MEANING

Debit Note is a document issued by a supplier under Section 34(3)of CGST Act, 2017, when there is a need of increase in taxable value or increase in GST charged in invoice.

The tax liability of the supplier will increase, as and when the Dr. Note is issued by the supplier.

It is to be noted that a debit note can be issued by a recipient also when the goods are returned or damaged in transit. But under GST, only supplier can issue the Dr. note.

ISSUANCE SECTION 34(3)

The person who supplies the goods shall issue a debit note in the following cases:

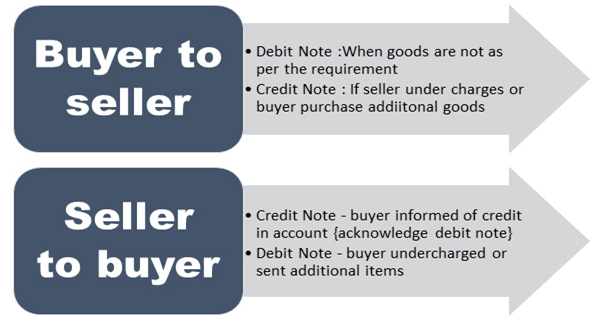

- When the value of invoice is less than the actual value of goods or services.

- When the taxable amount or GST charged is at a lower rate than what is applicable for such goods or services.

Value of invoice increases due to extra goods/services are delivered or incorrect amount( taxable value/tax) is entered in the invoice. In this case, the supplier will issue this note. As in the books of the supplier, customer account has the debit balance and on accounting of debit note, customer account balance be will increase. The customer gives credit note to the supplier on receipt on the debit note. The credit note will increase the liability in the books of the customer, as he has pay an extra amount to settle the liability.

IT INCLUDES THE SUPPLEMENTARY INVOICE

If debit note is issued it should be furnished in GSTR 1 for the month in which it is to be issued. The details will be auto posted in GSTR 2A of the recipient after which it is to be accepted by him or her and submit it in his or her GSTR 2.

For a corresponding response of the Dr. note on the tax liability the recipient must accept it in his or her Form GSTR 2.

CONTENTS

The following things are to be maintained in the Dr. note, for proper update and reporting. Although there is no predefined format for the same, necessary care has to be taken to mention these important details in the debit notes.

Rule 53 states that the debit note shall contain the following particulars:

- The word “Debit Note”, to be indicated

prominently

- Supplier’s name, address, and GSTIN

- Nature of the document

- The consecutive serial number which is a

unique number for every financial year

- Date of issue of the document

- Name, address and GSTIN or UIN, if

registered, of the recipient

- Name and address of the recipient and the

address of delivery, along with the name of State and its code, if such

recipient is unregistered

- Serial number and date of the corresponding

tax invoice or, as the case may be, bill of supply

- Value of taxable supply of goods or services,

the rate of tax and the amount of the tax credited or debited to the recipient

and

- Signature or digital signature of the supplier or his authorized representative

The details of debit notes have to be declared in the month following the month on which such debit note has been raised. Debit notes can be issued anytime without any time limit.

DETAILS OF DEBIT NOTE TO BE FURNISHED IN RETURN: SECTION 34(4)

Any registered person who issues a debit note shall declare the details of such debit note in the return for the month during which such debit note has been issued and the tax liability shall be adjusted in prescribed manner.

RECIPIENT CAN ISSUE Dr. NOTE WITHOUT GST

As per the act the issue of debit or credit note can only be done by the supplier. Both the notes can be issued with GST for increasing or decreasing the liability of GST of the supplier.

If in any case the recipient does not accept the value that is shown in the invoice of the supplier. The supplier do not issue credit note, the recipient has only option to issue Dr. note without GST otherwise his purchases will be inflated.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN