MEANING

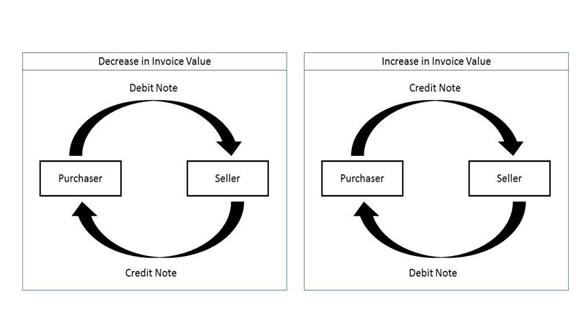

Credit Note is a document that is issued by a registered person under section 34(1) of CGST Act 2017 when supplies are returned or found deficient, or decrease in taxable value or GST charged in invoice. The tax liability of the supplier will reduce, as and when the Cr. Note is issued by the registered person.

Sometimes, the purchaser is unhappy with the quality of product shipped to him. In that case, he shall return the goods to the supplier, and in return, the supplier issues the purchaser, credit notes to the extent of the value of the goods being returned. There is no predefined format in which the credit note has to be issued; rather it is an intimation to the purchaser about such credit being offered.

ISSUANCE SECTION 34(1)

Where a Tax Invoice has been issued for supply of goods or services or both and;

- the value declared in the invoice is more than the actual value of the goods or services provided; or

- the rate of GST or Tax amount charged is at a higher rate than what is applicable for the kind of goods or services supplied; or

- the quantity received by the recipient is less than what is mentioned in the tax invoice; or

- the goods supplied are returned by the recipient;

then the registered person, who has supplied such goods or services or both, shall issue a Cr. Note to the recipient.

Once the Cr. Note is issued, the tax liability of the supplier will reduce.

TIME OF ISSUE OF CR. NOTE

Credit Note can be issued anytime that is there is no prescribed time limit for issuing them. Credit Notes that are issued should be declared in the returns of GST filed.

Credit Note is to be furnished in return for the month for which such note has been issued before:

- September following the end of the financial year in which such supply was made or

- the date of furnishing of Annual return

Whichever is earlier, and the liability of the tax should be adjusted in the manner prescribed.

FORMAT OF CREDIT NOTE

There is no prescribed format for Credit Note. However, it must contain prescribed Particulars same as a Revised Tax Invoice which includes the following:

- The word “Credit Note” indicated prominently

- Name, Address and GSTIN of the Supplier

- Nature of the document

- A consecutive serial number not exceeding 16 characters, containing alphabets or numbers or special characters, unique for a FY

- Date of issue of the document

- Name, address and GSTIN or UIN of the recipient (if registered)

- Name and address of the recipient, along with the address of delivery (if unregistered)

- Serial no. and date of the corresponding Tax Invoice

- Value of Taxable supply of goods or services, rate of tax and the amount of tax credited/debited to the recipient

- Signature/ Digital signature of the supplier or hiss authorized representative

DETAILS OF CR. NOTE TO BE FURNISHED IN RETURN: SECTION 34(2)

Any registered person who issues a credit note shall declare the details of such credit note in the return for the month during which such credit note has been issued but not later than

- September following the end of the financial year in which such supply was made; or

- the date of furnishing of Annual return,

whichever is earlier, and the tax liability shall be adjusted in prescribed manner.

OTHER PROVISIONS

- Credit note cannot be issued with GST on account of renegotiation of prices after supply if prices are reduced. In this case credit note can be issued without showing GST.

- This credit note will not be required to be filed with monthly return.

- Credit note for bad debts cannot be issued with GST.

- Credit note cannot be issued with GST in respect of B2C supply as the tax invoice does not have the GSTIN of the buyer.

CREDIT NOTE INCLUDES THE SUPPLEMENTARY INVOICE.

If credit note is issued it should be furnished in GSTR 1 for the month in which it is to be issued. The details will be auto populated in GSTR 2A of the recipient after which it is to be accepted by him or her and submit it in his or her GSTR 2.

A supplier will only be allowed to reduce the tax liability if the recipient accepts the credit note details in his GSTR 2.

ISSUE OF CR. NOTE IN CASE OF TIME EXPIRED GOODS

If the time expired goods are returned to the manufacturer or supplier, he or she can issue the credit note.

If such returned goods are destroyed by the manufacturer, he or she has to reverse the ITC attributable to the manufacture of such goods under section 17 (5)(h) of IGST Act.

REDUCTION IN TAX LIABILITY RELATED TO UNJUST ENRICHMENT

If cr. note is not accepted by the recipient and if he or she does not reverse the equivalent input tax credit, the supplier will not be allowed to the reduction of tax liability.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN