GST RETURNS

GST RETURN MEANING

GST Return is a document containing details of income which a taxpayer is required to file with the tax administrative authorities. This is used by tax authorities to calculate tax liability.

Under GST, a registered dealer has to file GST returns that include:

- Purchases

- Sales

- Output GST (On sales)

- Input tax credit (GST paid on purchases)

GST RETURN FILING – WHO SHOULD FILE GST RETURN?

All business owners and dealers who have registered under the GST system must file GST returns according to the nature of their business or transactions. In the GST regime, any regular business has to file two monthly returns and one annual return. This amounts to 26 returns in a year.

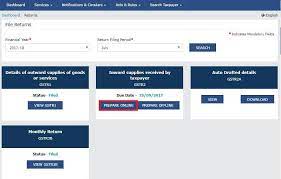

FILING GST RETURNS – HOW TO FILE GST RETURNS ONLINE?

From manufacturers and suppliers to dealers and consumers, all taxpayers have to file their tax returns with the GST department every year. Under the new GST regime, filing tax returns has become automated. GST returns can be filed online using the software or apps provided by Goods and Service Tax Network (GSTN) which will auto-populate the details on each GSTR forms. Listed below are the steps for filing GST returns online:

- Visit the GST portal (www.gst.gov.in).

- A 15-digit GST identification number will be issued based on your state code and PAN number.

- Upload invoices on the GST portal or the software. An invoice reference number will be issued against each invoice.

- After uploading invoices, outward return, inward return, and cumulative monthly return have to be filed online. If there are any errors, you have the option to correct it and refile the returns.

- File the outward supply returns in GSTR-1 form through the information section at the GST Common Portal (GSTN) on or before 10th of the following month.

- Details of outward supplies furnished by the supplier will be made available in GSTR-2A to the recipient.

- Recipient has to verify, validate, and modify the details of outward supplies, and also file details of credit or debit notes.

- Recipient has to furnish the details of inward supplies of taxable goods and services in GSTR-2 form.

- The supplier can either accept or reject the modifications of the details of inward supplies made available by the recipient in GSTR-1A.

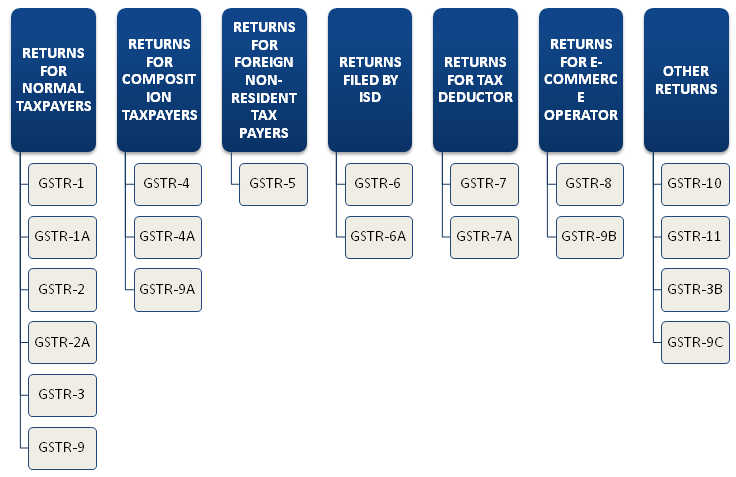

TYPES OF GST RETURNS

There are various types of returns to be filed by the tax payers under GST. All are as follows:

GST RETURNS TO BE FILED BY NORMAL TAXPAYERS

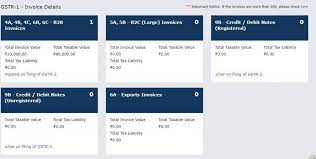

GSTR 1: Return for Outward Supplies

GSTR 1 is a monthly return of outward supplies undertaken by a normal registered taxpayer under GST. In other words, this monthly return showcases the sales transactions of a business in a particular month.

Who Needs To File GSTR 1?

Every normal registered taxpayer under GST is required to file GSTR 1 each month. This return showcases details of

- invoices,

- debit notes,

- credit notes and

- revised invoices issued pertaining to your outward supplies.

Due Date for Filing GSTR 1

The standard date for filing GSTR 1 is 10 days from the end of the month for which such a return is to be filed. However, the due date to file GSTR 1 can be extended for any class of persons beyond the tenth of the succeeding month by the Commissioner. The reasons for such an extension would be notified.

