DEPRECIATION ACCOUNTING

Depreciation denotes the decrease in the book value of the fixed assets. It is the permanent and gradual decrease in the value of fixed assets. It is due to use, effluxion of time, obsolescence, expiration of legal rights or any other cause. Depreciation Accounting is done to provide the assets at true value in the books of accounts

METHODS OF CHARGING DEPRECIATION

There are various methods of charging depreciation like

- Straight Line Method

- Diminishing balance Method

- Sum of the years digit method

- Annuity method

- Sinking fund method

- Insurance Policy method

- Machine hour rate method

- Depletion method

- Revaluation method

- Mileage method

STRAIGHT LINE METHOD FOR DEPRECIATION ACCOUNTING

The Straight Line Method of charging depreciation has different names like Original Cost Method or Fixed Installment Method or Fixed Percentage Method.

In this method, a fixed proportion of the original cost of the asset writes off each year. The asset account reduced to its scrap value at the end of the estimated economic useful life. The assumption of this method is that the depreciation is a function of time.

CALCULATION

- Calculation of Amount of Depreciation

d= Cost of Asset- Residual Life/ No. of years of estimated useful lif

- Calculation of Percentage/ Rate of Depreciation

Rate of Depreciation= Amount of depreciation/ Original cost of Asset*100

Example: Calculate amount of annual depreciation from the following information:

The machinery costs ₹50,000 and its installation cost is ₹1,000. Estimated scrap value is ₹5,000.

Annual Depreciation= 50,000-5000/ 10= ₹4,500 per annum

Rate of Depreciation= 4,500/50,000*100= 9% per annum

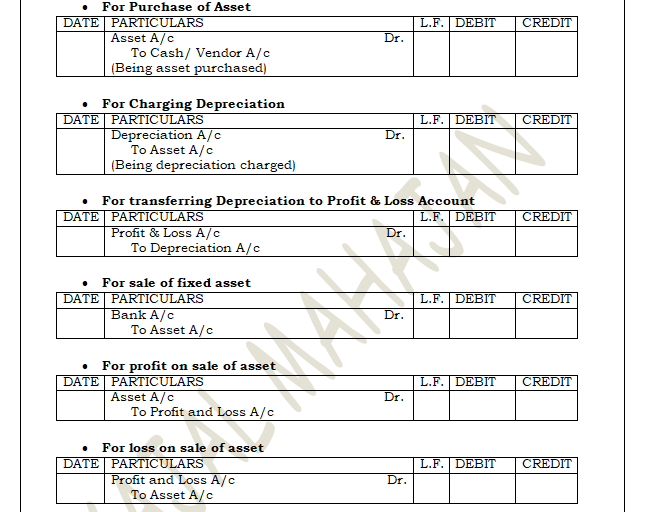

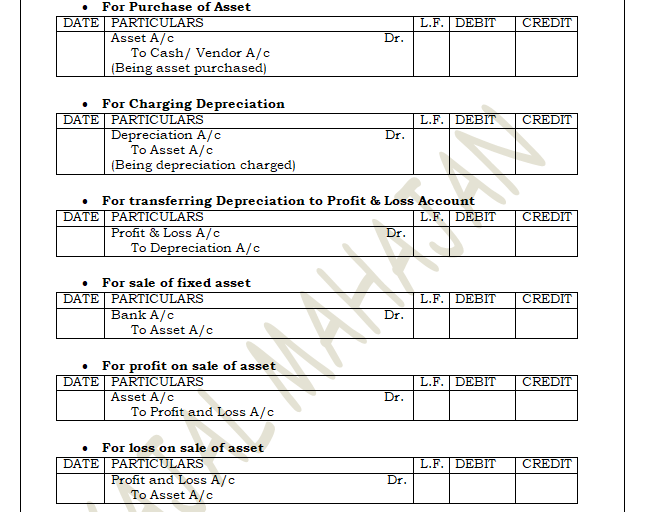

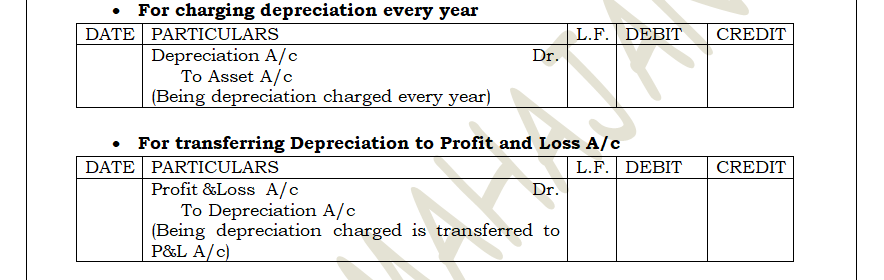

JOURNAL ENTERIES

ADVANTAGES/ MERITS OF STRAIGHT LINE METHOD

The following are the merits/ advantages of straight line method:

- SIMPLE: It is very easy method of providing depreciation and the calculations are very simple.

- ASSET FULLY WRITES OFF: In this method, the asset account writes off fully at the end of its useful working life.

- KNOWLEDGE OF TOTAL DEPRECIATION CHARGED: The amount of total depreciation charges to Profit and Loss Account. It can be easily ascertained by multiplying the annual installment of depreciation with the number of years, the machine has been used.

- SUITABLE FOR FIXED LIFE ASSETS: This method is very suitable for those assets which have a fixed working life. Eg: Lease, Furniture, Patents etc.

- Under this method, there is same effect on the Profit and Loss Account as same amount of depreciation charges every year.

DISADVANTAGES/ DEMERITS OF STRAIGHT LINE METHOD

- INTEREST ON CAPITAL: This method does not take consideration the interest on capital invested in fixed assets. Thus, the asset under-capitalizes and profits over-states.

- REPAIRS AND RENEWALS: As the amount of depreciation remains constant every year, the expenses on repairs and maintenance increase gradually. So, profit and loss account charges heavily in the later year.

- DECREASE IN UTILITY: Asset in the earlier part of its working life provides more utility than in future period when asset gradually becomes old. Thus benefit and cost do not matches rationally.

- NOT RECOGNISED BY TAX AUTHORITIES: Income tax Authorities do not recognise this system of depreciation.

- NO PROVISION FOR REPLACEMENT: The firms do not invests the amount of depreciation in outside business. So, there is no provision of funds for replacement of assets.

- The calculation of depreciation is difficult when there are different machines with different life spans.

- It is difficult to exactly estimate the scrap value of the assets.

SUITABILITY OF THIS METHOD

This method of charging depreciation is suitable where assets get depreciates with effluxion of time i.e. Patents, Leasehold etc. This method is also suitable for those assets which do not require much repairs and renewals. The firm follows this method where the repair charges are almost uniform throughout the life of the asset.

DIMNISHING BALANCE METHOD FOR DEPRECIATION ACCOUNTING

Diminishing Balance Method is the another method of depreciation accounting. It has different names like Reducing Balance Method or Written Down Value Method.

Under this method, a fixed percentage writes off each year on the balance of the asset, so that the asset reduces to its estimated scrap value at the end of the useful life.

As depreciation does not charge on the original cost of asset, the amount of the depreciation will be lesser and lesser as the time will pass. The book value of asset can never be zero under this method.

The factors taken into consideration while determining rate of depreciation are:

- Cost of Asset

- Estimated useful life of Asset

- Estimated Scrap Value

CALCULATION

Rate of Depreciation:

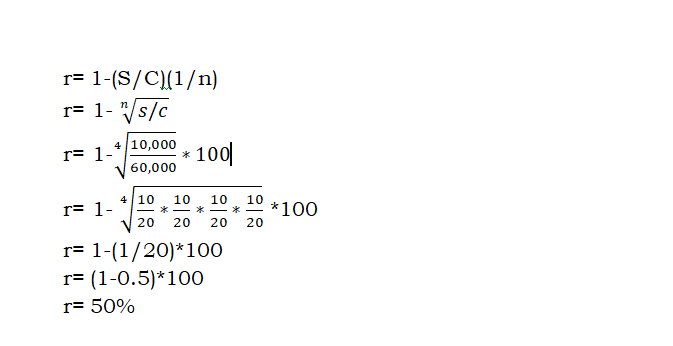

r= 1-(S/C)(1/n)

r= Rate of Depreciation

n= estimated useful life of asset

s= residual/ scrap value

c= original cost of asset

EXAMPLE: M/s Kavish Ltd. Purchased in machinery for ₹1,60,000 on 1st April, 2014. Its useful life is 4 years and scrap value is ₹10,000. Then the rate of depreciation will be:

JOURNAL ENTERIES

MERITS OF DIMNISHING BALANCE METHOD

- RATIONAL MATCHING: Under this method, the depreciation charges are high in earlier years when the machine is most useful and produce high revenues. Thus, the cost and revenues match rationally.

- OBSOLESCENCE: Obsolescence does not affect much because the major part of the asset writes off as depreciation. So, the management feels no difficulty in replacing the asset.

- RECOGNITION FROM INCOME TAX DEPARTMENT: This method assumes more significance because income tax authorities recognize this method for accounting purpose.

- SUITABLE FOR LONG LIFE ASSETS: This method is suitable for those assets which have long life.

- The amount of depreciation and repairs and maintenance part put some amount of burden on Profit and Loss Account. This is so because amount of depreciation goes on decreasing every year whereas cost of repair increases.

- Fresh calculations are not necessary when additions are there in the asset.

DEMERITS OF DIMNISHING BALANCE METHOD

- INTEREST ON CAPITAL: This methods ignores the interest on capital invested in fixed assets. As a result the profit over states.

- NO FUNDS FOR REPLACEMENT: This method does not solve the problem of availability of funds at the time of replacement of assets. the firms retains the amount of depreciation charged with itself.

- ASSET DO NOT REDUCES TO ZERO: The value of asset under this method never reduces to zero. Though the asset becomes useless after its working life is over but the book value does not extinguish.

- RATE OF DEPRECIATION: As compared to straight line method, it is difficult to calculate the rate of depreciation under this method.

- It ignores the actual use of the asset.

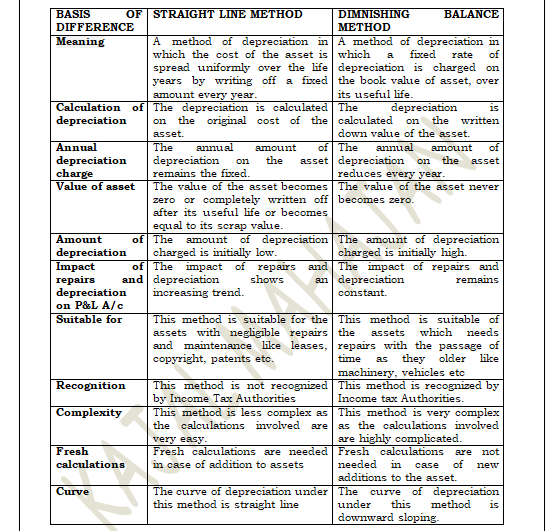

DIFFERENCE BETWEEN STRAIGHT LINE AND DIMNISHING BALANCE METHOD

Both Straight Line Method and Diminishing Balance Method have their own merits and demerits in providing the depreciation for the assets. The straight line method is very simple to understand and easy to calculate whereas the diminishing balance method is helpful in better matching of revenue and expenses derived from the asset by the company. Also, the income tax authorities prefer written down value method over the straight line method.

