HOW TO CLAIM TCS IN GST

Tax Collected at Source (TCS) under GST means the tax collected by an e-commerce operator from the consideration received by it on behalf of the supplier of goods, or services who makes supplies through operator’s online platform. TCS will be charged as a percentage on the net taxable supplies.

TCS credit received is a facility available after logging in to the GST portal. It can be filed by all the taxpayers who are making specified sales on the e-commerce platforms and/or entered into any kind of works contract with Government departments. The form is mostly similar to GSTR-2A as it auto-populates details from GST returns like GSTR-7 and GSTR-8 together.

Any GST portal user can click on ‘TCS credit received’ tile available on return dashboard after logging in. This can help them to claim or reject the credit of TCS deducted or collected by their corresponding e-commerce operator.

PROVISIONS OF TCS

Section 52 of the CGST Act, 2017 has specified the provision for collection of tax at source. Tax Collection at Source (TCS) has similarities with TDS, as well as a few distinctive features. TDS refers to the tax which is deducted when the recipient of goods or services makes some payments under a contract etc. while TCS refers to the tax which is collected by the electronic commerce operator when a supplier supplies some goods or services through its portal and the payment for that supply is collected by the electronic commerce operator.

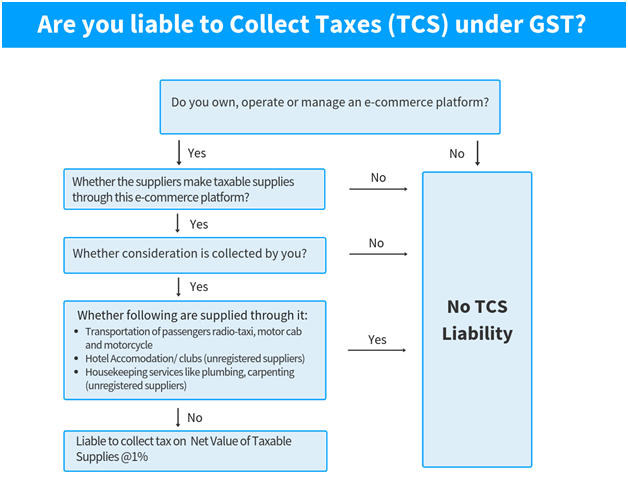

Section 2 (45) of the CGST Act, defines “Electronic Commerce Operator’ means any person who owns, operates or manages digital or electronic facility or platform for electronic commerce.

Section 2(44) of the CGST Act, defines ‘Electronic Commerce’ means the supply of goods or services or both, including digital products over digital or electronic network.

PROCEDURE OF COLLECTION OF TCS

The goods or services belonging to other suppliers are displayed on the portals of the operators and consumers buy such goods/services through these portals. On placing the order for a particular product/service, the actual supplier supplies the selected product/service to the consumer. The price/consideration for the product/ service is collected by the operator from the consumer and passed on to the actual supplier after the deduction of commission by the operator. Every electronic commerce operator, not being an agent, shall collect an amount calculated at the rate of 1% of the net value of taxable supplies made through it where the consideration with respect to such supplies is to be collected by the operator and pay to the Government.

Net value has to be ascertained in terms of a formula as provided under sub-section (1) of Section 52 of the Act.

Net Value of Taxable Supplies = [(Aggregate Value of Taxable Supplies of Goods + Services) – (Section 9(5) Services)]} – (Aggregate Value of Returned Taxable Supplies + Goods)]

Example: Suppose a certain product is sold at Rs. 1000/- through an Operator by a seller. The Operator would deduct tax @ 1% of the net value of Rs. 1000/- i.e. Rs. 10/-.

The said amount will be calculated on the net value of the goods/services supplied through the portal of the operator. For the purposes of considering the “net value of taxable supplies” shall mean the aggregate value of taxable supplies of goods or services, other than services notified under sub-section (4) of section 8 of the CGST Act, made during any month by all registered taxable persons through the operator reduced by the aggregate value of taxable supplies returned to the suppliers during the said month.

REGISTRATION

The e-commerce operator as well as the supplier supplying goods or services through an operator needs to compulsorily register under The threshold limit of Rs. 20 lakhs (Rs. 10 lakhs for special category states) is not applicable to them. Section 24(x) of the CGST Act, 2017 makes it mandatory for every e-commerce operator to get registered under GST. Similarly, section 24(ix) of the CGST Act, 2017 makes it mandatory for every person who supplies goods/services through an operator to get registered under GST.

POWER TO COLLECT TAX

Section 52 (2) of the CGST Act, empowered electronic commerce operator to collect the amount shall be without prejudice to any other mode of recovery from the operator.

