COST SHEET VS PRODUCTION ACCOUNT

Cost statement may be presented in the form of ledger account termed as “production account”. Production account presents information of production cost in an analytical manner according to double entry system. Cost of production and profit can be computed in this ledger.

Cost Sheet Vs Production Account is as follows:

| BASIS OF DIFFERENCE | COST SHEET | PRODUCTION ACCOUNT |

| FORM | It is prepared in the form of a statement. | It is prepared like an account |

| DOUBLE ENTRY | It is not based on double entry system. | It is based on double entry system and there are debit and credit side. |

| PERIOD | It is prepared with a view ascertain total-cost as well as per unit cost of production. | It is prepared after completion of production. |

| COMPARATIVE STUDY | Comparative study for two periods or two type of production is feasible. | Such comparative study is not possible in these methods. |

| COMPARISON WITH FINANCIAL ACCOUNTS | Results cannot be compared with financial account’s results. | Results can be compared with financial account’s results. |

| COST ANALYSIS | Detailed analysis of cost is made to control different elements of cost, viz. material, labor and expenses. | Different items of cost are shown as totals and are not analyzed. |

COST SHEET

Cost sheet is a device used to determine and present the cost under unit costing. It is a statement of costs incurred at each level of manufacturing a product or service. In a Cost sheet all the elements of cost is taken into consideration. It includes Prime cost, Factory/manufacturing cost, cost of production, cost of sale, Profit/loss etc.

ACCORDING TO C.I.M.A, LONDON

“Cost sheet is a cost schedule or document which provides for the assembly of the estimated detailed cost in respect of a cost center or cost unit”.

ACCORDING TO WHELDON

“Cost sheets are prepared for the use of management and consequently, they must include all the essential details which will assist the manager in checking the efficiency of production”

Items excluded from Cost Sheet:

1. Pure financial expenses like interest on capital, interest on loan, discount on debentures, loss on sale of fixed asset provision for bad debts and doubtful debts, writing off goodwill, copyright, preliminary expenses etc.

2. Pure financial incomes like interest received, profit on sale of investment, dividend received, rent received, commission received, discount received etc.

In addition to the above, no appropriation items will include in cost sheet.

Form of a Cost Sheet: Cost sheet for the period ending

| PARTICULARS | AMOUNT |

| Direct material Direct wages Direct Expenses | |

| Prime Cost | |

| Add: Factory Overheads | |

| Factory Cost | |

| Add: Administration Overheads | |

| Cost of Production | |

| Add: Selling and Distribution Overheads | |

| Total Cost /Cost of sale |

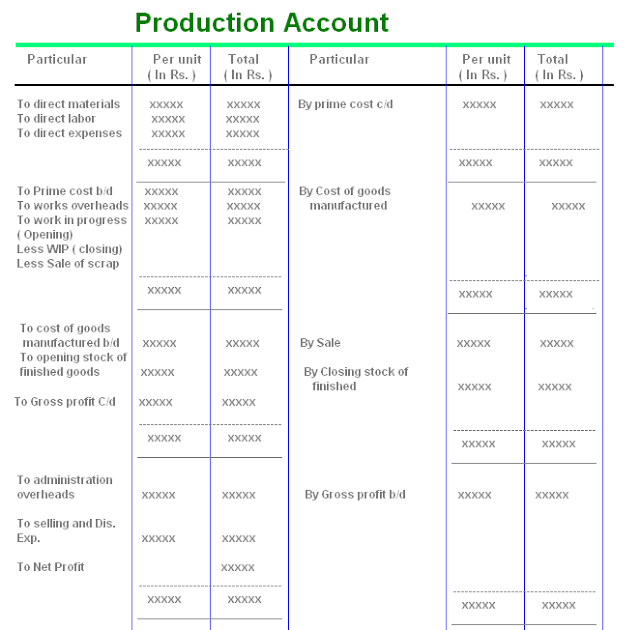

PRODUCTION ACCOUNT

If the details of cost sheet or production statement are shown in the form of a ledger account, it is known as production account. Besides cost of production it also includes selling and distribution expenses. It is prepared in three parts – the first part gives the cost of production, the second part gives the cost of goods sold and the third part shows cost of sales or total cost for the period. A specimen of a Production Account is as follows: