EXEMPTIONS UNDER GST

Exemption refers to the release or privileged freedom from some duty or tax. GST also provides exemptions to some parties regarding the registration. There are some people who are exempted from the GST Registration based on what is the nature of their supply.

The taxpayers who are exempted from GST Registration are:

- Agriculturists.

- Persons falling in Threshold Exemption Limit.

- Persons making Nil-Rated/ Exempt supplies of goods and services.

- Persons making Non-Taxable/ Non-GST supplies of goods and services.

- Activities that are neither Supply of Goods nor Services.

- Persons making only supplies covered under reverse charge.

The details of all the parties exempted are as follows:

AGRICULTURISTS

An agriculturist is a person who supplies the products out of his cultivation land. They will be given exemptions from GST Registration. Agro-inputs like fertilizers, seeds, irrigation (electricity is required), machinery and all other agricultural services are also exempted under GST regime.

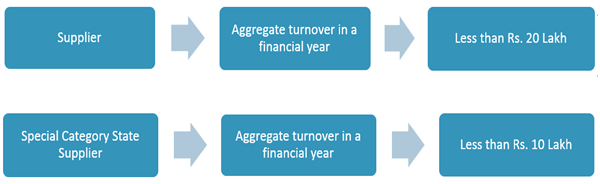

PERSONS FALLING IN THRESHOLD EXEMPTIONS LIMIT

A business entity with an annual turnover less than Rs. 20 lakh is given exemptions from GST registration. But there are some special category states (Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand) where this threshold limit is Rs. 10 lakh.

PERSONS MAKING NIL-RATED/ EXEMPT SUPPLIES

These are the persons who are engaged in the business of supplying common items which are in the exemptions list of GST. Some of them are mentioned below:

- All unprocessed food like rice, wheat, bread, milk, vegetables, cereals, eggs, meat, fish, salt etc.

- Train travel by local and sleeper classes

- Education

- Healthcare (but not medicines)

- Hotels, lodges with room rent less than Rs 1,000

- Kid’s colouring /drawing books

- Bindis, sindoor, bangles, etc

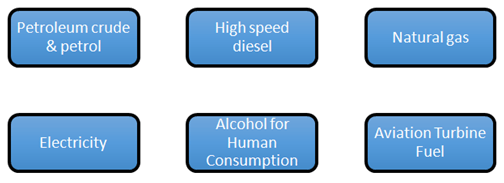

PERSONS MAKING NON-TAXABLE/ NON-GST SUPPLIES

Such items do not come under the purview or scope of GST:

ACTIVITIES THAT ARE NEITHER SUPPLY OF GOODS NOR SERVICES

These include:

- Services by an employee.

- Services by any Court or Tribunal.

- Functions and duties of –

- MPs, MLAs, Members of Panchayats, Municipalities and other local authorities;

- Person holding any Constitutional Post;

- Person as a Chairperson or a Member or a Director in a body.

- Funeral Services.

- Sale of land and building.

- Actionable claims (other than lottery, betting, and gambling).

PERSONS MAKING ONLY SUPPLIES COVERED UNDER REVERSE CHARGE

The Central Government has on 19th June 2016 via Notification No. 5/2017 exempted such persons from obtaining registration who are only engaged in making supplies of taxable goods or services, the total tax on which is liable to be paid on reverse charge basis by the recipient of such goods or services. This notification shall come into force on 22nd June 2016.

QUESTION COVERED

Do you agree that exemptions are given to Goods and Services from GST under the Act? If yes, then state the area of exemption in brief.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN

https://www.linkedin.com/in/kajal-mahajan-7549b2197/