Certain operators who own, operate and manage e-commerce platforms are liable to collect TCS. TCS applies only if the operators collect the consideration from the customers on behalf of vendors or suppliers. In other words, when the e-commerce operators pay the consideration collected to the vendors they have to deduct an amount as TCS and pay the net amount.

Here are few exceptions to the TCS provisions for the services provided by an e-commerce platform:

a. Hotel accommodation/clubs (unregistered suppliers)

b. Transportation of passengers – radio taxi, motor cab or motorcycle

c. Housekeeping services like plumbing, carpentry etc. (unregistered suppliers)

TIME PERIOD FOR TCS TAX PAYMENT

Sub-section (3) of Section 52 of the Act provides that Tax Collected at Source shall be paid to the Government within 10 days after the end of the month of collection.

MANNER OF PAYMENT

Any amount Collects as TCS shall be paid by debiting the e-cash ledger and electronic liability register shall be credited accordingly.

MONTHLY STATEMENT

The every operator who collects the amount of tax shall furnish a statement, electronically, containing all the details relating to:

a. Outward supplies of Goods and Services.

b. Returned of goods and services.

c. Amount collected during a month.

In Form GSTR-8 within 10 days from the end of the month in terms of sub-rule (1) of Rule 67 of the rules read with sub-section (4) of Section 52 of the CGST Act.

ANNUAL STATEMENT

The every electronic commerce operator who collects tax at source shall furnish an annual Statement, electronically, containing all the details relating to:

a. Outward supplies of Goods and Services,

b. Returned of goods and services during the Financial Year,

c. Amount collected during a financial year.

In Form GSTR-9B by 31’st December following the end of such Financial Year in terms of sub-section (5) of section 52 of the CGST Act, and read with sub-rule (2) of Rule 80 of the CGST Rules.

ERROR IN MONTHLY STATEMENT

If any e.commerce operator who collects the amount under section 52(1) of the Act, after furnishing a statement found any errors or omissions or incorrect particulars therein, other than as a result of scrutiny, audit, inspection or enforcement activity by the tax authorities then he shall rectify the same in the statement of month of such discovery, subject to Payment of interest under sub-section (6) of Section 52 of the Act.

Provided that no rectification will be allowed:-

After the due date of furnishing the statement for the month of September following the end of Financial Year, or Actual date of Furnishing the Annual Statement, whichever is earlier.

CLAIM OF INPUT CREDIT

Supplier of goods and services can claim the amount of credit in their e-Cash Ledger as collected and reflected by the e.commerce Operator in Statement under sub-section (7) of Section 52 of the Act.

MATCHING OF SUPPLIES

The Supplies shall match with the corresponding outward supplies of the registered Supplier as the details furnished by the e-commerce operator in Form GSTR-8 shall be made available electronically to each of the suppliers in Part C of Form GSTR -2A on the Common Portal after the due date of filing of Form GSTR-8 in terms of Rule (2) of Rule 67 read with sub-section (8) of Section 52 of the Act.

DISCREPANCY OF SUPPLIES

When the Supplies under sub-section (4) do not match with the corresponding supplies of the supplier then, such discrepancy shall be communicated to both the persons in terms of sub-section (9) of Section 52 of the Act.

PAYMENT OF DIFFERENTIAL AMOUNT

The amount in respect of which any discrepancy in the value of such supplies, the same would be communicated to both of the under sub-section (9) of Section 52 of the Act. If such discrepancy in value is not rectified within the given time, then such amount would be added to the output tax liability of such suppler. The supplier will have to pay the differential amount of output tax along with interest in terms of sub-section (10) & sub-section (11) of section 52 of the Act.

NOTICE TO THE ELECTRONIC COMMERCE OPERATOR

An officer not below the rank of Deputy Commissioner can issue Notice to supplied through electronic commerce operator during any period, stock of goods lying in warehouses/ godowns etc., managed by such operator and declared as additional places of business by such supplies.

REPLY TO NOTICE

The electronic commerce operator is required to furnish such details within 15 working days of serve of such notice under sub-section (13) of Section 52 of the Act.

RECOVERY PROCEEDING

In case an electronic commerce operator fails to furnish the information required by the notice, besides being liable for penal action under section 122 of the Act, states that any person committing the offences as stated under the section, shall be liable to pay a penalty of ten thousand rupees or an amount equivalent to the tax evaded or the tax not deducted under section 51 or short deducted or deducted but not paid to the Government or tax not collected under section 52 or short collected or collected but not paid to the Government or input tax credit availed of or passed on or distributed irregularly, or the refund claimed fraudulently, whichever is higher, it shall also be liable for penalty up to Rs. 25,000/-.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN