DIFFERENCE BETWEEN HIRE PURCHASE AND INSTALMENT

Before understanding the difference between Hire purchase and Instalment, both concepts must be understood:

HIRE PURCHASE SYSTEM

Hire Purchase system is a system in which the goods are delivered to the purchaser at the time of agreement before the payment of instalments but the title of the goods is transferred after the payment of all instalments as per the hire purchase agreement. It is a special system of purchase and sale of goods. Under this system the purchaser pay the price of goods in instalments.

CONDITIONS OF HIRE PURCHASE AGREEMENT

Hire purchase is a transaction where the goods are sold by vendor to the purchaser under the following conditions:

- The goods will be delivered to the purchaser at the time of the agreement.

- The purchaser has a right to use the goods delivered.

- The price of the goods will be paid in the instalments.

- Every instalment will be treated to be the hire charges of the goods which is being used by the purchaser.

- If all the instalments are paid as per the terms of agreement, the title of the goods is transferred by the vendor to the purchaser.

- If there is default in the payment of any of the instalments, the vendor will take away the goods from the possession of the purchaser without refunding him any amount received earlier in the form of instalments.

INSTALMENT SYSTEM

An instalment system is a credit sale system in which payments are made in instalments over a period of time. In this system, the buyer gets the possession of the goods as well as the ownership of the goods right at the time of signing the agreement. During the course of paying the instalment, the vendor cannot responses to the goods. In that case, the vendor can sue the buyer only for the recovery of dues.

FEATURES OF INSTALMENT SYSTEM

- Instalment purchase system is just like an outright credit sale of goods.

- The buyer makes the payment in different instalment over a periods of time as agrees upon in the agreement.

- Under instalment system, the buyer gets the immediate possession as well as the ownership of the goods.

- The seller cannot claim the good back if the buyer made default in the payment of instalment.

- In case of default in the payment of instalment, the total amount of instalments already paid by the buyer cannot be forfeited.

- Under this system, the buyer can sell or mortgage the goods as the ownership is with the buyer.

- Risk of the goods/ assets are to borne by the buyer just after signing the agreement.

- The buyer of the goods under this system has no right to return the goods to the seller.

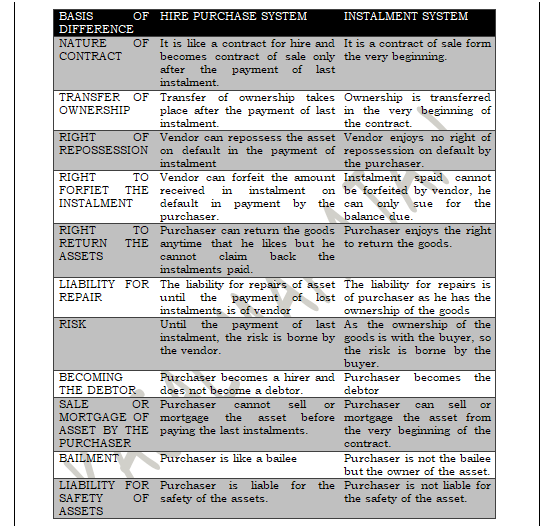

DIFFERENCE BETWEEN HIRE PURCHASE SYSTEM AND INSTALMENT SYSTEM

CONCLUSION

In the essence. the hire purchase system is suitable for the buyers who need the asset for the short period or are not sure of long term needs. The cushion of returning of the asset gives them leverage.

Instalment system is useful for those who are sure of utilizing the asset till its lifetime and those who are capable of taking the responsibility of assets in terms of its repairs and maintenance and wear and tear.