IDLE TIME

Idle time means the amount of time the workers remain idle in a normal working day. It is that time for which the employer pays, but from which he obtains no production. In other words, idle time is the difference between the time shown by the time card and job card. The idle time is usually caused by a sudden fault in machine or equipment, power failure, lack of orders for the product, inefficient work scheduling, defective materials and shortage of raw materials etc. The accounting treatment of idle time is that it is treated as indirect labor cost and should, therefore, be included in manufacturing overhead cost.

Idle Time = Total Time spent by a worker – Actual Time spent on production.

EXAMPLE: The normal weekly working hours of a worker are 48 and he is paid @ $8 per hour. If he remains idle for 6 hours due to power failure, then the cost of 42 hours would be treated as direct labor cost and the cost of 6 hours (idle time) would be treated as indirect labor cost and included in manufacturing overhead cost.

- Idle time is paid time that an employee, or machine, is unproductive that is a result of factors that can either be controlled or uncontrolled by management.

- Idle time can be classified either as normal or abnormal.

- Minimizing idle time is key if a business wants to maximize efficiency over long periods of time.

TYPES OF IDLE TIME

NORMAL IDLE TIME

Normal Idle time is inherent in any work situation and cannot be eliminated. This represents the time, the wastage of which cannot be avoided and, therefore, the employer must bear the labour cost of this time. But every effort should be made to reduce it to the lowest possible level. Following are some of the examples of normal idle time:

(i) The time taken in going from the factory gate to the department in which the worker is to work, and then again the time taken in coming from the department to the factory gate at the end of the day.

(ii) The time taken in picking up the work for the day.

(iii) The time which elapses between the completion of one job and the commencement of the next job.

(iv) The time taken for personal needs and tea breaks.

(v) The time lost when production is interrupted for machine maintenance.

(vi) The time lost due to waiting for job, instructions, drawings, the prints, material etc. or due to machine set-up time which are normal to production.

ABNORMAL IDLE TIME

It is that time the wastage of which can be avoided if proper precautions are taken. Abnormal idle time is such idle time that given the situation is considered controllable and should have been avoided if due care was taken. In other words abnormal idle is most of the time result of mismanagement.

Examples of abnormal idle time can be cited as below:

(i) The time wasted due to breakdown of machinery on account of the inefficiency of the works engineer.

(ii) The time wasted on account of the failure of the power supply.

(iii)The time wasted due to shortage of materials on account of the inefficiency of the storekeeper or the purchasing department.

(iv) The time wasted due to unnecessary waiting for instructions.

(v) The time wasted due to unnecessary waiting for tools and raw materials, and

(vi) The time wasted due to strikes or lock-outs in the factory.

CAUSES OF IDLE TIME

There are various causes of normal idle time and abnormal idle time. So the causes are classified into two categories on the basis of types of idle time.

CAUSES OF NORMAL IDLE TIME

(1) Travelling time from one job or department to another.

(2) The distance covered between the factory gate and actual place of work.

(3) Elapse of time between finishing one job and starting another job.

(4) Time spent to overcome fatigue.

(5) Tea and lunch breaks.

(6) Machine or job setting-up time etc.

CAUSES OF ABNORMAL IDLE TIME

(a) Temporary lack of work,

(b) Machine breakdown,

(c) Power failures,

(d) Shortage of raw materials,

(e) Waiting for tools,

(f) Waiting for jobs due to unplanned production,

(g) Stoppage of work due to managerial policy decisions,

(h) Strikes and lockouts, and

(i) Floods, earthquakes, etc.

ACCOUNTING TREATMENT OF IDLE TIME

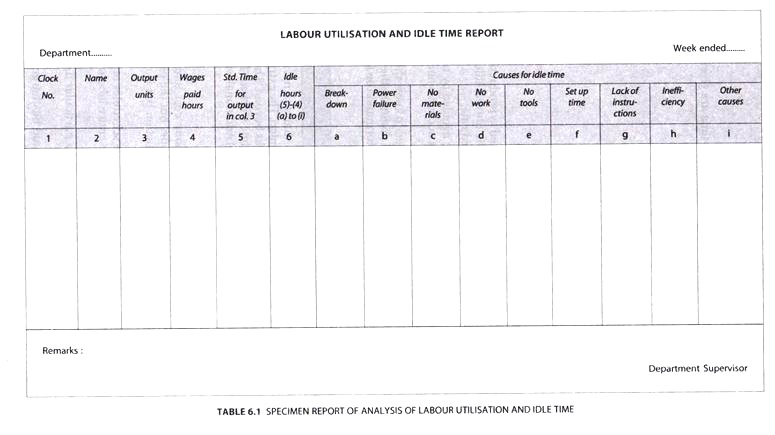

Accounting treatment of idle time depends upon the categorization of idle time. The following specimen shows the treatment in the costing records:

The normal idle time and abnormal idle time treatments is as follows:

ACCOUNTING TREATMENT OF NORMAL IDLE TIME

There are two methods of treating normal and unavoidable idle time costs:

Inflated Wage Rate Method: Under this method, normal and unavoidable hours are ascertained and the direct labor cost per hour is accordingly increased.

Overhead Method: Under this method, the cost of normal idle time is charged to works overhead account. But this method is less scientific since an element of direct cost is treated as indirect.

ACCOUNTING TREATMENT OF ABNORMAL IDLE TIME

There are also two methods of treating the abnormal idle time.

Overhead Method: under this method, cost of abnormal idle time is considered as a part of the works overhead. It will be better to apportion the idle time costs to different departments so that a clear picture may be available to the management so that it may take necessary remedial action.

Costing Profit and Loss method: Under this method, such costs are transferred to Costing Profit and Loss Account and thus these are treated as loss.

CONTROL OVER ABNORMAL IDLE TIME

Idle time can be controlled, thus:

(i) There must be planned production and proper supervisions, so that idle time will be reduced to a minimum level.

(ii) Jobs in hand should be planned in such a manner that the workers do not have to wait for the work.

(iii) Instructions and drawing must be clear so that the workers are not confused or have to wait for clarifications.

(iv) Proper inspection and maintenance of the power plant must be made to avoid frequent power failure.

(v) Timely supply of materials, proper maintenance of plant and machinery, adequate power supply will no doubt reduce the abnormal idle time.