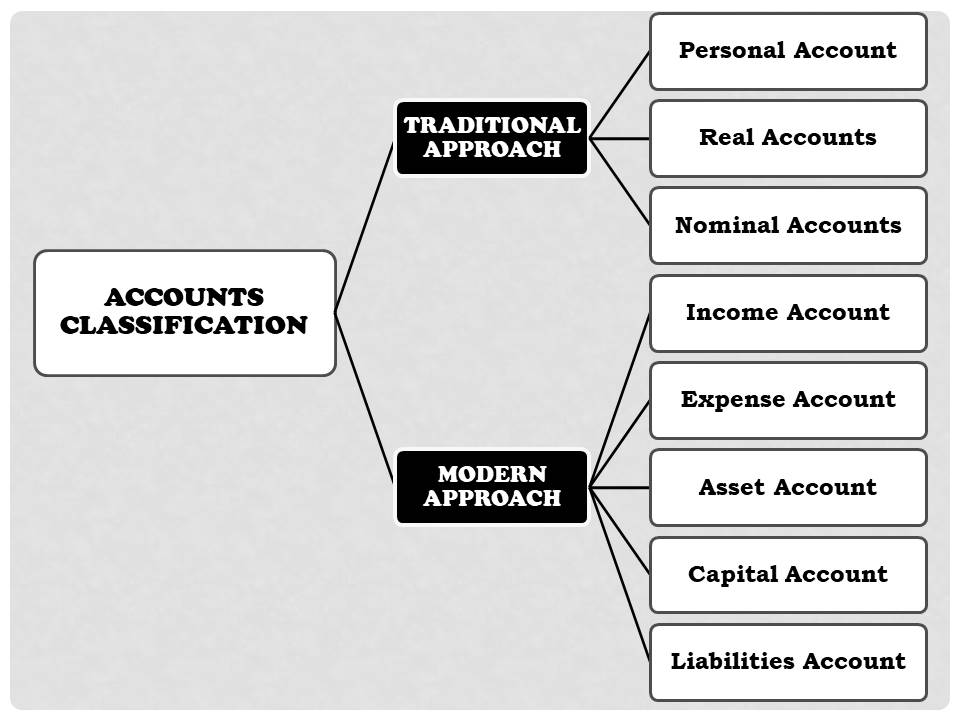

Golden rules of Accounting

The golden rules of Accounting are the foundation or base of the accounting which helps in posting the transactions correctly in the books of accounts. The golden rules of accounting are as follows:

TRADITIONAL APPROACH

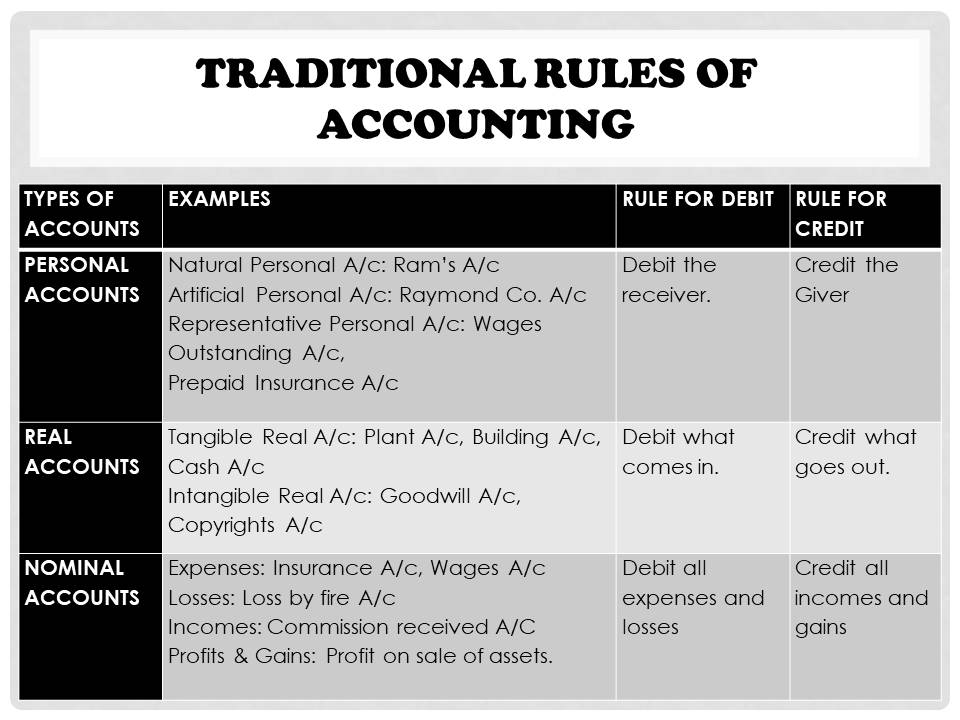

Under the traditional approach, the accounts are divided into three parts. The golden rules of accounting are as follows:

PERSONAL ACCOUNT

These accounts are related to the individuals, firms, societies, clubs, hospitals etc. The personal accounts can be:

- Natural Personal Accounts

- Artificial Personal Accounts

- Representative Personal Accounts

The rule for personal account is:

DEBIT THE RECEIVER

CREDIT THE GIVER

According to the rule of ‘Debit the Receiver’, the personal account of a person to whom we give some money or goods is debited.

Example: If we gave ₹20,000 to Gopal, the entry will be:

Gopal A/c Dr. 20,000

To Cash A/c 20,000

(Being cash paid to Gopal)

In the same way, according to the rule ‘Credit the giver’, the personal account of the person from whom we receive some money or goods is credited.