GSTR 1 is a detailed form containing 13 different heads. The critical headings are:

- GSTIN of the Taxable Person

- Name

- Gross Turnover in Last Financial Year

- The Period for which the return is being filed

- Taxable outward supplies

- Debit Notes or Credit Notes Details

- Export Sales

- Tax Liability arising out of advance receipts

- Tax Paid

GSTR 2A : Read Only Document

GSTR 2A is a read only document. This document gets auto-populated once the supplier uploads the details in GSTR 1. In other words, GSTR 2A enables the recipient to verify the details uploaded by the supplier in GSTR 1. Also the recipient could accept, reject, modify or keep the invoices pending using the said details. However, such changes are made by the recipient in GSTR 2.

Who Needs To File GSTR 2A?

GSTR-2A is made available to every normal registered taxpayer filing return under GST. This is because it is a read only document that gets auto-populated with details uploaded by supplier in GSTR-1.

Due Date for Filing GSTR 2A

GSTR 2A is a read-only document used by the recipient to match the details uploaded by the supplier in GSTR-1. Thus, the recipient can accept, reject, modify or keep the invoices pending in case there is any mismatch. However, the recipient can make actual changes, if any, only in Form GSTR 2. This process of making changes and filing GSTR-2 is to be undertaken between 11th and 15th day of the month succeeding the month for which such a return is to be filed.

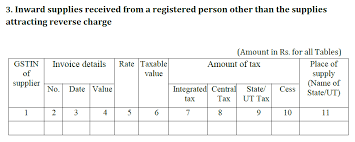

GSTR – 2: Return for Inward Supplies

GSTR-2 is a monthly return of inward supply of goods and services as agreed by the recipient of the goods and services. In other words, GSTR-2 contains details with regards to the purchases made by the recipient in a particular month. The information contained in GSTR-2 is auto-populated with the details contained in GSTR-2A.

Who Needs To File GSTR-2?

Every normal registered taxpayer under GST is required to provide details regarding inward supplies or purchases made for each month in GSTR-2. This return showcases details with regards to purchases made from registered and unregistered taxable persons, debit notes and credit notes issued with respect to the inward purchases etc.

Hence, the recipient makes use of the details auto-populated in Form GSTR-2A with details uploaded by supplier in GSTR-1. The recipient makes necessary changes if required in GSTR-2 after verifying the information auto-populated in GSTR-2A.

Due Date for Filing GSTR-2

The process of making changes and filing GSTR-2 is required to be undertaken .

GSTR-2 shall include the following heads:

- GSTIN of the Taxable Person

- Name

- The Period for which the return is being

- Details of all inward supplies

- Changes to the inward supplies made for any previous period

- Import of Goods

- Import of Goods in earlier periods

- Services received from a person outside India (Import of Services)

- Import of Services in earlier periods

- Debit notes or Credit notes Details

- Amendments made to Debit or Credit notes of previous periods

- Inward supplies emanating from Unregistered persons

- Credits received from an Input Service Distributor

- TDS credit from specified persons

- TCS credit from E-Commerce operators

- Input Tax Credit remaining to be taken against an invoice, from which initially a partial invoice was taken

- Reverse Charge tax liability

- Amendment to such reverse charge tax liability

- Tax Paid

- Input Tax Credit Reversals – A dropdown containing reasons for such reversals shall be made available

- Amendments to such Input Tax Credit Reversals

GSTR-1A

The form shall be auto-populated after filing of GSTR-2 on the 15th of the next month, having all the correct or changed information. The supplier shall have the choice to accept or reject the changes made by the recipient. Following such acceptance, the GSTR-1 shall be revised to such extent.

GSTR-3

This form is auto prepared by 20th of the next month. It will have the details of all outward as well as inward supplies of goods and services as furnished in GSTR-1 and GSTR-2. After considering both the details, GSTN will determine your input tax credit availability or the amount of tax payable.

