TRANSACTIONS

Transactions refer to any exchange of goods and services on cash or credit basis by the business with the outside parties i.e. other business or customer. Transaction is an economic activity. It has an effect on the net worth or financial position of the business.

FEATURES OF TRANSACTION

The following are the features of transaction:

ECONOMIC ACTIVITY

Transaction is an economic activity. It includes the dealing such as purchase and sale of goods, lending or borrowing money etc. It does not include any kind of social activity such as inviting a friend to dinner or giving money as gift on some occasion.

IMPACT ON FINANCIAL POSITION

Transaction has a great bearing on the financial position of the firm. Each transaction may have little or great impact on the financial position of the firm. It results in either inflow or outflow of cash and inflow or outflow of goods and services.

MAY BE QUANTITATIVE OR QUALITATIVE

Transaction may be quantitative or qualitative. Quantitative transactions are those that involve the exchange of money. Example: purchase of furniture worth Rs. 5,000 for cash.

On the contrary, qualitative transactions are those that involve no exchange of money. Example: Depreciation or decrease in the value of the asset.

FINANCIAL CHANGE

Transaction brings financial change for the business or parties. Only that event is regarded as transaction that impacts the financial position. Example: Death of a debtor turns the amount due from him/her into bad debt, which is a monetary loss, hence regarded as transaction.

On the other hand, death of an inefficient employee leads to no monetary loss, hence not regarded as transaction.

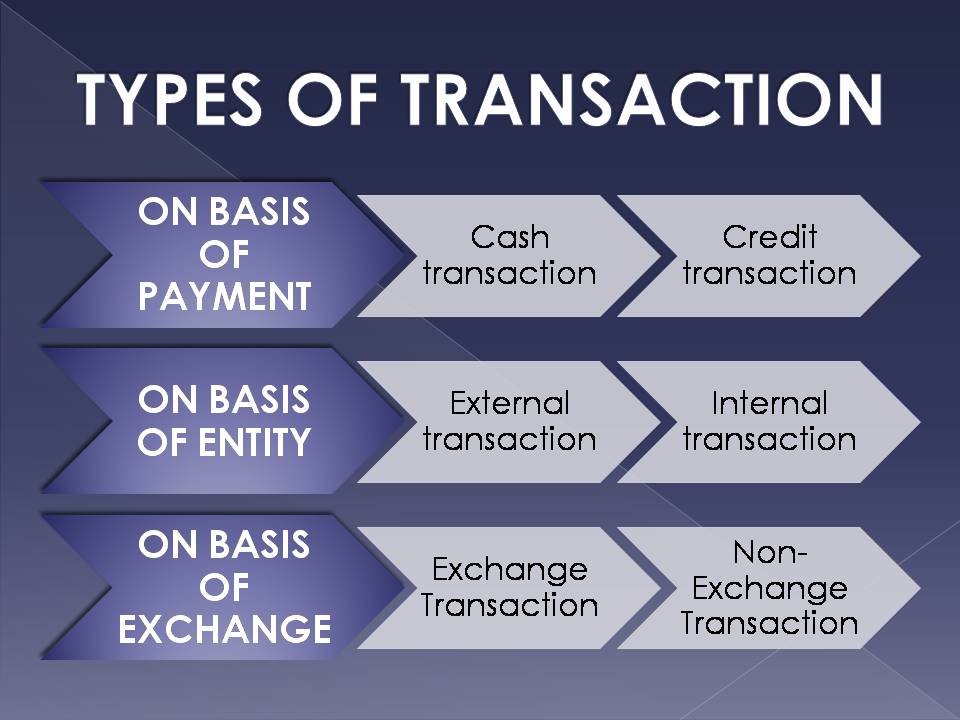

TYPES OF TRANSACTION

The following are the various types of transactions:

ON THE BASIS OF PAYMENT INVOLVED

CASH TRANSACTION: Cash transaction involves the inflow and outflow of the cash between the two parties. Example: Purchase of furniture worth Rs, 10,000 is a cash transaction as it involves payment of Rs. 10,000 in the form of cash.

CREDIT TRANSACTION: Credit transaction is the transaction that does not includes cash payments or receipts. It involves payment or receipt of cash on any future date. Example of credit transactions are:

- Purchase of goods on credit.

- Supply of goods on credit.

ON THE BASIS OF ENTITY INVOLVED

EXTERNAL TRANSACTION: These transactions are entered into with the parties that are external to the business. Example: sale of goods to customer.

INTERNAL TRANSACTION: These transactions are entered into within the organization of between the different departments of the organization. Example: Depreciation on machinery, supply of goods from department to another.

ON THE BASIS OF EXCHANGE

EXCHANGE TRANSACTION: These transaction leads to inflow or outflow of something. Example: Purchase of land. This leads to inflow of an asset i.e. land and outflow of cash.

NON-EXCHANGE TRANSACTIONS: This is one way transaction. It does not involve any kind of inflow or outflow. Example: Depreciation on machinery.