RESERVES ACCOUNTING

It refers to the amount set aside out of profits of the business to strengthen its financial position or to meet future contingencies or losses. Reserves Accounting aims to provide the firm with sufficient finance to safeguard itself for upcoming adverse situations.

Usually the firm does not distribute the whole amount of profits. It retains the amount of profits to use it for upcoming contingent losses and future projects. The creation of reserves are

- For redeeming liabilities

- To replace the depreciable assets

- For declaring uniform rate of dividend throughout the years.

Reserves are created only in that year in which the firm earns sufficient profit. It means no reserves can be created in the year firm suffers losses.

ACCORDING TO WILLIAM PICKLES

“Reserves mean the amount set aside out of profits and surpluses which are not earmarked in any way to meet any particular liability, known to exist on the date of the balance sheet.”

FEATURES

- APPROPRIATION OF PROFITS: Reserve is an appropriation of profits as it is credited out of divisible profits.

- CREATED VOLUNTARILY: Reserves are created voluntarily to strengthen the financial position of the business.

- RESERVES ACCOUNTING: These are shown on the Liabilities side of the Balance Sheet as reserve is a part of profit, which would have been distributed otherwise.

- RESERVE FUND: The investment of reserve amount in outside securities is Reserve Fund.

- CREATED TO MEET UNKNOWN LIABILITY: Reserve is not created to meet any known liability or depreciation in the value of assets but for meeting an unknown liability or loss in the future.

OBJECTIVES OF CREATING RESERVE

The objectives of making reserves are as follows:

- Expansion of business through internal sources i.e. ploughing back of profits.

- To strengthen the financial position of the business.

- To increase the working capital of the business.

- For meeting future contingencies.

- To meet any unknown liability or loss

- To replace as wasting asset.

TYPES OF RESERVES

OPEN RESERVE

Those reserves which are specifically created by debiting the Profit and Loss Account and shown specifically on the Liabilities side of the Balance Sheet are called Open Reserves or Published Reserves.

The Open reserves are of two types which are as follows:

A. CAPITAL RESERVE

Capital Reserves are the reserves created out of capital profits. These reserves are not made available for distribution as dividend among the shareholders.

Examples of capital profits out of which capital reserve is maintained:

Profit on:

- Sale of fixed assets.

- Sale of investments.

- Redemption of debentures.

Objectives of creating capital reserves:

- To help in making the organization financially strong.

- To help in writing off the capital losses.

- To help in issue of fully paid bonus shares to existing shareholders.

Disadvantages of capital reserves:

- Reserves are not made available for distribution to shareholders.

- It does not give any indication of operating efficiency of the business.

- It does not help in making the management responsible to sell old assets at satisfactory price.

B. REVENUE RESERVE

Revenue reserves are the reserves set aside out of revenue profits which are available for distribution as dividend.

ACCORDING TO KOHLER

“A revenue reserve is that portion of the net worth or total equity of an enterprise representing retained earnings available for withdrawal by the proprietors.”

TYPES OF REVENUE RESERVES

1. GENERAL RESERVE

It is the reserve created out of the profit not for any specific purpose. Revenue reserve is called ‘Contingency Reserve’.

Objectives of creating General Reserve:

- To strengthen the financial position of the business.

- To meet the unknown and unexpected liabilities or losses.

- To provide the funds for the expansion and development of the business.

Disadvantages of General reserves:

- It reduces the available profits to be distributed to the shareholders.

- It shows the position of the business better even in the years of the loss.

- It leads the management for unfair use of reserve to maintain the reputation of the business.

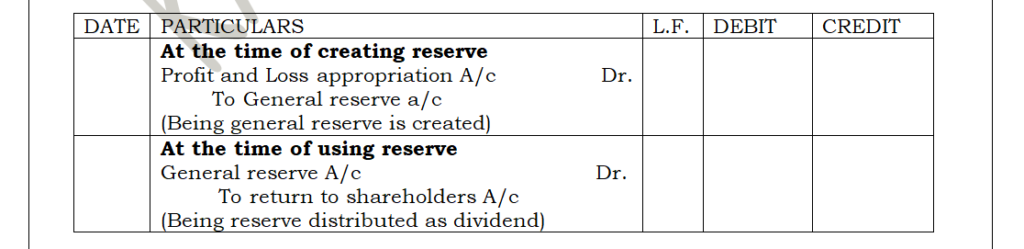

General Reserves Accounting:

2. SPECIFIC RESERVE

It is the reserve set aside for a specific purpose, which can be utilized only for that purpose.

Examples of Specific Reserve are:

- Dividend Equalization Reserve: It is created to maintain a steady dividend rate. This reserve is utilized in the year in which profits are insufficient.

- Debenture redemption Reserve: It is created to provide funds for the repayment of debentures.

- Workmen Compensation Reserve: It is created to meet the compensation payable to workers. Example: Case of an accident.

- Investment Equalization Reserve: It is created to provide for decline in the value of investments arising out of market fluctuations.

Objectives of creating Specific Reserves:

- Providing enough funds for replacement of assets at the end of their useful life.

- To provide enough cash for redemption of debentures or preference shares or loans with due date.

- Helps in maintaining future credibility of business.

3. RESERVE FUND

Reserve invested in outside securities and earmarked for a particular purpose is Reserve Fund. A company prefers to invests the reserves in outside securities to earn surplus over it.

- Cash is available for investment.

- Funds cannot be profitably invested in the business itself.

Advantages of Reserve Fund

- Regular income earned from securities.

- Investments having been made in government securities, the amount of reserve is quite safe.

- There may be a profit on sale of investments, if market price of securities rises. There can also be a loss, if market price falls.

Example: SINKING FUND

It is a specific reserve set aside out of the annual profits. It is usually invested in outside securities. The investment in outside securities is made to earn interest and to provide cash in case needed.

It is of two types:

- Sinking Fund for Replacing Assets

- Sinking Fund for Redeeming Liabilities

The fund which is created to provide enough finance for the replacement of the fixed assets at the end of their useful life is known as Sinking Fund for Replacing Assets.

The fund which is created with a view to enable the business to pay out its loan within due date is known as Sinking Fund for Redemption of Liabilities.

Objectives and Advantages of creation of Sinking Fund

- This fund provides enough finance for replacement of assets at the end of the useful life of asset.

- This fund makes enough cash available for the redemption of Preference Shares and Debentures.

- This fund helps in maintaining future credibility of the business.

Disadvantages of Sinking Fund

- It reduces the divisible profits to be distributed to the shareholders.

- It is difficult to estimate the amount of fund required to replace the fixed assets in future.

- It is very difficult to maintain accounts for Sinking Fund.

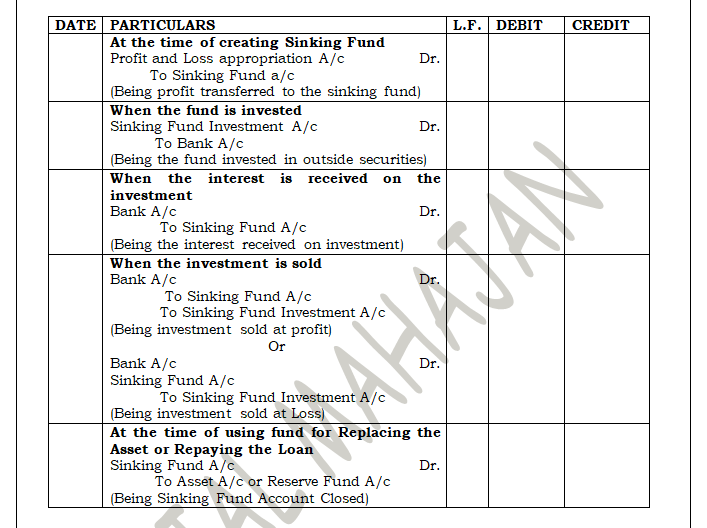

Accounting Treatment for Sinking Fund

SECRET RESERVES

Secret reserves are the reserves which are not shown in the balance sheet. They are created by showing the profit as figure much lower than actual or by showing asset at a lower figure or liabilities at a higher figure. It is also known as ‘Hidden Reserve’ or ‘Internal Reserve’

Methods of creating Secret Reserves/ Secret Reserves Accounting:

- By providing excessive depreciation.

- By creating more provision than actually required.

- Treating a revenue receipt as capital receipt.

- Undervaluation of assets.

- Charging capital expenditure to revenue expenditure.

- Showing contingent liabilities as actual liabilities.