PROVISIONS MEANING

Provisions meaning states the amount set aside by charging to the Profit and Loss Account, to provide for any known liability, the amount of which cannot be determined with accuracy.

ACCORDING TO COMPANIES ACT 2013:

“Provision usually means an amount written off or retained by the way of providing depreciation, renewals or dimunitions in the value of the assets or retained by the way of providing any known liability, of which the amount cannot be determined with the substantial accuracy.”

FEATURES OF PROVISIONS

The features of provisions are:

1. CREATED OUT OF PROFITS: Provisions are created out of profits for the current year and recorded in profit and Loss Account.

2. CREATED TO MEET KNOWN LIABILITY: The provision is created to meet the known liability.

Example: Provision for Taxation, Provision for bad debts, Provision for discount on debtors.

3. ESTIMATED AMOUNT: The exact amount of anticipated loss or expense or depletion in the value of asset cannot be determined with the reasonable accuracy.

4. CHARGE AGAINST PROFITS: All provisions are charged to Profit and Loss Account or Statement of Profit and Loss. This leads to reduction in the profits of the year in which they are created.

TYPES OF PROVISIONS

The provisions are created as a charge against profit. These are as follows:

PROVISION FOR BAD DEBTS AND DISCOUNT ON DEBTORS

The conservatism convention requires that the business should not anticipate any profit but provide for all losses. It means if there is any possibility of bad debts or discount on debtors in the future, a provision should be created for likely bad debts and likely discount to be allowed for debtors. Such provisions are charged to Profit and Loss Account.

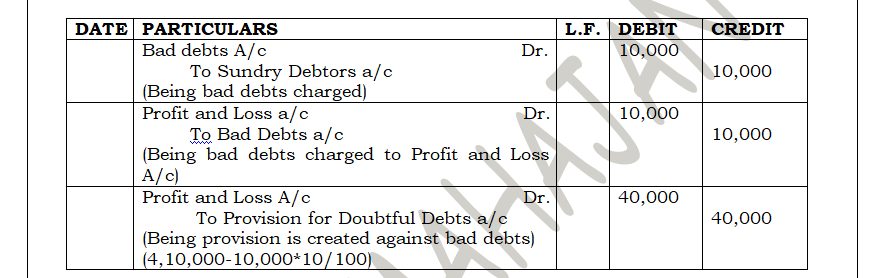

EXAMPLE: Suppose the debtors of the company are ₹4,10,000 out of which ₹10,000 are bad debts. Create a provision for 10% and pass the necessary journal enteries:

PROVISION FOR TAXATION

The tax liability for income tax can be ascertained only after the preparation of final accounts of that year. That means the income tax for a year can be ascertained only after preparing the income statement for the year and paid in the next year.

ACCOUNTING TREATMENT

OBJECTIVES OF CREATING PROVISIONS

The following are the objectives or needs to create the provisions:

1. TO ASCERTAIN TRUE PROFITS OF THE FIRM:

The true profits of the business enterprise can be ascertained only when all the expenses and all the provisions for known liabilities have been charged to Profit and Loss Account.

2. TO ASCERTAIN TRUE FINANCIAL POSITION OF THE BUSINESS:

The balance sheet will depict the true and fair view of the financial position of the business only if adequate provision has been made for all the anticipated losses and expenses.

3. REQUIREMENT AS PER CONCEPT OF ‘PRUDENCE’:

Provision help in following the Prudence Concept which states:

“Anticipate no profits but provide for all possible losses”

So, Provisions are created to provide the funds for all the upcoming known losses which may arise.

4. HELPS TO MAINTAIN THE CAPITAL INTACT:

In the absence of provision, any loss or depletion in the value of an asset would affect the capital of the business in the form of gradual decrease in the capital. Creation of provisions helps to maintain the capital of the business intact.

5. TO PROVIDE FOR KNOWN LOSSES, EXPENSES OR LIABILITIES:

A business enterprise needs funds to meet the known losses, expenses or liabilities in the future. This is why provisions are made to provide funds for meeting such losses or liabilities.

Thanks