The difference between Debit note and Credit note is as follows:

DEBIT NOTE IN GST

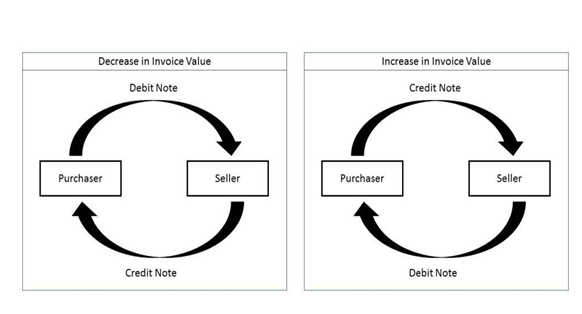

Debit note is a document issued by a supplier under Section 34(3)of CGST Act, 2017, when there is a need of increase in taxable value or increase in GST charged in invoice.

The tax liability of the supplier will increase, as and when the Debit Note is issued by the supplier.

It is to be noted that a debit note can be issued by a recipient also when the goods are returned or damaged in transit. But under GST, only supplier can issue the debit note.

CREDIT NOTE

Credit notes is a document that is issued by a registered person under section 34(1) of CGST Act 2017 when supplies are returned or found deficient, or decrease in taxable value or GST charged in invoice. The tax liability of the supplier will reduce, as and when the Credit Note is issued by the registered person.

Sometimes, the purchaser is unhappy with the quality of product shipped to him. In that case, he shall return the goods to the supplier, and in return, the supplier issues the purchaser, a credit note to the extent of the value of the goods being returned. There is no predefined format in which the credit note has to be issued; rather it is an intimation to the purchaser about such credit being offered.

DIFFERENCE BETWEEN DEBIT NOTE AND CREDIT NOTE

| BASIS OF DIFFERENCE | Debit Note | Credit Note |

| PREPARED BY | It is sent when a buyer returns goods to the seller | It is given when a supplier receives returned goods from the buyer |

| NATURE OF AMOUNT | This shows a positive amount | This shows a negative amount |

| JOURNAL ENTRIES | Journal Entries Sales Returns A/C – Debit To Debtor’s A/C – Credit | Journal Entries Creditor’s A/C – Debit To Goods Returned A/C – Credit |

| TIME LIMIT | No time limit is there for issuing debit note. | There is time limit for issuing credit note. |

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN