INSTALMENT PAYMENT SYSTEM

An instalment payment system is a credit sale system in which payments are made in instalments over a period of time. In this system, the buyer gets the possession of the goods as well as the ownership of the goods right at the time of signing the agreement.

During the course of paying the instalment, the vendor cannot responses to the goods. In that case, the vendor can sue the buyer only for the recovery of dues.

FEATURES OF INSTALMENT PAYMENT SYSTEM

- Instalment purchase system is just like an outright credit sale of goods.

- The buyer makes the payment in different instalment over a periods of time as agrees upon in the agreement.

- Under instalment system, the buyer gets the immediate possession as well as the ownership of the goods.

- The seller cannot claim the good back if the buyer made default in the payment of instalment.

- In case of default in the payment of instalment, the total amount of instalments already paid by the buyer cannot be forfeited.

- Under this system, the buyer can sell or mortgage the goods as the ownership is with the buyer.

- Risk of the goods/ assets are to borne by the buyer just after signing the agreement.

- The buyer of the goods under this system has no right to return the goods to the seller.

ACCOUNTING TREATMENT

The accounting treatment in the books of the buyer and seller is as follows:

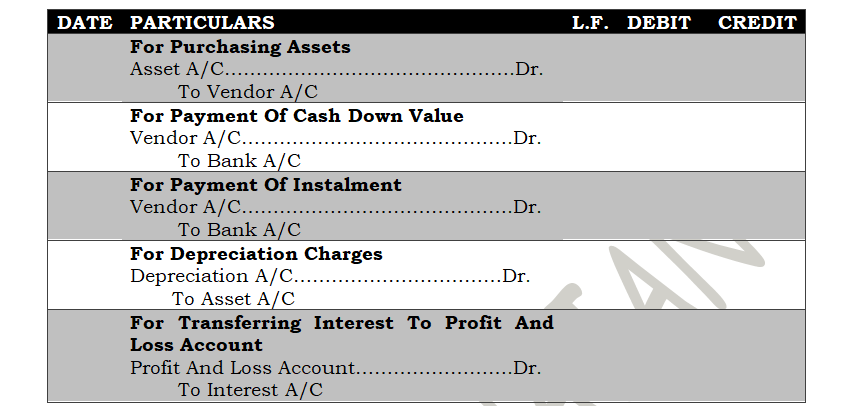

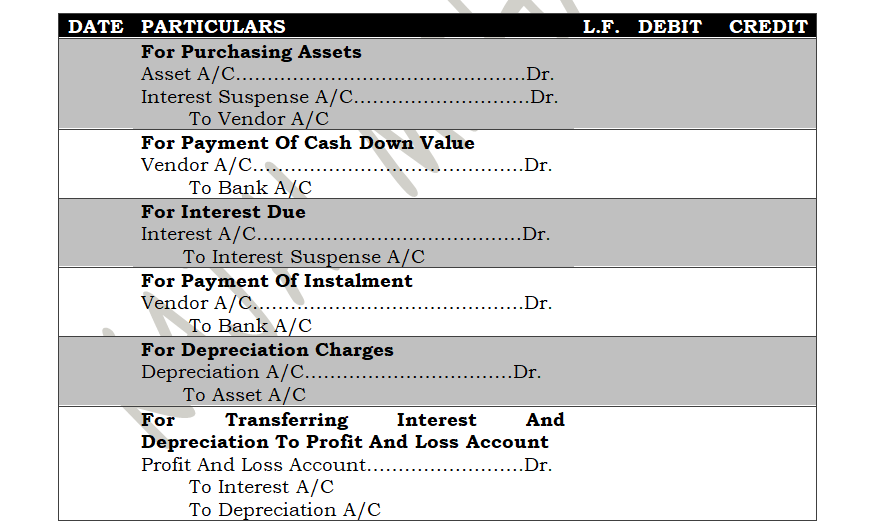

IN THE BOOKS OF THE BUYER

There are two methods of recording transactions:

WITHOUT OPENING INTEREST SUSPENSE ACCOUNT

BY OPENING INTEREST SUSPENSE ACCOUNT

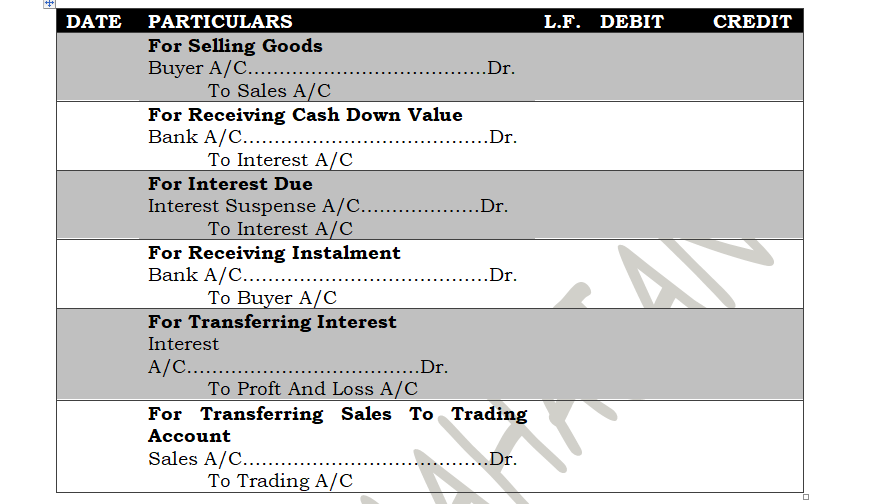

IN THE BOOKS OF THE VENDOR

Here again entries are recorded by two methods:

WITHOUT OPENING INTEREST SUSPENSE ACCOUNT

| For selling goods: Buyer A/c Dr. To Sales A/c |

| For receipt of down payment: Cash/ Bank A/c Dr. To Buyer A/c |

| For instalment received: Cash/ Bank A/c Dr. To Buyer A/c |

| For transfer of sales to trading account Sales A/c Dr. To Trading A/c |

| For transfer of interest to Profit and Loss Account Interest A/c Dr. To Profit and Loss A/c |

WITH OPENING INTEREST SUSPENSE ACCOUNT

ADVANTAGES OF INSTALMENT PAYMENT SYSTEM

- This system enables the buyers to buy the goods which are beyond their reach.

- It widens the market

- Middlemen are eliminated

- As convenience and luxury goods are sold, the standard of living increases.

- Sellers can increases their sales by adopting this method.

DISADVANTAGES

- This system tempt the buyers to buy the goods beyond their reach. So this is extravagant.

- The buyer pays higher price for the article as interest charge is usually more.

- There are many legal formalities which are quiet cumbersome.