It will have the following details:

- GSTIN of the Taxable Person – Auto-populated result

- Name – Auto-populated result

- Address of the person – Auto-populated result

- The Period for which the return is being filed – Month & Year shall be available as a drop-down for selection

- Total turnover

- Export Turnover

- Taxable Turnover

- Non-GST Turnover

- Nil Rated or Exempted Turnover

- Total Turnover (Sum of 1-4)

- Details of outward supplies

- Inter-state supply to end customers

- Intra-state supply to end customers

- Inter-state supply to registered persons

- Intra-state supply to registered persons

- Exports

- Amendments to Sales Invoices, Debit Notes and Credit Notes

- Tax liability on such outward supplies

- Details of inward supplies

- Inter-State received

- Intra-State received

- Imports

- Amendments to Purchase invoices, Debit Notes and Credit Notes

- Tax liability on such inward supplies

- Reversals of Input Tax Credit

- Total tax liability for the period

- TDS received for the period

- TCS received for the period

- ITC for the period

Apart from the above details, a Part B has to be filed containing the details of,

- Any taxes, interests, penalties or fees paid during the period

- Any refunds claimed during the period with respect to cash ledger.

GSTR-9: Annual Return For Normal Registered Taxpayer Under GST

Section 44(1) requires that:

Every registered person shall furnish electronically an annual return for every financial year in the prescribed form, except the following:

- Input Service Distributor

- Person paying tax under section 51 or section 52,

- Casual taxable person

- Non-resident taxable person

Furthermore, persons registered under GST but having no transactions during the year are still required to file a Nil Annual Return.

Due Date for Filing GSTR-9

Such a return needs to be furnished on or before the 31st day of December following the end of such financial year. To further add to this, Rule 80(1) of the CGST Rules, 2017 states that such registered person shall furnish an annual return electronically in Form GSTR-9. This return needs to be filed through the common portal either directly or through a Facilitation Centre notified by the Commissioner.

RETURNS TO BE FILED BY COMPOSITION TAX PAYERS

GSTR-4A

Similar to the GSTR-2A above, GSTR-4A is generated quarterly for composition scheme taxpayers. It has the details of the inward supplies as reported by suppliers in GSTR-1.

GSTR-4: Return For Composition Dealers

GSTR-4 is a quarterly return that needs to be filed by a registered taxpayer who has signed up for the Composition Scheme. Under this scheme, small taxpayers having a turnover of upto Rs 1.5 Crores need to pay tax at a fixed rate and file quarterly return. This is unlike the normal registered dealer who files three returns every month including GSTR-1, GSTR-2 and GSTR-3B.

Who Needs To File GSTR-4?

The Composition Scheme was introduced under GST in order to reduce the compliance burden on small taxpayers. Every registered taxpayer opting for Composition Scheme is required to file quarterly return in GSTR-4.

Due Date for Filing GSTR-4

The due date for filing GSTR-4 is 18th of every month following the quarter for which such a return needs to be filed. Say for instance, Kapoor Pvt Ltd is a composition dealer who needs to file his GST return for the quarter January – March 2019.

GSTR-9A: Annual Return For Composition Dealers

GSTR 9A is the annual return that every registered person opting for composition levy needs to file every financial year. This return is in addition to the quarterly returns filed by a composition dealer during a financial year. Thus, GSTR 9A is an annual return filed by a composition dealer containing details that relate to the quarterly returns filed by him during the year. This return contains details with regards to supplies made by the taxpayer during the year under composition scheme. These details include:

- Inward and outward supplies,

- Tax paid,

- Input credit availed or reversed,

- Tax refunds,

- Late fee etc

Due Date for Filing GSTR-9A

The due date to file GSTR 9A is on or before December 31 succeeding the close of a particular financial year for which the return needs to be filed.

RETURNS TO BE FILED BY FOREIGN NON-RESIDENT TAXPAYER

GSTR – 5: Return For Non-Resident Taxable Persons

GSTR-5 is a monthly return filed by every non-resident taxable person. This return includes details pertaining to:

- Inward supplies

- Outward supplies

- Any interest, penalty, fees

- Tax payable or tax paid or

- Any other amount payable under the act

Furthermore, this is the only return to be filed by a non-resident taxable person. This means, a non-resident taxable person is not required to file any annual return.

Who Needs To File GSTR-5?

Unlike a normal registered taxpayer, a non-resident taxable person is required to File monthly return in For GSTR-5. A non-resident taxable person means a person who supplies goods or services occasionally. This person does not have a fixed place of business or residence in India. Moreover, he can supply goods or services either as a principal or an agent or in any other capacity.

