MEANING

Voyage Account is an account which is prepared by the shipping companies. This account is prepared to get a complete record of the profits earned and loss incurred on the particular voyage undertaken by the shipping company. It records both inward and outward journey. It is prepared separately for each voyage.

FEATURES OF VOYAGE ACCOUNT

NATURE OF ACCOUNT: Voyage Account is a nominal account. It is prepared on the basis of rule of Nominal Account which is as follows:

DEBIT ALL EXPENSES AND LOSSES

CREDIT ALL INCOMES AND GAINS

PREPARATION OF ACCOUNT: Voyage Account is prepared by the shipping companies or marine business companies to record the details of the particular voyage.

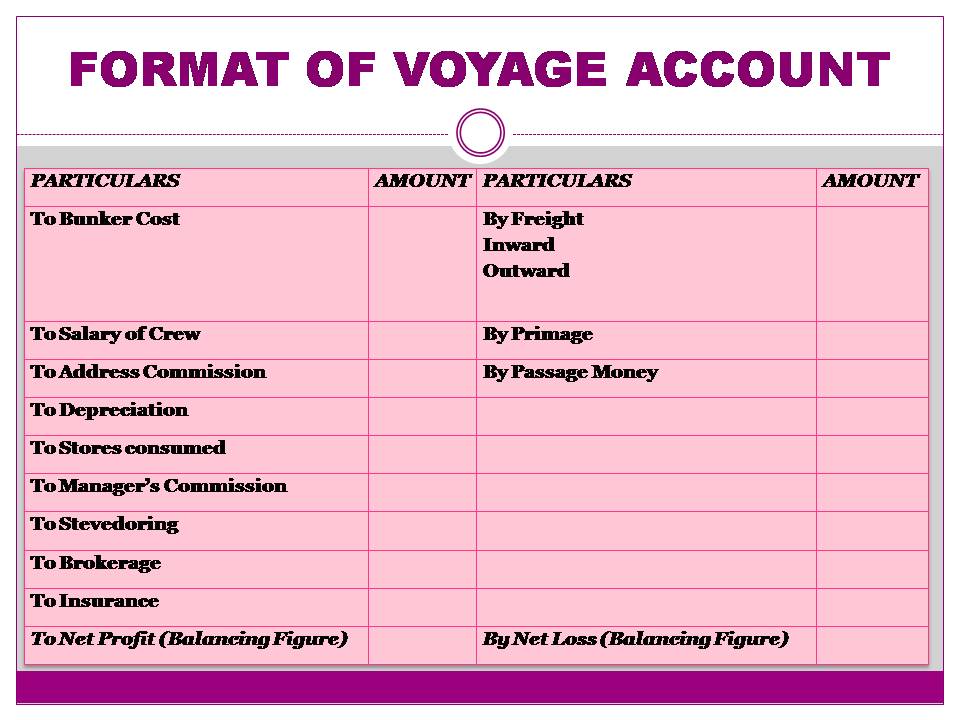

EXPENSES RELATED TO VOYAGE: Voyage account records all the expenses on the debit side. The expenses related to voyage are as follows:

Address commission: This is the commission which is paid to the agents who book the freight for the shipping companies. It is calculated as a percentage of freight and primage.

Address Commission= (Freight+ Primage)* Rate/100

Port Charges: The charges which are paid to the port authorities to use the port for loading and unloading the cargo from the ship.

Insurance: Expenses of premium paid to Insurance Company for the insurance of ship and freight are also debited to Voyage Account. But its premium is paid for a year. It should be adjusted according to the period of voyage.

Depreciation: Depreciation is the decrease in the value of the ship due to its use during the voyage. It is a non-cash expense and posted on the debit side of the voyage account.

Stores: Stock of store is purchased during the year for the use during the period of voyage. Stores consumed is calculated as:

(Opening stock+ Net Purchases- Closing Stock)

Stevedoring: Stevedoring are the charges of loading and unloading of the cargo on and from the ship. It is calculated usually on the unit basis. Example: If the stevedoring charges are Rs. 2 and units loaded are 1,000, then stevedoring is 10,000*2= Rs. 20,000.

Lighterage: The ship usually remains at a distance from the port in deep water. For loading and unloading the cargo, the big ships take the help of the small ships known as Lighter. The charges paid for these lighter is known as Lighterage.

Crew: Crew means staff working on the ship.

INCOMES RELATED TO VOYAGE: All the incomes related to voyage are recorded on the credit side of the voyage account. The incomes are as follows:

Freight: Freight is the amount earned by the shipping companies on the cargo delievered. Freight is of two types:

- Freight Inward: Earned on return journey.

- Freight Outward: Earned on outgoing journey.

Primage: Primage is also known as surcharge. It is the additional freight collected as a percentage of the amount of the freight. It is calculated as:

Primage= Freight*Rate/100

Passage money: The ships also carry some passengers along with the cargo on every voyage. The amount charged from the passengers on board is known as passage money.

RESULT: The voyage account shows the profit and loss on each voyage separately. Excess of incomes over expenses is known as profit and excess of expenses over income is known as loss.

PREPARATION: The voyage account is prepared separately for each voyage. It is not prepared on periodical basis rather records all the incomes and expenses on voyage or shipment basis.

FORMAT OF VOYAGE ACCOUNT