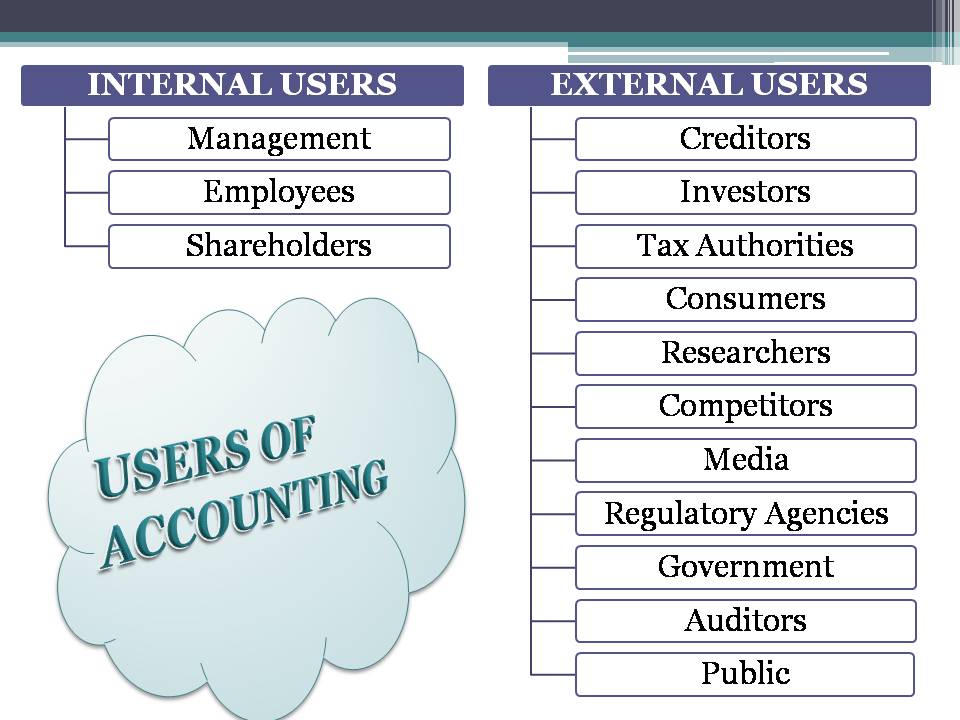

USERS OF ACCOUNTING

Accounting provides the information to the users of the business. Various users are interested to know about the financial position of the business, which they get from the accounting records kept by the business and provided to them by way of publishing final accounts.

The users of accounting are as follows:

INTERNAL USERS

Internal users are the users who work in the organization and have direct interest in the working of the company. The various internal users are as follows:

OWNERS/ SHAREHOLDERS

Shareholder or the Owners are the persons who have invested their money in the business. These persons are interested in knowing the accounting information for following purposes:

- To keep an eye on the financial health of the business.

- To ensure the return on their funds invested.

- To ensure the optimum utilization of the funds.

- To determine the exposure of risk to the funds invested by them.

- To determine the profit earning capacity of the business.

MANAGEMENT

There are three levels of management: Top, Middle and Low level of management. This is the most active user of the accounting information. Management needs the accounting information for following purposes:

- Selecting out alternative proposals.

- Controlling, acquisition and maintenance of inventories, cash receipts and payments.

- Planning or budgeting for the future.

- For checking the profit earning capacity of the business.

- To ensure the fair return on the equities invested by the shareholders.

- For managing the finances properly.

EMPLOYEES

Employees are other internal users of the accounting information. Employees are the persons who work in the organization in consideration of salaries and wages. The employees need the financial information due to the following reasons:

- To demand the bonus in case company is earning supernormal profits.

- To ensure job security.

- To know better about the company’s financial position.

EXTERNAL USERS

External users are not directly associated or work in the organization. They may have direct or indirect interest in the working of the organization. These users are as follows:

CREDITORS

Creditors are the lenders of the business. The creditor may be:

Short term Creditors who supplies the raw material or goods to the company or business on credit basis.

Long term creditors that provide funds to the business by subscribing the debentures or bonds of the company or by granting the loans.

The creditors need the financial or accounting information of the business for the following reasons:

- To know the credit worthiness of the business.

- To ensure the repayment of the credit provided.

- To assess the risk associated with the credit provided.

- T o know the existing debt service capability of the firm.

- To know the existing loan amount raised by the company from other sources.

INVESTORS/ POTENTIAL INVESTORS

Investors are the persons who have invested their funds in the business.

Potential investors are the investors who have not invested their funds in the business but are planning to invest in the business. These parties need the accounting information for varied reasons which are as follows:

- To judge the future prospects of earning on investment.

- To decide whether to invest more in the business or not.

- To make the decision regarding holding the existing investment or to sell it.

TAX AUTHORITIES

Tax authorities include the Income Tax authorities, Goods and Service Tax authorities, Custom duty Authorities, Corporate Tax Authorities etc. These authorities require the accounting information:

- To assess the tax liability of the business.

- To audit the records and imposing the penalties if any default is there.

CONSUMERS

Consumers are the persons who consume the goods and services provided by the business house. These parties are interested to know the financial position of the business to get an idea about the price structure of the products manufactured by the companies. Also the consumer protection associations require accounting data to get to know about the social responsibility initiatives taken by the company in favor of the consumers.

RESEARCHERS

Research scholars make use of the accounting information to conduct the various researches. The information regarding various companies is a mirror of the business environment. Accounting information is needed to conduct researches regarding

- Capital structure theories

- Assets management

- Credit rating

- Risk management

- Social responsibility initiatives etc.

COMPETITORS

Competitors are the rivals in the same business line. The competitors need the accounting information to draw out the plans that will make them more successful than any other firm in the same business. Competitors make analysis of the financial position of the other firms to know about the strengths and weaknesses.

MEDIA

The newspapers and various TV channels related to the economics and finance need information for publishing or telecast the achievements, performance and problems of companies. Accounting provides such information to the users. Also, the share of each company in the nation development or GDP can be ascertained on the basis of the accounting information provided in the accounting records.

REGULATORY AGENCIES

Regulatory agencies include Chambers of Commerce, various authorities under the various Acts, SEBI, Ministry of Labor, Ministry of Industries, FICCI etc. These agencies require the accounting information to check whether the company is complying with the legal provisions laid down under the legal and regulatory framework or not. These authorities also make a check on the fraudulent and unlawful sources of income of the business houses.

GOVERNMENT

Government ensures that a company’s disclosure of accounting information is in accordance with the regulations that are in place to protect the interest of various stakeholders who rely on such information in forming their decisions.

Government defines and monitors accounting limits such as sales revenue and net profit to determine the size of each business for the purpose of ensuring that it complies with the relevant employee, consumer and safety regulations.

AUDITORS

External auditors examine the financial statements and the underlying accounting record of businesses in order to form an audit opinion.

Investors and other stakeholders rely on the independent opinion of external auditors on the accuracy of financial statements.

PUBLIC

General public may also be interested in accounting information of a company. These could include journalists, analysts, academics, activists and individuals with an interest in economic developments.