MONOPOLY MEANING

In this post you will get notes on Monopoly Meaning, Features of Monopoly and price determination under monopoly.

The word Monopoly Meaning is the derivation from the combination of two words i.e., ‘Mono’ and ‘Poly’. Mono refers to a single and poly to control.

In this way, monopoly refers to a market situation in which there is only one seller of a commodity.

There are no close substitutes for the commodity it produces and there are barriers to entry. The single producer may be in the form of individual owner or a single partnership or a joint stock company. In other words, under monopoly there is no difference between firm and industry.

Monopolist has full control over the supply of commodity. Having control over the supply of the commodity he possesses the market power to set the price. Thus, as a single seller, monopolist may be a king without a crown. If there is to be monopoly, the cross elasticity of demand between the product of the monopolist and the product of any other seller must be very small.

ACCORDING TO BILAS

“Pure monopoly is represented by a market situation in which there is a single seller of a product for which there are no substitutes; this single seller is unaffected by and does not affect the prices and outputs of other products sold in the economy.”

ACCORDING TO KOUTSOYIANNIS

“Monopoly is a market situation in which there is a single seller. There are no close substitutes of the commodity it produces, there are barriers to entry”.

ACCORDING TO A J BRAFF

“Under pure monopoly there is a single seller in the market. The monopolist demand is market demand. The monopolist is a price-maker. Pure monopoly suggests no substitute situation”.

ACCORDING TO FERGUSON

“A pure monopoly exists when there is only one producer in the market. There are no other competitions.”

ACCORDING TO MC CONNEL

“Pure or absolute monopoly exists when a single firm is the sole producer for a product for which there are no close substitutes.”

FEATURES OF MONOPOLY

The features of monopoly are as follows:

One Seller and Large Number of Buyers

The monopolist’s firm is the only firm; it is an industry. But the number of buyers is assumed to be large.

No Close Substitutes

There shall not be any close substitutes for the product sold by the monopolist. The cross elasticity of demand between the product of the monopolist and others must be negligible or zero.

Difficulty of Entry of New Firms

There are either natural or artificial restrictions on the entry of firms into the industry, even when the firm is making abnormal profits.

Monopoly is also an Industry

Under monopoly there is only one firm which constitutes the industry. Difference between firm and industry comes to an end.

Price Maker

Under monopoly, monopolist has full control over the supply of the commodity. But due to large number of buyers, demand of any one buyer constitutes an infinitely small part of the total demand. Therefore, buyers have to pay the price fixed by the monopolist.

Nature of Demand and Revenue under Monopoly

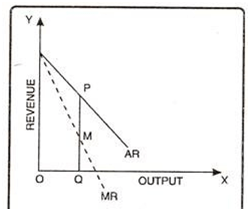

Under monopoly, it becomes essential to understand the nature of demand curve facing a monopolist. In a monopoly situation, there is no difference between firm and industry. Therefore, under monopoly, firm’s demand curve constitutes the industry’s demand curve. Since the demand curve of the consumer slopes downward from left to right, the monopolist faces a downward sloping demand curve. It means, if the monopolist reduces the price of the product, demand of that product will increase and vice- versa.

In the diagram above, Average revenue curve of the monopolist slopes downward from left to right. Marginal revenue (MR) also falls and slopes downward from left to right. MR curve is below AR curve showing that at OQ output, average revenue (= Price) is PQ where as marginal revenue is MQ. That way AR > MR or PQ > MQ.

PRICE AND OUTPUT DETERMINATION UNDER MONOPOLY: SHORT RUN

In the short run, a monopolist has to work with a given existing plant. He can expand or contract output by varying the amount of variable factors. He cannot adjust the size of plant in the short run.

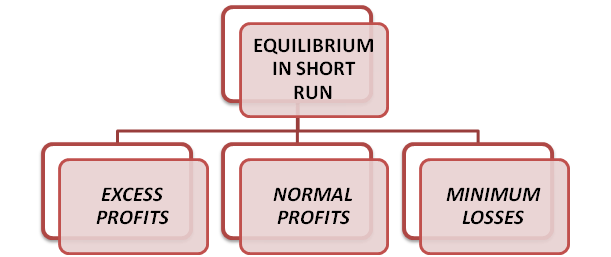

A monopolist in equilibrium may face three situations in the short run:

The process of price determination under monopoly has been explained as follows:

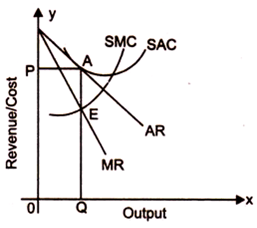

1. Super Normal Profit:

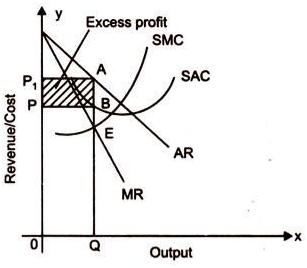

If the average revenue (AR) fixed by monopolist in equilibrium is more than the average cost (AC) than monopolist will earn excess profits.