FACTORS CONSIDERED WHILE SELECTING DEPRECIATION METHOD:

CONVENTION OF CONSISTENCY:

Convention of Consistency means the accounting practice should stay the same from one period to another. It signifies that the use of same accounting techniques for assembling financial statement in different years. A business must use consistent approach in selecting a method for depreciating the group of assets i.e. different methods of depreciation applies to different group of assets. But the firm may use same method in successive years.

CONVENTION OF CONSERVATISM:

It is called ‘Doctrine of Prudence’. Convention of Conservatism states to anticipate all the future losses and ignore gains. This concept should apply not only in selecting the depreciation method, but also for estimated life and salvage value. Depreciation is purely an estimate. The amount of depreciation must not produce higher periodic expenses in order to avoid overstating profits.

INCOME TAX:

In financial accounting, income tax consideration for depreciation should be kept entirely separate. Two separate methods of depreciation can be used for business accounting and tax accounting. But for avoiding cost of maintaining two sets of records, a business may use same figures for both the purposes.

CALCULATION:

For avoiding separate calculation for each type of assets, a single, rate of depreciation is applied to all the assets of a business. Many business houses simply apply the same method to all the assets, ignoring the estimated lives and salvage values.

BENEFIT:

An asset provides service to the business more in earlier years than the later years. Also, repairs and maintenance increase through the life of an asset. Therefore, depreciation should be more in earlier years than in the later years.

CAUSE OF DECREASE IN THE VALUE OF AN ASSET:

The decline in the value of the asset may be a function of time or usage or extraction. The cause of depreciation should be kept in mind before applying the method of depreciation.

TECHNOLOGICAL INNOVATION:

Because of the technological innovation, a machine may become obsolete before its estimated economic life. If the probability of obsolescence is high in the near future, the estimated economic life should be shortened.

LAW OF THE LAND:

The Law of the Land may determine the method and specific rate of depreciation for a particular rate for particular business entities. Example: In India, for all limited companies, depreciation is to be calculated in accordance with the rates specified in the Schedule II of the Companies Act, 2013.

CFrom the above, it can be concluded that different considerations may indicate different depreciation methods. Therefore, in selecting a method, a clear choice must be made based on the relative importance of the considerations. It should be kept in mind that the cost of asset over its estimated economic life in a systematic and rational manner, so that costs should be matched with the expected benefits.

ACCOUNTING TREATMENT

There are two ways or methods of depreciation accounting:

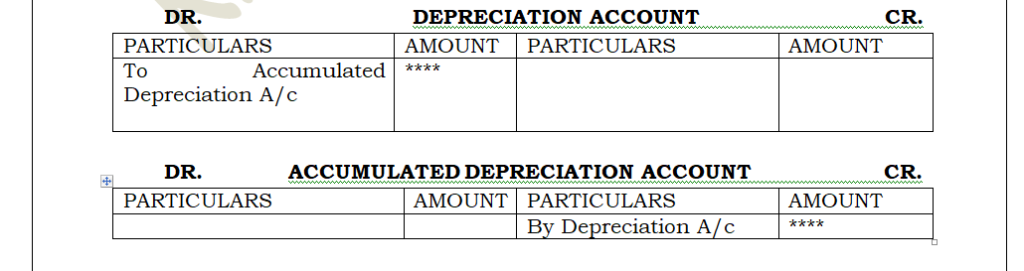

WHEN PROVISION FOR DEPRECIATION ACCOUNT IS MAINTAINED:

