HIRE PURCHASE

Hire Purchase system is a system in which the goods are delivered to the purchaser at the time of agreement before the payment of instalments. However, the title of the goods is transferred after the payment of all instalments as per the hire purchase agreement.

It is a special system of purchase and sale of goods. Under this system the purchaser pay the price of goods in instalments.

CONDITIONS OF HIRE PURCHASE AGREEMENT

- Hire purchase is a transaction where the goods are sold by vendor to the purchaser under the following conditions:

- The goods will be delivered to the purchaser at the time of the agreement

- The purchaser has a right to use the goods delivered

- The price of the goods will be paid in the instalments.

- Every instalment will be treated to be the hire charges of the goods which is being used by the purchaser.

- If all the instalments are paid as per the terms of agreement, the title of the goods is transferred by the vendor to the purchaser.

- If there is default in the payment of any of the instalments, the vendor will take away the goods from the possession of the purchaser without refunding him any amount received earlier in the form of instalments.

FEATURES OF HIRE PURCHASE AGREEMENT

1. TRANSFER OF POSSESSION ONLY: The hire vendor transfers only the possession of goods to the hire purchaser immediately after the agreement of hire purchase is made.

2. GOVERNING ACT: Hire purchase system is governed under the Hire Purchase Act, 1972. This act came into force on 1 September, 1973.

3. CREDIT PURCHASE: Hire purchase is a system of credit purchase. It implies that the goods are sold for payment that is to be done in future period of time.

4. TERMINOLOGY: The terms used in the agreement of hire purchase are:

- Hire Purchaser: The buyer in the hire purchase agreement who purchases the goods on hire basis

- Hire Vendor: The seller in the hire purchase agreement who sell the goods on the hire basis.

- Cash Payment: The amount to be paid on outright purchase in cash.

- Down Payment: Initial payment made at the time of signing the hire purchase agreement.

- Hire Purchase Price: The amount to be paid if the goods are purchased under the hire purchase system. It includes cash price and interest on future instalments.

5. RIGHT TO TERMINATE: The hire purchase has a right to terminate the agreement at any time in the capacity of a hirer.

6. Goods should be delivered in the possession of the purchaser at the time of commencement of agreement.

7. Hire Vendor continues to be the owner of the goods as the last payment of instalment is over.

8. If there is default in the payment of any instalment, the hire vendor will take away the goods from the possession of the purchaser without refunding him any amount.

9. Each instalment consists of partly interest and part of capital payment.

ACCOUNTING TREATMENT

The accounting treatment is as under:

IN THE BOOKS OF THE HIRE PURCHASER

There are two methods of accounting in the books of the hire purchaser:

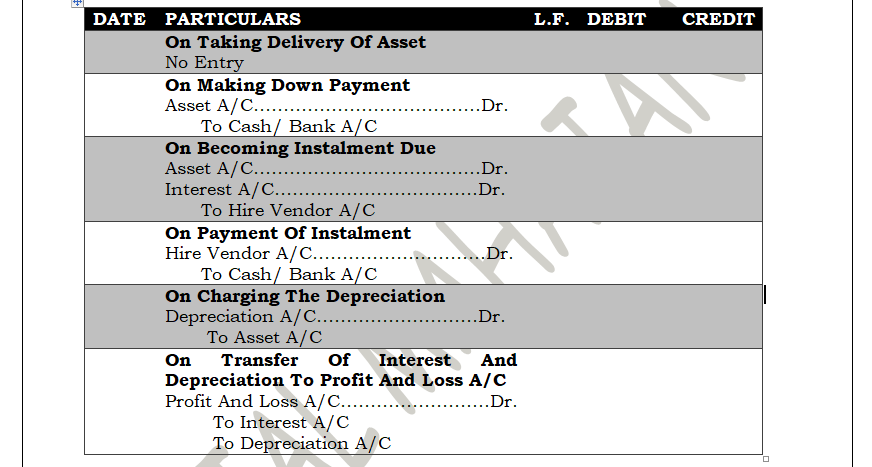

ASSET ACCRUAL METHOD

Under this method it is considered that the hire purchaser is the owner of the asset up to the value of cash price paid by him in the form of down payment or the cash price paid included in the various instalments.

The journal entries are recorded under this method are:

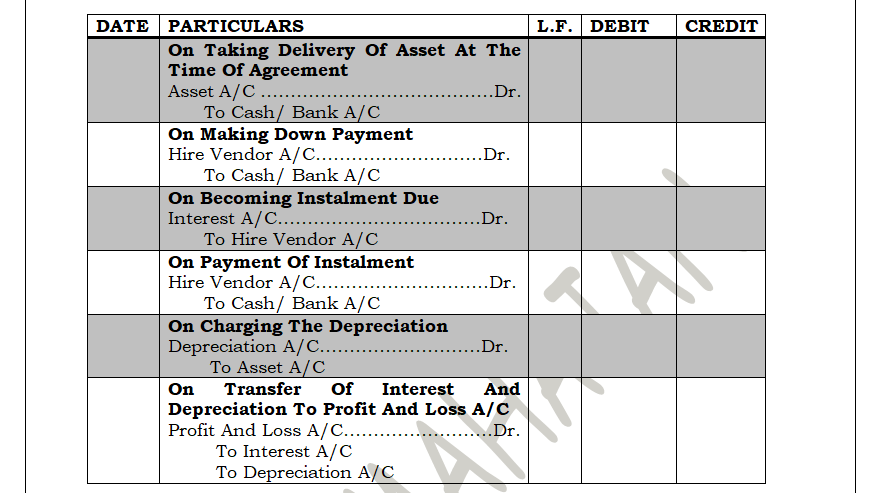

TOTAL ASSETS VALUE METHOD

Under this method of accounting in the books of hire purchaser, is done on the assumption that the ownership of the asset is also transferred to the purchaser with the delivery of goods. The journal entries to be passed are:

POSTING IN LEDGER ACCOUNTS

After passing the journal entries, the accounts opened in the ledger are as follows:

- Asset a/c

- Vendor’s a/c

- Interest a/c

- Depreciation a/c

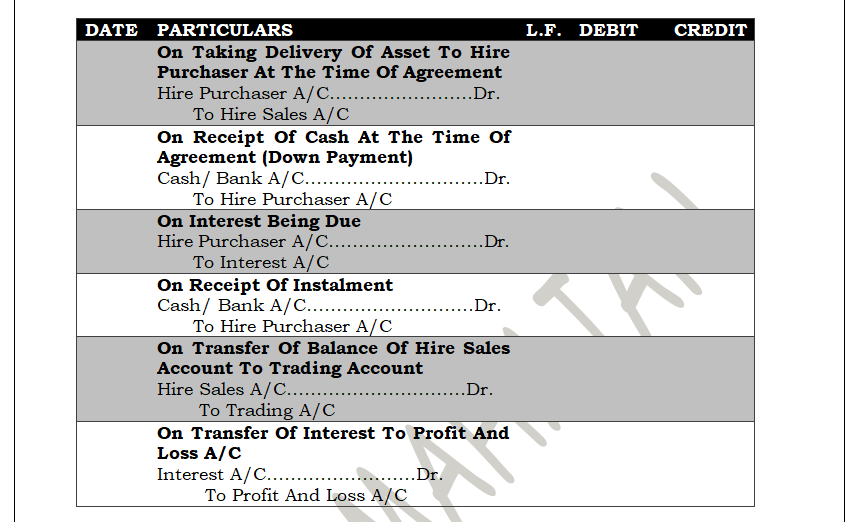

IN THE BOOKS OF THE HIRE VENDOR

There is only one method to record the journal entries in the books of hire vendor. The journal entries are as follows:

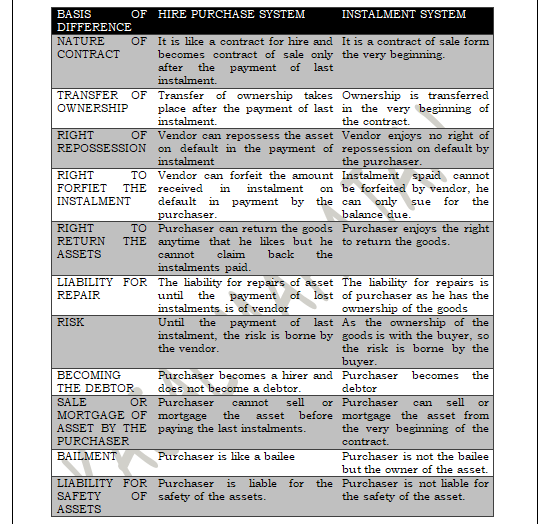

DIFFERENCE BETWEEN HIRE PURCHASE SYSTEM AND INSTALMENT SYSTEM

CONCLUSION

In the essence. the hire purchase system is suitable for the buyers who need the asset for the short period or are not sure of long term needs. The cushion of returning of the asset gives them leverage.

Instalment system is useful for those who are sure of utilizing the asset till its lifetime and those who are capable of taking the responsibility of assets in terms of its repairs and maintenance and wear and tear.

JOIN THE CHANNEL ON TELEGRAM

Pretty knowledgeable.

Thanks