Example: If we received ₹50,000 from Govind, the entry will be:

Cash A/c Dr. 50,000

To Govind 50,000

(Cash received from Govind)

REAL ACCOUNT

Real Accounts are the accounts related to the assets and liabilities of the business. There may be tangible Real Accounts or Intangible Real Accounts. The rule for Real Accounts is as follows:

DEBIT WHAT COMES IN

CREDIT WHAT GOES OUT

According to the rule of ‘Debit what comes in and credit what goes out’, the account of the cash or other property which is received by the business firm is debited and in the same way, the account of the Cash or other property which goes out of the business is credited.

Example: Machinery purchased for ₹50,000

Machinery A/c Dr. 50,000

To Cash A/c 50,000

(Machinery purchased for cash)

NOMINAL ACCOUNT

These accounts related to the expenses, incomes, profits and losses of the business. These accounts are Wages Account, Loss of goods by fire Account, Interest Received Account, Repairs Account, etc. the rule for Nominal Accounts is as follows:

DEBIT ALL EXPENSES AND LOSSES

CREDIT ALL INCOMES AND GAINS

According to the rule of ‘Debit all Expenses’, the accounts of all expenses and losses are debited.

Example: Salary paid ₹20,000

Salary A/c Dr. 20,000

To Cash A/c 20,000

(Salary paid in cash)

Similarly, according to the rule of ‘Credit all Incomes’, the accounts of all the incomes and profits are credited.

Example: ₹5,000 is received for commission. The entry will be:

Cash A/c Dr. 5,000

To Commission A/c 5,000

(Commission received)

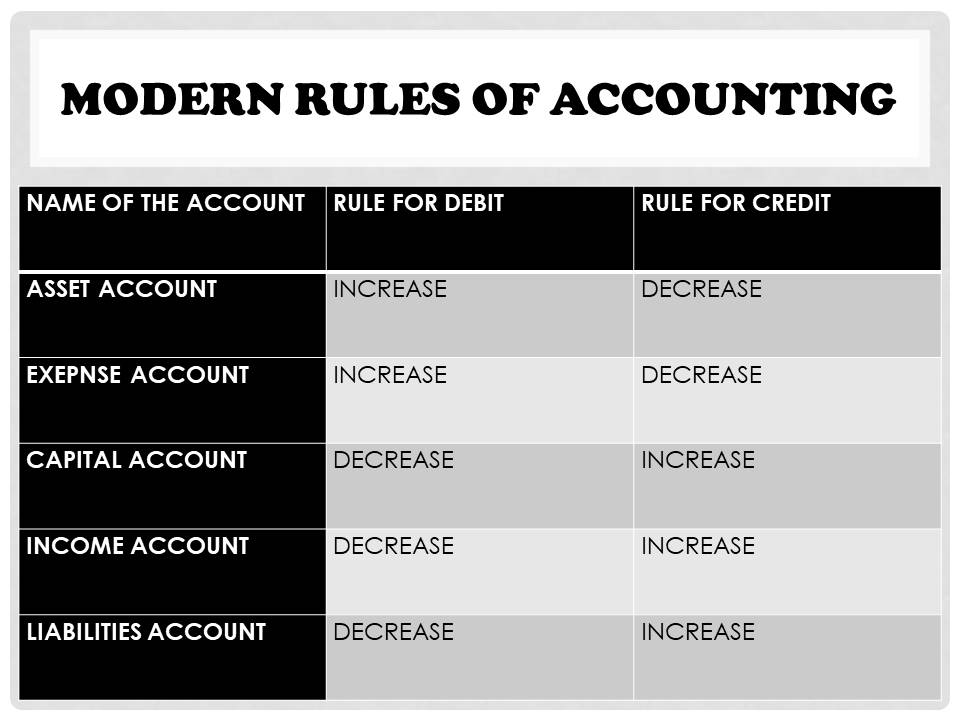

MODERN APPROACH

Under this system, the accounts are divided into 5 categories which are as follows:

ASSET ACCOUNT

An asset is any owned physical object or right, having a money value. These are the economic resources which are owned by a business and from which future economic benefits are expected to flow to the enterprise. The rule for asset account is as follows:

DEBIT THE INCREASE

CREDIT THE DECREASE

Example: Cash A/c, Furniture A/c, etc.

CAPITAL ACCOUNT

The amount invested by the owner in the business is known as Capital Account. It may be invested in cash or kind. The rule for this account is as follows:

DEBIT THE DECREASE

CREDIT THE INCREASE

LIABILITIES ACCOUNT

It refers to an amount owing by one person to another payable in money, goods or services. The rule for Liabilities Account is:

DEBIT THE DECREASE

CREDIT THE INCREASE

Example: Bank overdraft A/c, Loan A/c, etc.

EXPENSE ACCOUNT

Expense is that portion of the expenditure which has been consumed during the current accounting period to earn revenue. Since expenses are the cost of goods and services used up, they are also called expired cost. The rule for Expense Account is as follows:

DEBIT THE INCREASE

CREDIT THE DECREASE

Example: Rent A/c, Insurance A/c, Advertisement A/c, etc.

INCOME ACCOUNT

Income is the increase in the net worth of the enterprise from business or non- business activities. It is wider term which includes profits also. The rule for Income Account is:

DEBIT THE DECREASE

CREDIT THE INCREASE

Example: Interest received Account, Commission Received Account, Dividend Received A/c.

DESCRIPTION : Golden rules of accounting