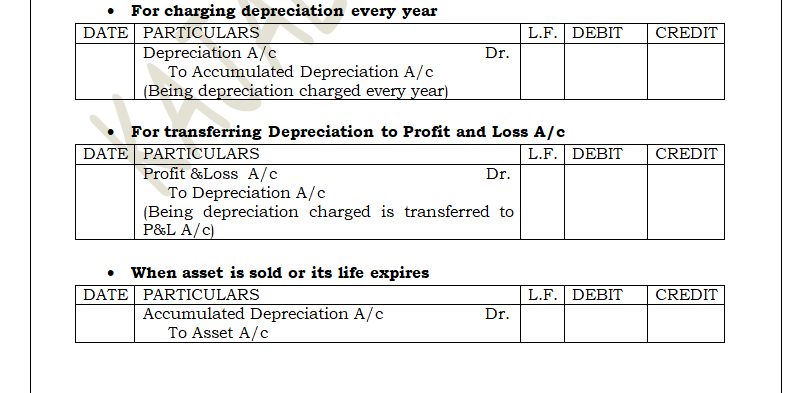

Under this method, depreciation is not directly charged to the Asset Account. The depreciation for the period is debited to Depreciation Account and Credited to ‘Accumulated Depreciation Account’ or ‘Provision for depreciation Account.’

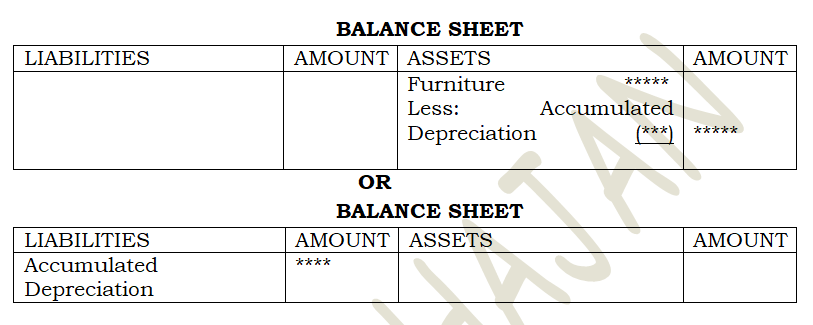

In the Balance sheet, asset appears at the original cost and the accumulated depreciation is shown as a deduction from the asset or shown at the liabilities side of the Balance Sheet.

Here, from the balance sheet, the original cost of the asset and the total depreciation to date that has been charged on that asset can be easily ascertained. As due year passes, the balance of the accumulated depreciation goes on increasing since constant credit is given to this account in each accounting year. After the expiry of the useful life or when asset is sold before the expiry of useful life, these accounts are closed by Debiting the Accumulated Depreciation Account and Crediting the Asset Account. Any balance in the Asset Account is transferred to the Profit and Loss Account.

JOURNAL ENTERIES

WHEN PROVISION FOR DEPRECIATION ACCOUNT IS NOT MAINTAINED:

Under this method, the depreciation is directly charged to the Assets Account. The value of assets is reduced by the amount of depreciation. Depreciation account is closed by transferring it to the Profit & Loss Account. In the Balance sheet, asset appears at its written down value i.e. Cost less depreciation charged to date.

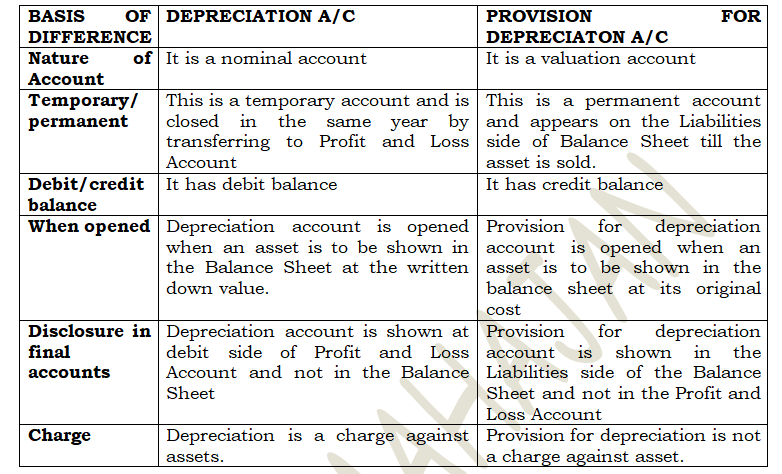

DIFFERENCE BETWEEN DEPRECIATION ACCOUNT AND PROVISION FOR DEPRECIATION ACCOUNT