MEANING

Balance Sheet is also known as Position Statement. It is a summary of all the assets and the liabilities of the business concern prepared at the end of the year. It is a part of final accounts. All the nominal accounts i.e. Trading Account and Profit and Loss Account are closed by transferring to the Balance Sheet.

ACCORDING TO ERIC L KOHLER

“A statement of financial position of any economic unit disclosing as at a given moment of time its assets, its liabilities and its ownership equities.”

ACCORDING TO FREEMAN

“A balance sheet is an item-wise list of assets, liabilities and proprietorship of a business at certain date.”

FEATURES OF BALANCE SHEET

NOT AN ACCOUNT, A STATEMENT

It is not an account, it is a statement. It is not prepared in account form and has no Debit or Credit side. All the assets are recorded on the right hand side and all the liabilities are recorded on the left hand side with no use of ‘BY’ and ‘TO’.

RECORDS ONLY ASSETS AND LIABILITIES

It makes a record of assets, liabilities and capital only. All the assets whether they are current or non-current are recorded on the right hand side and all the current or non-current liabilities are recorded on the left hand side.

TIME OF PREPARATION

It is prepared at the end of the financial year as at 31st March 20__. It makes it a static statement.

STAGE OF PREPARATION

It is prepared after the preparation of Trading Account and Profit and loss Account. The net profit or net loss found out of the profit or loss account is posted on the liabilities side under the head capital.

SHOWS FINANCIAL POSITION OF THE BUSINESS

It shows the financial position of the business. It depicts how much the business owes and business owns.

BASIS OF PREPARATION

Balance Sheet is prepared on the basis of accounting equation which is as follows:

ASSETS= LIABILITIES + CAPITAL

As per this equation, the both sides of the balance sheet must be equal.

MARSHALLING OF BALANCE SHEET

Marshalling means ‘Sequence’. Marshalling of Balance Sheet means the order in which the assets and liabilities will appear in the Balance Sheet. There are two main orders:

- IN THE ORDER OF PERMANENCE

- IN THE ORDER OF LIQUIDITY

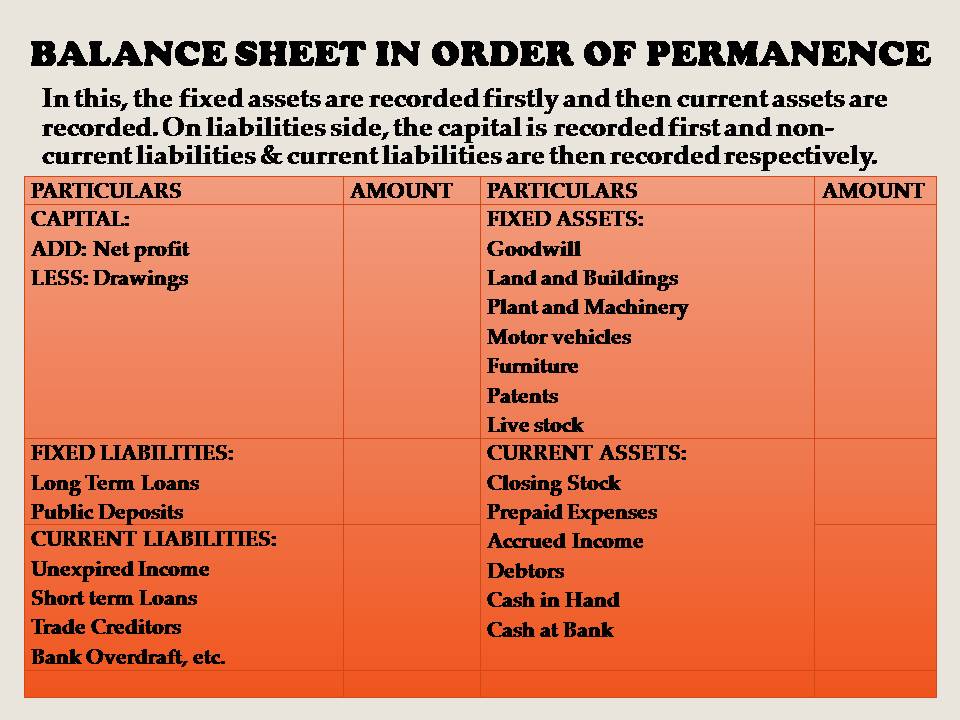

IN THE ORDER OF PERMANENCE

As per this order, the fixed assets are recorded firstly and then current assets are recorded. On the liabilities side, the capital is recorded first and non-current liabilities and current liabilities are then recorded respectively.

The format of Balance sheet in order of permanence is as follows:

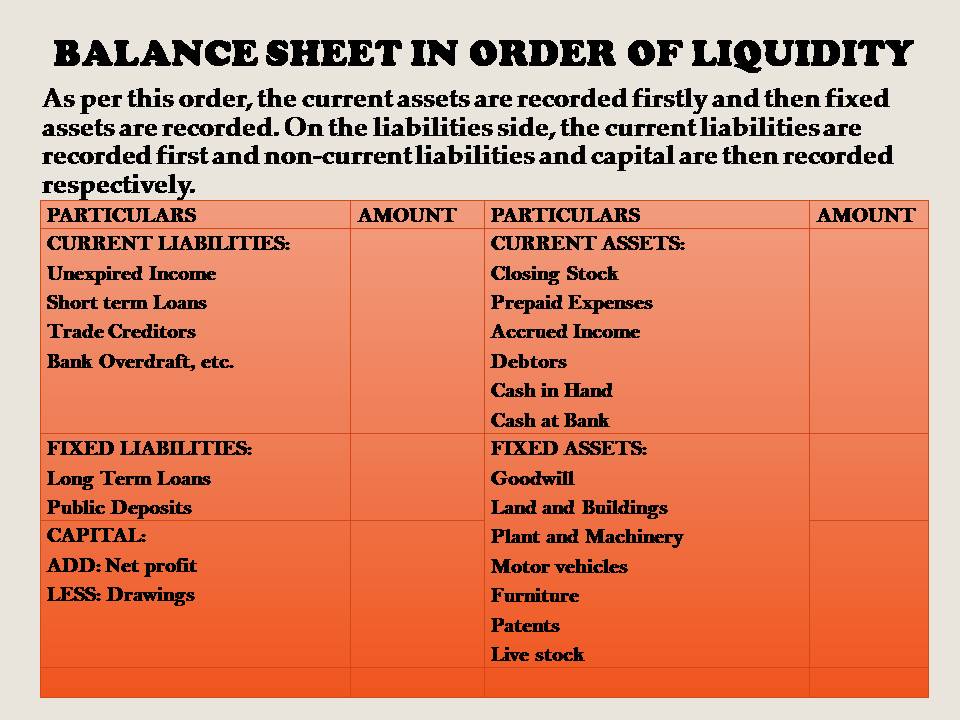

IN ORDER OF LIQUIDITY

As per this order, the current assets are recorded firstly and then fixed assets are recorded. On the liabilities side, the current liabilities are recorded first and non-current liabilities and capital are then recorded respectively.

The format of Balance sheet in order of liquidity is as follows: