GOODS AND SERVICE TAX IN INDIA (GST)

Goods and Service Tax is a comprehensive tax levy on manufacture, sale and consumption of goods and service at a national level under which no distinction is made between goods and services for levying of tax. It will mostly substitute all indirect taxes levied on goods and services by the Central and State governments in India.

Goods and Service Tax is a tax on goods and services under which every person is liable to pay tax on his output and is entitled to get input tax credit (ITC) on the tax paid on its inputs(therefore a tax on value addition only) and ultimately the final consumer shall bear the tax.

In simple words, Goods and Service Tax (GST) is an indirect tax levied on the supply of goods and services. This law has replaced many indirect tax laws that previously existed in India.

Goods and Service Tax is one indirect tax for the entire country.

“Goods and Service Tax is a comprehensive, multi-stage, destination-based tax that is levied on every value addition.”

There are around 160 countries in the world that have GST in place. It is a destination based taxed where the tax is collected by the State where goods are consumed. India has implemented the GST from July 1, 2017 and it has adopted the Dual GST model in which both States and Central levies tax on Goods or Services or both.

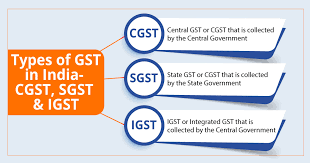

SGST – State Goods and Service Tax, collected by the State Govt.

CGST – Central Goods and Service Tax, collected by the Central Govt.

IGST – Integrated Goods and Service Tax, collected by the Central Govt.

HISTORY OF GOODS AND SERVICE TAX IN INDIA

The following is the brief history of Goods and service tax in India:

- 2000: In India, the idea of adopting Goods and Service Tax was first suggested by the Late Prime minister Atal Bihari Vajpayee Government in 2000. The state finance ministers formed an Empowered Committee (EC) to create a structure for GST, based on their experience in designing State VAT. Representatives from the Centre and states were requested to examine various aspects of the Goods and Service Tax proposal and create reports on the thresholds, exemptions, taxation of inter-state supplies, and taxation of services. The committee was headed by Asim Dasgupta, the finance minister of West Bengal. Dasgupta chaired the committee till 2011.

- 2004: A task force that was headed by Vijay L. Kelkar the advisor to the finance ministry, indicated that the existing tax structure had many issues that would be mitigated by the Goods and Service Tax system.

- February 2005: The finance minister, P. Chidambaram, said that the medium-to-long term goal of the government was to implement a uniform Goods and Service Tax structure across the country, covering the whole production-distribution chain. This was discussed in the budget session for the financial year 2005-06.

- February 2006: The finance minister set 1 April 2010 as the Goods and Service Tax introduction date.

- November 2006: Parthasarthy Shome, the advisor to P. Chidambaram, mentioned that states will have to prepare and make reforms for the upcoming Goods and Service Tax regime.

- February 2007: The 1 April 2010 deadline for Goods and Service Tax implementation was retained in the union budget for 2007-08.

- February 2008: At the union budget session for 2008-09, the finance minister confirmed that considerable progress was being made in the preparation of the roadmap for Goods and Service Tax. The targeted timeline for the implementation was confirmed to be 1 April 2010.

- July 2009: Pranab Mukherjee, the new finance minister of India, announced the basic skeleton of the GST system. The 1 April 2010 deadline was being followed then as well.

- November 2009: The EC that was headed by Asim Dasgupta put forth the First Discussion Paper (FDP) , describing the proposed Goods and Service Tax regime. The paper was expected to start a debate that would generate further inputs from stakeholders.

- February 2010: The government introduced the mission-mode project that laid the foundation for GST. This project, with a budgetary outlay of Rs.1,133 crore, computerised commercial taxes in states. Following this, the implementation of GST was pushed by one year.

- March 2011: The government led by the Congress party puts forth the Constitution (115th Amendment) Bill for the introduction of Goods and Service Tax. Following protest by the opposition party, the Bill was sent to a standing committee for a detailed examination.

- June 2012: The standing committee starts discussion on the Bill. Opposition parties raise concerns over the 279B clause that offers additional powers to the Centre over the Goods and Service Tax dispute authority.

- November 2012: P. Chidambaram and the finance ministers of states hold meetings and set the deadline for resolution of issues as 31 December 2012.

- February 2013: The finance minister, during the budget session, announces that the government will provide Rs.9,000 crore as compensation to states. He also appeals to the state finance ministers to work in association with the government for the implementation of the indirect tax reform.