The revenue and cost conditions faced by monopolist firm are presented in the following figure:

AR and MR are the average and marginal revenue curves of the firm, respectively. SAC and SMC are the short run average cost and marginal cost curves of the firm, respectively. To maximise profits, the monopolist firm chooses a price and output combination for which SMC = MR, and SMC curve cuts MR from below.

As shown in the Figure, E is the equilibrium where monopolist SMC curve cuts MR curve from below. A perpendicular parallel to y-axis is drawn at point E connecting the x-axis at Q and the demand curve at A. OQ is the equilibrium output. AQ is the equilibrium price, because the price is determined by demand curve or average revenue curve.

The average cost is BQ, because line AQ cuts SAC curve at point B. Thus, the monopolist’s per unit excess profit is AB, which is the difference between the price (AQ) and the corresponding average cost of production (BQ) The ABPP1 represent total monopolist’s profit. The total profit of the monopolist will be maximum only at OQ level of output.

2. Normal Profit:

In the short period, it is possible that monopolist may earn normal profit. This happens only when the average cost curve of the monopolist is tangent to its average revenue curve.

In following figure, the monopolist is the equilibrium at OQ level of output, because at this level of output his marginal cost curve (SMC) cuts MR curve at point E. Also at same level of output (OQ) the monopolist SAC curve touches his AR curve at point A. Thus AQ or OP is the monopolist price (which is determined by AR curve) is also equal to the cost per unit (AQ). The monopolist will earn only normal profit and the normal profit is included in the average cost of production.

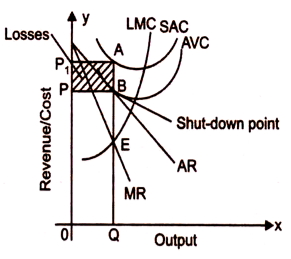

3. Loss Minimization in the Short Period:

In the short run, the monopolist may incur losses also. The monopolist may continue his production so long as price of his product is high enough to cover his average variable cost. If the price falls below average variable cost, the monopolist prefers to stop production. Accordingly, a monopolist in equilibrium, in the short run, may bear minimum losses equivalent to fixed costs. The situation of minimum losses has been illustrated in the following figure:

The monopolist is in equilibrium at point E, where SMC = MR and SMC curve cuts MR curve below. 0Q is the equilibrium level of output.

The price of equilibrium output 0Q is fixed at BQ or 0P.

At this price, average variable cost (AVC) curve AR curve at point B. It means firm will set at only average variable cost from the prevailing price. The firm will bear the loss of fixed cost equivalent to AB per unit. The firm will bear total loss equivalent to ABPP1. If its price falls below (BQ) the monopolist will prefer to stop the production. The point B is also known as ‘shut-down point’.

From the above analysis of short run price and output equilibrium it may be content that profit maximisation or loss minimisation or attainment of normal profit will be accomplished only at that level of output at which marginal cost is equal to marginal revenue and marginal cost cuts MR curve from below.

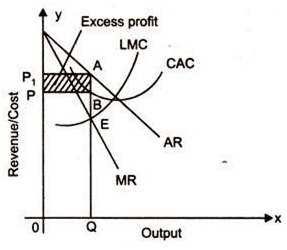

PRICE AND OUTPUT DETERMINATION UNDER LONG-RUN

In the long run, the monopolist has the time to expand its size of the plant, or to use his existing plant at any level which will maximize his profit. With entry blocked, however, it is not necessary for the monopolist to reach an optimal scale, what is certain is that the monopolist will not stay in business, if he makes losses in the long run.

However, the size of his plant and the degree of utilization of any given plant size depends entirely on the market demand. After these adjustments are completed, the monopoly rum will have a long run equilibrium determined by the equality of long run marginal cost and marginal revenue as shown in following figure:

E is the equilibrium point of the monopolist firm. Corresponding to this equilibrium point, 0Q is the equilibrium level of output. The monopoly will fix price AQ in the long run. Average cost is BQ. Profit per unit is AB. Total profit is equal to ABPP1.

It may be noted that there is always a tendency for the monopolist firm to secure excess profits, even in the long run, since entry into the industry is prohibited.