LEVY AND COLLECTION OF GST

Levy means import of the tax as well as the assessment of the tax. Assessment of the tax is done to ascertain the liability arising under the law. Collection of the tax is done as prescribed under the law.

Section 9 of CGST Act/SGST Act and Section 5 of IGST Act are the Charging Sections for the purpose of levy of GST. CGST and SGST shall be levied on all intra-state supplies of goods and/or services and IGST shall be levied on all inter-state supplies of goods and/or services respectively.

The levy and collection of different types of GST is as follows:

LEVY AND COLLECTION AS PER CGST ACT, 2017 (UNDER SECTION 9)

1. Levy of central goods and service tax [Section 9(1)]:

Under CGST Act, central tax called as the central goods and services tax (CGST) shall be levied on all intra-State supplies of goods or services or both, except on the supply of alcoholic liquor for human consumption.

It shall be levied on the value determined under section 15 and at such rates, not exceeding 20%, as may be notified by the Government on the recommendations of the Council and collected in such manner as may be prescribed and shall be paid by the taxable person.

2. Central tax on petroleum products to be levied from the date to be notified [Section 9(2)]:

The central tax on the supply of petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas and aviation turbine fuel shall be levied with effect from such date as may be notified by the Government on the recommendations of the Council.

3. Tax payable on reverse charge basis [Section 9(3)]:

The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both.

Further, all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

4. Tax payable on reverse charge if the supplies are made to a registered person by unregistered person [Section 9(4)]:

The central tax in respect of the supply of taxable goods or services or both by a supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

5. Tax payable on intra-State supplies by the electronic commerce operator on notified services [Section 9(5)]

As per section 2(45) of the CGST Act, 2017, “electronic commerce operator” means any person who owns, operates or manages digital or electronic facility or platform for electronic commerce.

Further, “electronic commerce” means the supply of goods or services or both, including digital products over digital or electronic network.

Thus, Electronic Commerce Operators (ECO), like flipkart, uber, makemy-trip, display products as well as services which are actually supplied by some other person to the consumer, on their electronic portal. The consumers buy such goods/services through these portals. On placing the order for a particular product/service, the actual supplier supplies the selected product/service to the consumer. The price/consideration for the product/service is collected by the ECO from the consumer and passed on to the actual supplier after the deduction of commission by the ECO.

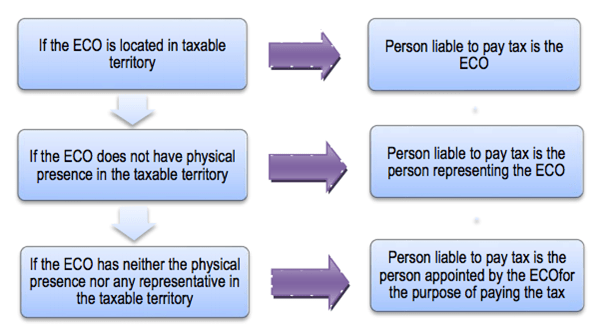

The Government may, on the recommendations of the Council, by notification, specify categories of services the tax on intra-State supplies of which shall be paid by the electronic commerce operator (ECO), if such services are supplied through it.

- Where an electronic commerce operator (ECO) does not have a physical presence in the taxable territory, any person representing such electronic commerce operator (ECO) for any purpose in the taxable territory shall be liable to pay tax.

- Where an electronic commerce operator (ECO) does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

LEVY AND COLLECTION AS PER IGST ACT, 2017 (UNDER SECTION 5)

U/s 5(1) of IGST Act, 2017

There shall be levied a tax Called the Integrated Goods and Services Tax (IGST)

- On all the

inter-state supplies of goods or services or both, except on supply of

alcoholic liquor for human consumption;

- On the value determined u/s 15 of CGST Act, 2017

- At such a rate (maximum 40%,) as notified by the Central Government on recommendation of GST Council

- Collected in such a manner as may be prescribed

- Shall be paid by the taxable person.

Provided further that IGST will be imposed on goods/ services imported into India.

U/s 5(2) of IGST Act, 2017

The CGST of following supply shall be levied with the effect from such date as notified by the Central Government on recommendation of GST Council

- Petroleum

crude

- high speed diesel

- Motor spirit (commonly known as petrol)

- Natural gas

- Aviation turbine fuel

U/s 5(3) of IGST Act, 2017

IGST is to be paid on reverse charge basis by the recipient on notified goods/ services or both. Reverse charge is the liability to pay tax by the recipient of supply of goods / services rather than supplier of goods/ services under forward charge).

U/s 5(4) of IGST Act, 2017

IGST on taxable inter-state supply of goods/ services to registered supplier from unregistered supplier (agriculturist) is to be paid on reverse charge basis by the recipient.

U/s 5(5) of IGST Act, 2017

E-Commerce operator is liable to pay CGST on notified inter-state supplies

LEVY AND COLLECTION OF GST UNDER UTGST ACT. (SECTION 7)

The provisions under section 7 of the UTGST Act are similar to section 9 of CGST Act except—

- The word CGST has been substituted by the word UTGST under the UTGST Act.

- Under UTGST Act, tax called UT tax is be levied on all intra-State supplies,

- Maximum rate 7(1) of UTGST Act is 20%.

LEVY AND COLLECTION OF CESS

Under GST (Compensation to States) Act, 2017

Section 8 of GST (Compensation to States) Act, 2017 forms the basis for levy and collection of cess which will be levied on for the purposes of providing compensation to the States for loss of revenue arising on account of implementation of the goods and services tax with effect from the date from which the provisions of the Central Goods and Services Tax Act were brought into force. The cess is levied on:

- such intra-State supplies of goods or services or both, as provided for in section 9 of the Central Goods and Services Tax Act, and

- such inter State supplies of goods or services or both as provided for in section 5 of the Integrated Goods and Services Tax Act

The same shall be collected in such manner as may be prescribed, on the recommendations of the Council, for a period of five years.

- However, no such cess shall be leviable on supplies made by a taxable person who has decided to opt for composition levy under section 10 of the Central Goods and Services Tax Act.

- The cess shall be levied on such supplies of goods and services as are specified in Schedule to the Act.

- Where the cess is chargeable on any supply of goods or services or both with reference to their value, for each such supply the value shall be determined under section 15 of the Central Goods and Services Tax Act for all intra-State and inter-State supplies of goods or services or both

- Cess on goods imported into India shall be levied and collected in accordance with the provisions of section 3 of the Customs Tariff Act, 1975, at the point when duties of customs are levied on the said goods under section 12 of the Customs Act, 1962, on a value determined under the Customs Tariff Act, 1975.

LEVY OF REVERSE CHARGE- TAX PAYABLE BY RECIPIENT OF SUPPLY OF GOODS OR SERVICES OR BOTH

CGST/UTGST/SGST/IGST shall be paid by the recipient of goods or services or both, on reverse charge basis, in the following cases:

- Supply of goods or services or both, notified by the Government on the recommendations of the GST Council.

- Supply of taxable goods or services or both by an unregistered supplier to a registered person

All the provisions of the relevant GST law shall apply to the recipient in the aforesaid cases as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN

https://www.linkedin.com/in/kajal-mahajan-7549b2197/