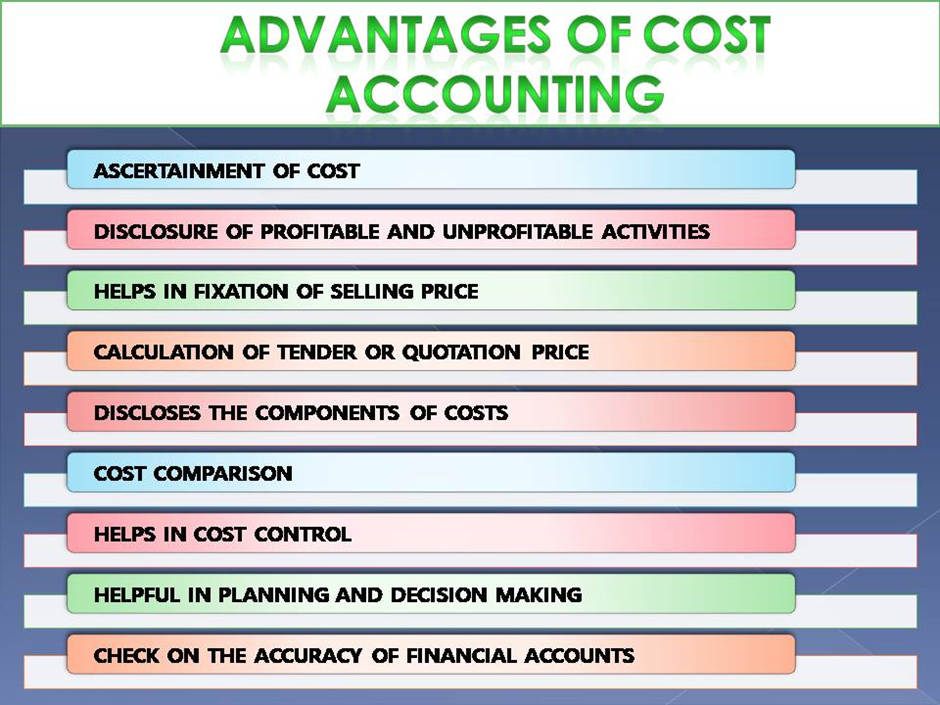

ASCERTAINMENT OF COST

The sphere of cost accounting comprises cost ascertainment firstly. Cost ascertainment means determining the cost incurred in producing any product. The cost ascertainment includes:

- Collection of expenses

- Analysis of expenses

- Measurement of production

The cost may be ascertained by following ways:

Activity Based Costing in which each activity is taken as fundamental cost object.

Unit costing which is adopted to ascertain the total cost and also per unit cost by making a detailed analysis of different elements of cost.

Job Costing method as per which costs is ascertained for the particular job or work.

Batch Costing which is used when products are produced in batches and cost is ascertained for each batch separately.

Contract Costing is a method of cost ascertainment of a particular contract which is non-recurring in nature. The person executing the contract is known as ‘contractor’ and the person with whom the contract is executed is known as the ‘Contractee’.

Process Costing is a method employed to ascertain the cost of production in industries where a product passes through different processes or stages.

Operation Costing represents the costing in which each cost of each operation involved in an activity is ascertained separately.

Composite Costing is applied to ascertain the cost of complex products manufactured by the manufacturing concerns where no single method of ascertaining cost can be applied.

Departmental Costing is adopted where the factory is divided into several departments and it is desired to ascertain the cost of each department than the whole concern collectively.

DISCLOSURE OF PROFITABLE AND UNPROFITABLE ACTIVITIES

The accounting records prepared on the basis of cost accountancy discloses the cost incurred of each job, process or operation. It provides the data to make a decision regarding the profitable and unprofitable activities of the concern. This information provides a base to make a decision regarding which activity is to be contracted or eliminated and which activity is to be expanded.

HELPS IN FIXATION OF SELLING PRICE

Cost accounting provides all the details regarding the actual cost incurred in the production of the commodity. It provides the businessman with the sound basis for fixing the selling price of the commodity. This protects the businessman from taking the wrong decision of charging fewer prices and incurring losses.

CALCULATION OF TENDER OR QUOTATION PRICE

Tenders or quotations are made to provide the rate which will be charged to supply the manufactured goods in future times. The cost data provides a useful base to set the tender price. If the tenders are based on the actual cost data, they are bound to be competitive and sure to be accepted by the prospective customer.

DISCLOSES THE COMPONENTS OF COSTS

To manufacture a product, the cost is incurred on material, labor and overheads. Cost accounting records

- Wage rate payable to efficient or inefficient employees

- Material ordering costs

- Material carrying costs

- Overtime cost, etc

All this minute information assist the manufacturer to ascertain the importance of each element of cost and determining where there is greater scope for the economy.

COST COMPARISON

The accounting records of cost of one year can be compared with the records of another year. The cost accounting system provides the reliable information to compare the costs of different periods, for different volumes of output, in different departments or processes and in different establishments.

HELPS IN COST CONTROL

Cost control is the guidance and regulation of the costs by the administration and management authorities. It guides the organization to achieve the target of the undertaking for a given period. Cost control involves the following steps:

- Setting up the targets for expenses and production performance

- Measurement of the actual performance

- Comparison of the actual performance with the standard performance

- Finding out deviations, if any

- Taking corrective actions to remove all the deviations.

Cost control is done by following the various techniques:

Marginal Costing: It is a technique of cost accounting which pays attention to the behavior of costs with changes in the volume of the output.

Budgetary Control: It involves the establishment of budgets relating to the responsibilities of the executives to the requirements of the policy and the continuous comparison of the actual with the budgeted results, either to secure by individual action of that policy or to provide a basis for its revision.

Standard Costing: Standard costing discloses the cost of deviations from standards and classifies these as to their causes, so that management is immediately informed of the sphere of operations in which remedial action is necessary.

Variance Analysis: Variance analysis is a process of analyzing variances by sub-dividing the total variance in such a way that the management can assign the responsibility for off production performance. The main cost variances are: direct material variance, direct labor cost variance and overhead variance.

HELPFUL IN PLANNING AND DECISION MAKING

The various cost records maintained under the cost accounting system provide valuable information for the purpose of future planning and for decision making. The costing records assist the management in making the following decisions:

- Manufacture or buy decision.

- Selection of the profitable product mix

- Operate or shut down decisions

- Selection of profitable method of production

- Fixation of the selling price.

CHECK ON THE ACCURACY OF FINANCIAL ACCOUNTS

Cost Accounting system provides an independent and most reliable check on the accuracy of financial accounts by means of reconciliation of profits as shown by cost accounts and financial accounts.