REVISED INVOICE IN GST

Under GST, all the taxable dealers will have to apply for provisional registration and carry out all the formalities post which they will get the permanent registration certificate.

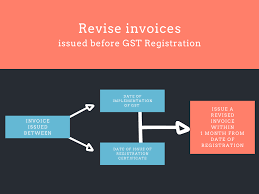

For all the invoices issued between the period –

- Date of implementation of GST

- Date of issue of Registration certificate

The dealers will have to issue a revised invoice against the invoice already issued between the said period. The revised invoice will have to be issued within one month from the date of issue of the registration certificate.

HOW TO REVISE A TAX INVOICE IN GST?

There may be a situation where an invoice has been wrongly issued, or there are certain changes that are required in an already issued invoice. Such situations call for a rectification of invoices. All such rectification has to be reported accordingly in the monthly returns.

Revision of tax invoices can take place in a number of ways. There can be a downward or an upward revision in prices of goods or services being supplied, or there can be a change the in the rate of tax of GST or many other cases.

These cases render a change in the issued invoice. An upward revision can be catered to with a supplementary invoice. Similarly, a downward revision can be catered to using a credit note to that effect. In some cases, there can be a complete revision in the invoice; hence, a “revised” invoice has to be issued.

All invoices raised between the date from which GST is applicable and the date on which they get the formal GST ID number, such taxable registered person shall be required to issue a “revised” invoice. This invoice shall be in adherence to the terms of GST and has to be issued within 1 month from the receipt of original registration certificate.

It is obvious from the above that a registered taxable person cannot issue a revised invoice after receipt of registration certificate.

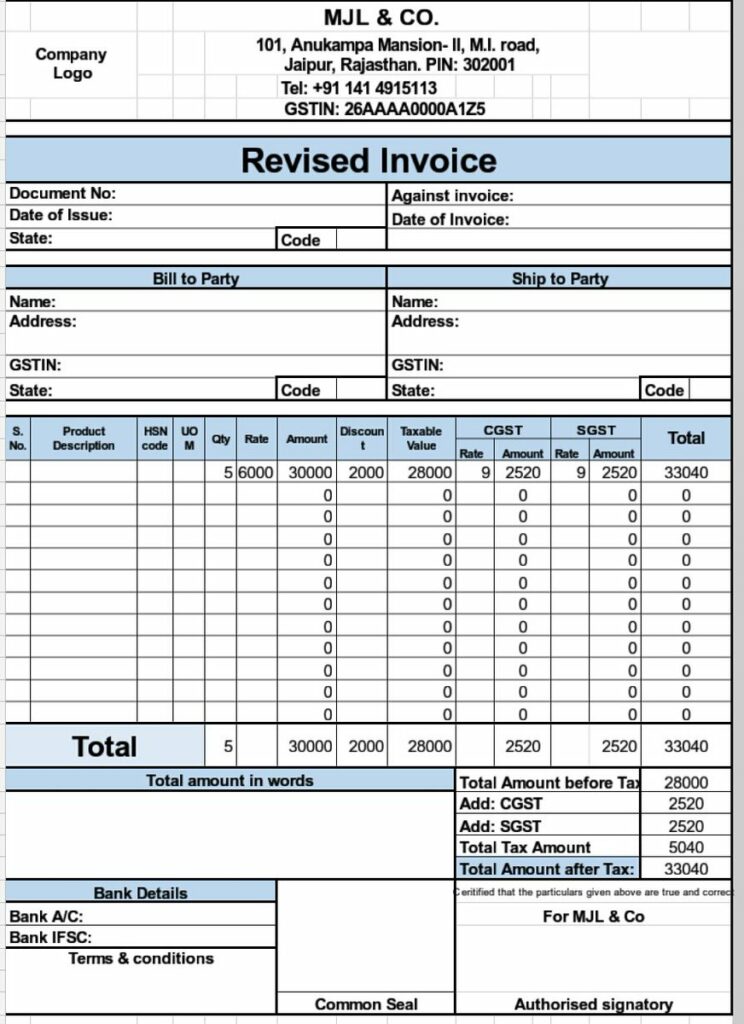

GST REVISED INVOICE FORMAT

All revised tax invoices under GST must contain the following particulars:

- The word “REVISED INVOICE”, indicated prominently on the invoice.

- Name, address and GSTIN of the Supplier;

- Nature of the document;

- Consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters -hyphen or dash and slash symbolized as “-” and “/” respectively, and any combination thereof, unique for a financial year;

- Date of issue of the invoice;

- Name, address and GSTIN or UIN, if registered, of the recipient;

- Name and address of the recipient and the address of delivery. The details shall also include the name of the State and its code. (for the un-registered recipient);

- Serial number and date of the corresponding tax invoice. It applies for a bill of supply;

- Value of taxable supply of goods or services, rate of tax, and the amount of the tax credited or. It applies if debited to the recipient;

- A signature, digital signature of the supplier, or authorized representatives.