Due Date for Filing GSTR-5

The details in GSTR 5 need to be filed within a time period that is earlier of:

- Within 20 days after the end of the calendar month or within

- 7 days after the last date of validity of the registration

RETURNS TO BE FILED BY AN INPUT SERVICE DISTRIBUTOR

GSTR-6A

GSTR 6A is an auto drafted, read only form. This form is generated automatically based on the details furnished by the suppliers of an ISD in form GSTR 1. This form contains details pertaining to the supplies against which credit is received for distribution. It also includes the details pertaining to the debit notes and credit notes received during the current tax period. This form will be generated by 11th of next month after the suppliers have filed their GSTR-1 on 10th of the next month.

GSTR – 6: Return For Input Service Distributors

GSTR 6 is a monthly return that an Input Service Distributor files every calendar month. This return provides information of all the invoices on which credit has been received and are issued by an ISD. This means that it gives a summary of the total input tax credit available for distribution during a particular month. Thus, the details of the invoices that an ISD furnishes in form GSTR 6 are made available to every recipient of the credit. These details are visible to the recipient in part B of form GSTR 2A.

Due Date for Filing GSTR-6

GSTR-6 needs to be filed on the thirteenth day of the month succeeding the month for which tax is to be paid. Say for instance, Kapoor Pvt Ltd is registered as an ISD in Mumbai having branches in Mumbai, Hyderabad, Bangalore and Gurgaon. Kapoor Pvt Ltd needs to file ISD return for the month November 2018. Hence, the last date to file GSTR 6 for Kapoor Pvt Ltd is December 13, 2018.

RETURNS TO BE FILED BY A TAX DEDUCTOR

GSTR – 7: Return For Taxpayers Deducting TDS

GSTR 7 is a monthly return that is required to be filed by the deductors who are required to deduct TDS under GST. Such a return consists of the details regarding:

- Tax deducted at source,

- The liability towards tds,

- Tds refund claimed if any

- Interest, late fees etc. Paid or payable

Due Date for Filing GSTR-7

GSTR-7 is required to be filed by the deductor within 10 days after the end of the month in which the deduction was made. For example, the due date for filing GSTR-7 for the month of June 2018 would be 10th July, 2018.

GSTR-7A

GSTR-7A is an auto-generated form. The form gets generated once the deductor furnishes details in Form GSTR-7 on the common portal. If the details furnished by the deductor are accepted by the deductee, then a TDS certificate is made available to the deductee electronically.

RETURN TO BE FILED BY AN E-COMMERCE PORTAL

GSTR-8: Return For E-Commerce Operators Collecting TCS

GSTR 8 is a monthly return furnished by every electronic commerce operator who is required to deduct Tax Collected at Source under GST. This return reflects details of the supplies made through e-commerce portal and the amount of tax collected from suppliers of goods and services. Furthermore, the operator can also make changes to the details of supplies furnished in any of the earlier period statements.

Due Date for Filing GSTR-8

The last date to file GSTR 8 is the 10th day of the month succeeding the month for which TCS is to be collected. Thus, the amount of tax that the operator collects also needs to be deposited by the 10th day of the following month during which such a collection is made. Furthermore, the operator is also required to file an annual statement in the prescribed format in GSTR 9B. This return needs to be filed by 31st December following the end of each financial year.

GSTR – 9B: Annual Return For E-Commerce Operators Collecting TCS

Every electronic commerce operator required to collect tax at source under section 52 shall furnish annual statement in FORM GSTR -9B. This return includes all the information furnished by the e-commerce operators in the monthly returns filed during the financial year.

Due Date for Filing GSTR-9B

All the e-commerce taxpayers are required to file GSTR-9B on or before 31st December following the close of the financial year.

OTHER RETURNS

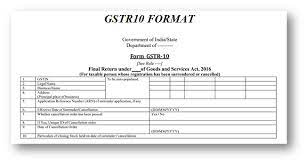

GSTR – 10: Return For Registered Person Whose GST Registration Gets Cancelled

GSTR-10 is a final return required to be filed by a registered person whose GST Registration gets cancelled. Such a registered person does not include:

- Input Service Distributor

- Person paying tax under composition scheme

- Non-resident taxable person

- Person collecting TDS or TCS

Further, Form GSTR-10 is filed electronically through the common portal either directly or via a facilitation centre as prescribed by the Commissioner. The intent of filing this final return is to make sure that the taxpayer pays of any liability outstanding. This liability may include an amount equivalent to the amount that is higher of:

- Input tax related to stock of finished and semi-finished goods, capital goods or plant and machinery or

- Output tax payable on such goods

Due Date for Filing GSTR-10

The registered person whose GST Registration has been cancelled is required to file final return in Form GSTR-10 within a period which is later of:

- 3 months from the date of cancellation or

- Date of order of cancellation

GSTR – 11: Return For UIN (Unique Identification Number) Holders

GSTR-11 is a return to be furnished by a person who has been allotted a Unique Identification Number (UIN). UIN is issued so that the registered person obtaining the same can claim refunds for GST paid on goods and services purchased by them in India.

Who Can Apply For UIN?

UIN is allotted to foreign embassies and diplomatic missions who are not required to pay taxes in India. This number is issued so that these organizations can claim a refund for the amount of tax paid to the Indian Tax Authorities. In order to claim the refund on GST paid, these organizations need to file GSTR-11.

The organizations that can apply for UIN include:

- Specialized agency of the United Nations Organization

- A consulate or embassy of foreign countries

- Multilateral financial institution and organization notified under the United Nations (Privileges and Immunities) Act, 1947

- Any other person or class of persons as may be specified by the Commissioner

Due Date for Filing GSTR-11

The due date for filing GSTR-11 is 28th of the month succeeding the month in which inward supplies are received by the UIN holders. This means, GSTR-11 is not filed on a monthly basis. Rather, this form is filed on case-to-case basis as and when the supplies are made.

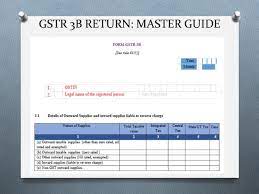

GSTR – 3B: Summary of Inward and Outward Supplies

GSTR 3B is a simplified monthly summary return of inward and outward supplies. It is a self declaration showcasing the summary of GST liabilities of the taxpayer for the tax period in question. Moreover, it helps the taxpayer to discharge the tax liabilities in a timely manner.

GSTR-3B is a form that cannot be revised. Furthermore, this form does not require the compliance of comparing invoices between supplier and purchaser. That means both the suppliers and the recipients file the GSTR-3B form separately. Therefore, such a facility does not cause delays in filing of returns which would consequently attract late fees and interest.

Who Needs To File GSTR-3B?

Every normal registered taxpayer filing GST Returns is required to file GSTR-3B. GSTR-3B is also filed during the tax periods for which the tax liability is zero. That is, a taxpayer needs to file a Nil Return in case there are no outward or inward transactions during a particular month.

Due Date for Filing GSTR-3B

The GSTR-3B must be submitted by the 20th of the month succeeding the tax period for which GST is filed. In case no transactions have been undertaken in a particular month, the registered person needs to file a NIL return for that period.

GSTR – 9C: Return For Registered Persons Getting Accounts Audited From CA

Every registered person having an aggregate turnover of more than Rs. 2 crores during a financial year must get his accounts audited by a CA or cost account. Furthermore, he needs to submit the annual return, a copy of the audited accounts and a reconciliation statement. This reconciliation statement is in Form GSTR 9C. So basically, GSTR 9C is a reconciliation statement reconciling value of supplies declared in annual return with the audited annual accounts.

Due Date for Filing GSTR-9C

The due date for filing GSTR-9C is the same as that for filing annual returns in GSTR-9. Hence, GSTR-9C shall be submitted on or before 31st December of the year subsequent to the relevant FY under audit. For instance, the due date for filing GSTR-9C for the FY 2017-2018 shall be 31st December 2018.

LATE FILING OF GST RETURNS

Return filing is mandatory under GST. Even if there is no transaction, you must file a Nil return.

- You cannot file a return if you do not file

previous month/quarter’s return.

- Hence, late filing of GST return will have a cascading effect leading to heavy fines and penalty.

- The late filing fee of the GSTR-1 is populated in the liability ledger of GSTR-3B filed immediately after such delay.

INTEREST/LATE FEES TO BE PAID

- Interest is 18% per annum. It has to be calculated by the taxpayer on the amount of outstanding tax to be paid. It shall be calculated on the Net tax liability identified in the ledger at the time of payment. The time period will be from the next day of filing due date till the actual date of payment.

- As per GST Act Late fee is Rs. 100 per day per Act. So it is 100 under CGST & 100 under SGST. Total will be Rs. 200/day. The maximum is Rs. 5,000. There is no late fee on IGST.

QUESTIONS COVERED

What do you mean by GST Return? What types of returns are specified under GST Regime? Discuss in brief.

What is GSTR? Discuss in brief various types of GSTRs specified under GST Regime.