- August 2013: The report created by the standing committee is submitted to the parliament. The panel approves the regulation with few amendments to the provisions for the tax structure and the mechanism of resolution.

- October 2013: The state of Gujarat opposes the Bill, as it would have to bear a loss of Rs.14,000 crore per annum, owing to the destination-based taxation rule.

- May 2014: The Constitution Amendment Bill lapses. This is the same year that Narendra Modi was voted into power at the Centre.

- December 2014: India’s new finance minister, Arun Jaitley, submits the Constitution (122nd Amendment) Bill, 2014 in the parliament. The opposition demanded that the Bill be sent for discussion to the standing committee.

- February 2015: Jaitley, in his budget speech, indicated that the government is looking to implement the GST system by 1 April 2016.

- May 2015: The Lok Sabha passes the Constitution Amendment Bill. Jaitley also announced that petroleum would be kept out of the ambit of Goods and Service Tax for the time being.

- August 2015: The Bill is not passed in the Rajya Sabha. Jaitley mentions that the disruption had no specific cause.

- March 2016: Jaitley says that he is in agreement with the Congress’s demand for the Goods and Service Tax rate not to be set above 18%. But he is not inclined to fix the rate at 18%. In the future if the Government, in an unforeseen emergency, is required to raise the tax rate, it would have to take the permission of the parliament. So, a fixed rate of tax is ruled out.

- June 2016: The Ministry of Finance releases the draft model law on Goods and Service Tax to the public, expecting suggestions and views.

- August 2016: The Congress-led opposition finally agrees to the Government’s proposal on the four broad amendments to the Bill. The Bill was passed in the Rajya Sabha.

- September 2016: The Honourable President of India gives his consent for the Constitution Amendment Bill to become an Act.

- 2017: Four Bills related to Goods and Service Tax become Act, following approval in the parliament and the President’s assent:

- Central Goods and Service Tax Bill

- Integrated Goods and Service Tax Bill

- Union Territory Goods and Service Tax Bill

- Goods and Service Tax (Compensation to States) Bill

The GST Council also finalized on the Goods and Service Tax rates and Goods and Service Tax rules. The Government declares that the Goods and Service Tax Bill will be applicable from 1 July 2017, following a short delay that is attributed to legal issues.

FEATURES OF GOODS AND SERVICE TAX IN INDIA

Goods and Service Tax belongs to the VAT family as tax revenues are collected on the basis of value added. Unlike in the case of a pure commodity based VAT system, Goods and Service Tax includes services tax also. Similarly, input credit is given while calculating the tax burden. Following are the main features of the Goods and service tax as per the final agreement.

TAXES COVERED

Most of the important indirect taxes of the centre and states are integrated under the Goods and service tax . The most important tax of the central government (in terms of tax revenue collection) -the Central Value Added Tax (or Union Excise Duty), Additional Customs Duty (CVD), Special Additional Duty of Customs (SAD), Central Sales Tax (levied by the Centre and collected by the States, the fastest growing tax revenue of the centre – Service Tax, the most important tax revenue of the states – the state VAT (Sales tax) are now merged into a single tax under the Goods and Service Tax.

There are three important indirect taxes for the centre – the union excise duties, service tax and customs duties. Of these, the central excise duties and service taxes are brought under the Goods and service tax . Customs duties as a tax on trade was not merged with the Goods and service tax .

States have two important indirect taxes – sales tax and state excise duties. Of these two, only the sales tax is merged with the Goods and Service Tax.

Along with these four big taxes of the centre and states, several other low revenue incurring taxes are also brought under the Goods and service tax .

A. The following taxes levied and collected by the Centre are merged with the Goods and Service Tax:

- Union Excise duties

- Services tax

- Duties of Excise (Medicinal and Toilet Preparations)

- Additional Duties of Excise (Textiles and Textile Products)

- Additional Duties of Excise (Goods of Special Importance)

- Additional Duties of Customs (commonly known as CVD)

- Special Additional Duty of Customs (SAD)

- Cesses and surcharges

B. State taxes that are subsumed under the Goods and service tax are:

- State VAT

- Central Sales Tax

- Entertainment Tax (not levied by the local bodies)

- Entry Tax (other than those in lieu of octroi)

- Luxury Tax

- Taxes on advertisements

- Taxes on lotteries, betting and gambling

- State cesses and surcharges insofar as they relate to supply of goods or services.

UNIFIED TAX REGIME

The Goods and Service Tax integrates into one unified tax regime. Previously, the goods and services were imposed and administered differently.

THE FOUR-TIER RATE STRUCTURE

The GST proposes a four-tier rate structure. The tax slabs are fixed at 5%, 12%, 18% and 28% besides the 0% tax on essentials. Gold is taxed at 3%. The centre has strictly demanded and got an additional cess on demerit luxury goods that comes under the high 28% tax. Essential commodities like food items are exempted from taxes under Goods and Service Tax. Other consumer goods which are common items will be taxed at 5%.4. The new Goods and Service Tax seems to have two standard rates – 12% and 18%. Goods and Service Tax rate structure for the goods and services are fixed by considering different factors including luxury/necessity nature.

SERVICE TAX RATE UNDER GOODS AND SERVICE TAX

Under the Goods and service tax , there is a differential tax structure. A low tax rate of 5% is imposed on essential services. Common services are charged at 12% and some commercial services at 18%. A tax rate of 28% on luxury services is also made. Several services like education provided by an educational institution, Post Offices, RBI etc. are exempted from service taxation. The standard Goods and service tax rate on services seems to be 18%. Services are taxed at a common rate of 15% previously.

TURNOVER LIMIT

Under Goods and Service Tax and tax right over low turnover entities: Goods and Service Tax is applied when turnover of the business exceeds Rs 20lakhs per year (Limit is Rs 10lakhs for the North-Eastern States). Traders who would like to get input tax credit should make a voluntary registration even if their sales are below Rs 20 lakh per year. Traders supplying goods to other states have to register under Goods and service tax , even if their sales are less than Rs 20 lakh. There is a composition scheme for selected group of tax payers whose turnover is up to Rs 75 lakhs a year.

TAX REVENUE APPROPRIATION BETWEEN THE CENTRE AND STATES

The centre and states will share Goods and Service Tax tax revenues at 50:50 ratio (except the IGST). This means that if a service is taxed at 18%, 9% will go to the centre and 9% will go to the concerned state.

COMPONENTS OF GST: CGST, SGST AND IGST

When the centre and states are merging their prominent indirect taxes under GST, both should get their own share in the Goods and Service Tax. For this, the Goods and Service Tax Council has adopted a dual Goods and Service Tax with two components – the Central Goods and Service Tax (CGST) and the State Goods and Service Tax (SGST).

Objective of this division is sharing the revenue from the unified Goods and service tax between the centre and states.

Central and State Goods and Service Tax

There is sharing of Goods and service tax by the centre and the tax accruing state at 50:50 ratio. For example, if a good is taxed at 18%, out of this, 9% will go to the centre and the remaining 9% will go to the state where the good is consumed. The GST going to the Centre is called as Central Goods and service tax (CGST) and that toes to the States is known as State GST (SGST). Here, the centre and the concerned state will equally share Goods and Service Tax on goods and services.

Basically, Goods and Service Tax is a destination based or consumption tax. Meaning of a destination based tax is that tax revenue (SGST) will go to the consuming state and not to the producing state.

In the case of intrastate production and consumption (production and consumption takes place in the same state), the share of SGST will accrue to the concerned state where as the share of CGST should be credited to the center’s account.

Integrated Goods and Service Tax (IGST)

The IGST comes to play when the commodity is produced in one state and is traded to another state (interstate trade). In this case, the share of SGST should go to the consuming state (as the Goods and service tax is a destination based tax). As a consumption based tax i.e the tax SGST share should be received by the state in which the goods or service are consumed and not by the state in which such goods are manufactured.

As per the GST law (Article 269 A), an Integrated Goods and Service Tax (IGST) would be levied and collected by the Centre on inter-State supply of goods and services. This tax will be collected by the Centre to ensure that the supply chain or interstate trade is not disrupted.

COMPOSITION SCHEME UNDER Goods and Service Tax

The composition levy is an alternative method of levy of tax designed for small taxpayers with turnover is up to Rs. 75 lakhs. The scheme can be availed by manufacturers and restaurants. Other service providers can’t opt for the scheme. It enables taxpayers to make payments at a flat rate under GST, without input credits. An alternate upper limit of Rs. 50 lakhs is applicable in a few states – Assam, Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, Sikkim and Himachal Pradesh.

The objective of the optional Composition Scheme is to bring simplicity and to reduce the compliance cost for the small taxpayers. Eligible persons opting to pay tax under this scheme can pay tax at a prescribed percentage of the turnover every quarter, instead of paying tax at normal rate. The GST rate under the composition scheme is 1% for manufacturer, 2.5% for restaurant sector and 0.5% for other suppliers of turnover. There will not be any input tax credit under the scheme. Instead of filing 3-4 returns monthly, taxpayers registered under this scheme will be required to file returns once every quarter.

In the service sector, Composition Scheme is available only for one sector – restaurants. The Composition Scheme is not available for manufacturers of tobacco and manufactured tobacco substitutes, pan-masala and ice-cream and other edible ice, whether or not containing cocoa.

Exports are exempted from GST as in the case of the previous regime. Administrative coordination between the centre and states, improvement of the tax administration machinery, awareness to the tax payers and the launch of the IT interface of GSTN are some of the preparatory efforts made by the government. Several benefits like creation of a unified tax regime in the country for indirect taxes, better centre state coordination and elimination of reducing tax on tax or cost cascading effect of tax are the positive outcome of the GST regime. Similarly, the system may raise compliance (revealing of taxable activity and paying taxes) among assessees.

RIGHT TO TAX ON TERRITORIAL WATERS

Right to impose tax on economic activities that are done on territorial waters: Here, the both centre and states have decided that states can impose and collect tax on those falls within 12 nautical miles.

ADVANTAGES OF GOODS AND SERVICE TAX IN INDIA

The Goods and Services Tax was introduced with the primary objective of boosting India’s economy. Besides simplifying the indirect taxation system, Goods and service tax has helped in clearing away the hidden costs on commodities/services, thus benefitting the end users. Some major advantages of the GST in India are as follows:

EASIER CLASSIFICATION

The GST system has facilitated in creating a transparent system with easier classification of products & services. However, the taxation under GST is based upon the concept of supply rather than on this classification. That is, if a transaction does not fall under the realm of supply, it will not be taxable under GST. Moreover, litigation, arising from cases whether a particular item or activity is goods or service, is not likely to occur.

BETTER COMPLIANCES

The implementation of the GST system has paved way for simpler procedures and compliances as well as aided in easy monitoring and tracking of defaults or non-compliances. Furthermore, there had been multiple legal compliances under different legislatures. But now, taxpayers have got things easier as legal norms only under one statue need to be adhered to. GST is supported by the Goods and Service Tax Network (GSTN), a fully integrated tax platform, to help manage all aspects of GST.

BENEFITS FOR SME’S AND START-UPS

SMEs and start-ups in India have a host of benefits awaiting them under the GST system which includes:

- Ease of starting business by lower compliances. Companies that have business in different states & territories were earlier required to comply with multiple laws. However, the centralised registration under GST has eased the process of setting up new businesses while also reducing the costs.

- Minimised tax burden on new businesses. Earlier, it was mandatory for companies with turnover more than Rs 5 lakhs to register themselves under VAT. However, the limit under GST has now been extended to Rs 20 lakhs. This has provided relief to over 60 percent of the SMEs.

- Efficient logistics leading to efficiency in delivery & cost savings. The entry tax for goods manufactured and sold in any part of India has been done away with under GST. Thus, it has paved way for smother transportation of goods by minimising waiting time on check posts. A direct result of this would be significant savings on transportation costs.

- Uniformity in the taxation process. Through a simple online mechanism, small businesses find it extremely easy to file their tax returns every quarter.

PRODUCT COMPETITIVENESS

Becoming at par with the international tax standards, the introduction of the GST system has ensured reduction in overall costs of production, thereby making Indian products much more competitive in the global market. Furthermore, inflation is likely to remain under control under the GST regime.

BENEFIT TO THE GOVERNMENT

The GST system has ensured better revenue generation for the government as the cost of tax collection has reduced. And, the government is seeing an increase in taxpayer registration. Also, with the systematic rules under GST, malpractices like corruption and sales without receipts are kept under check.

MITIGATION OF

CASCADING EFFECT

Under the GST administration, the final tax would be paid by the consumer for

the goods and services purchased. However, there would be an input tax credit

structure in place to ensure that there is no slumping of taxes. GST is levied

only on the value of the good or service.

ABOLITION OF

MULTIPLE LAYERS OF TAXATION

One of the advantages of GST is that it integrated different tax lines such as

Central Excise, Service Tax, Sales Tax, Luxury Tax, Special Additional Duty of

Customs, etc. into one consolidated tax. It prevents multiple tax layers

imposed on goods and services.

RESOURCEFUL

ADMINISTRATION BY GOVERNMENT

Previously, the management of indirect taxes was a complicated task for the

Government. However, under the GST establishment, the integrated tax rate,

simple input of tax credit mechanism and a merged GST Network, where

information is available, and administration of resources are well-organised

and straightforward for the Government.

ENHANCED PRODUCTIVITY OF LOGISTICS

The restriction on inter statement movement of goods has reduced. Earlier logistic companies had to maintain multiple warehouses across the country to avoid state entry taxed on interstate movements.

CREATION OF A COMMON NATIONAL MARKET

GST gave a boost to India’s tax to Gross Domestic Product ratio that aids in promoting economic efficiency and sustainable long – term growth. It led to a uniform tax law among different sectors concerning indirect taxes. It facilitates in eliminating economic distortion and forms a common national market.

EASE OF DOING BUSINESS

With the implementation of GST, the difficulties in indirect tax compliance have been reduced. Earlier companies faced significant problems concerning registration of VAT, excise customs, dealing with tax authorities, etc. The benefits of GST has aided companies to carry out their business with ease.

REGULATION OF THE UNORGANIZED SECTOR UNDER GST

It has created provisions to bring unregulated and Unorganised sectors such as the textile and construction industries to name a few under regulation with continuous accountability.

REDUCTION OF LITIGATION

GST aids in reducing litigation as it establishes clarity towards the jurisdiction of taxation between the Central and State Governments.GST provides a smooth assessment of tax.

TACKLING CORRUPTION AND TAX LEAKAGES

With the GST online network portal, the taxpayer can directly register, file returns and make payments of the taxes without having to interact with tax authorities. A mechanism has been devised to match the invoices of the supplier and buyer. This will not only keep a check on tax frauds and evasion but also bring in more businesses into the formal economy.

DISADVANTAGES OF GOODS AND SERVICE TAX IN INDIA

There are various benefits of GST in India. However, a tax reform of such magnitude comes with its teething problems.

IT INFRASTRUCTURE

Since GST is an IT-driven law, it cannot be sure whether all the states in India are currently equipped with infrastructure and workforce availability to embrace this law. Only a few states have implemented this E- Governance model. Even today some states use the manual VAT returns system.

HIGHER TAX BURDEN OF SME’S

Earlier the small and medium enterprises had to pay excise duty only on a turnover that exceeded Rs. 1.5 crore every financial year. However, under the Goods and service tax administration, businesses whose turnover exceeds Rs 40 lacs are liable to pay GST.

INCREASE BURDEN OF COMPLIANCE

The Goods and service tax administration states that companies are required to register in all the states they operate in. This increases the burden on the business for excessive paperwork and compliance.

PETROLEUM PRODUCTS DON’T FALL UNDER THE GST SLAB

Petrol and petroleum products have not been included in the scope of Goods and service tax until now. States levy their taxes on this sector. Tax credit for inputs will not be available to these industries or those related industries.

COACHING OF TAX OFFICERS

There is inadequate training that is provided to the Government officers for practical usage and implementation of such systems since the GST administration heavily banks on information technology.

INCREASED IMPLEMENTATION COST

The overall process of ensuring GST compliance and tax filing has led to an increase in the implementation cost for the businesses. This cost refers to the expenditure or investment in resources like computers, accounting (GST), software or training initiatives for GST experts. Moreover, the overall cost of doing business mounted in the initial few months of GST implementation.

RISE IN OPERATIONAL COSTS

GST has transformed the way in which taxes are paid. Moreover, to achieve compliances, businesses are required to depend on services by professional GST consultants. This has led to an additional cost for smaller businesses for hiring GST consultants leading to operational costs.

Implementation of GST has led to shortage of available funds. Traders have been facing issues in claiming tax refunds or transitional refund owing to complicated procedures.

ADVERSE IMPACT ON SOME INDUSTRIES

Some tax experts believe the GST system could have negative effects as certain products have become costlier. For instance, GST would add up to as much as 8 percent to the cost of new homes and minimise the demand by about 12 percent. Similarly, the tax levied on some retail products at present is only four percent tax. However with GST, garments and clothes are likely to get expensive.

Similarly, service sector like banks also feel the pinch. The banking industry is instrumental in the process of export of services or goods. Before the GST regime, a service tax @ 14% was levied on the banking transactions. However after the GST implementation, the rate has increased to 18%, thereby increasing the transaction costs, especially in those imports or exports with huge transactions.

CONCLUSION

GST in India was a sweeping reform and benefits of Goods and service tax and has changed the way businesses are conducted. Businesses are being included in the formal economy through Goods and service tax implementation. GST and its benefits have provided long term returns for the Indian economy on a large scale which have been welcomed as a new change by all the stakeholders.