Final Accounts of Sole trader covers the topic of Preparation of Profit and loss account and Balance sheet.

QUESTION: Explain the Income statement under Sole Trader Concept.

Income statement of sole trader consists the preparation of Trading account and Profit and Loss account. Income statement shows how much the sole trader has earned the profit or has suffered the loss. Income statement of sole trader is prepared as follows:

TRADING ACCOUNT

Trading Account is one of the financial statements prepared by the trading firms at the end of the year. These are prepared to find out the gross profit or gross loss accruing to the firm. This account records all the amounts related to the goods purchased and sold. It helps in providing all the material facts regarding the stock sold or remain unsold.

ACCORDING TO JR BATLIBOI

“The Trading Account shows the result of buying and selling of goods. In preparing this account, the general establishment charges are ignored and only the transactions in goods included.

FEATURES

The features of this account are as follows:

NATURE OF ACCOUNT: It is a Nominal Account. It records all the expenses on purchases on the debit side and income in the nature of the sales on credit side. The rule applies to this account is:

“DEBIT ALL EXPENSES AND LOSSES

CREDIT ALL INCOMES AND GAINS”

TIME OF PREPARATION:It is prepared at the end of the year i.e. as at 31st March, 20__. It is prepared at first before preparing Profit and Loss Account and Balance Sheet.

RESULT: This Account shows the result of Gross Profit or Gross Loss by comparing the both sides Debit and Credit. Increase of debit over credit results in Gross Loss and increase of credit over debit results in Gross Profit.

Debit< Credit= Gross Profit

Debit> Credit= Gross Loss

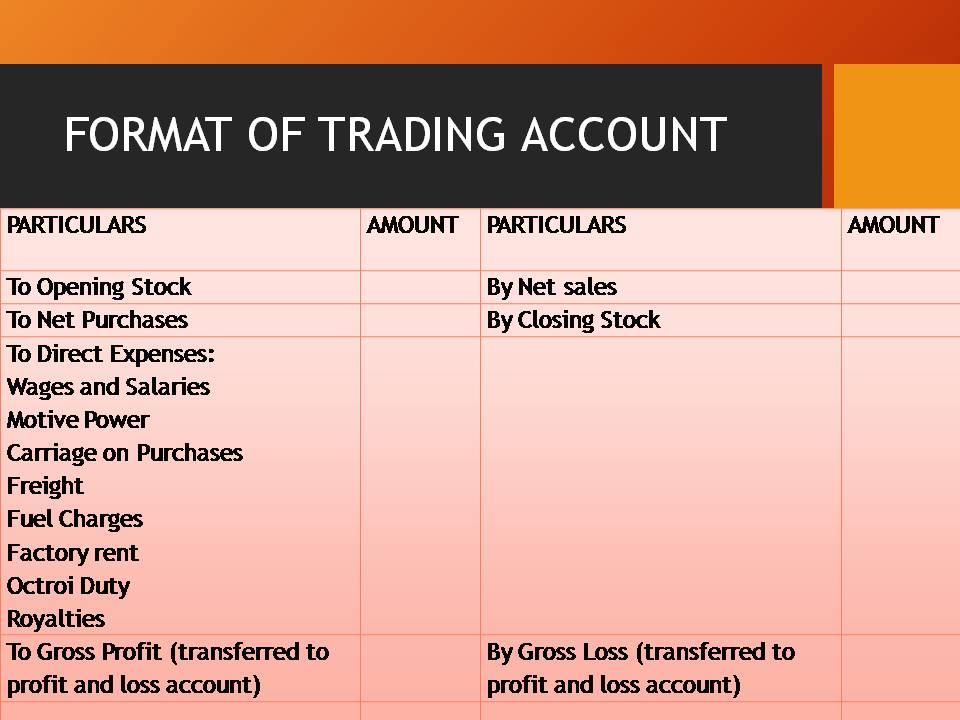

ITEMS ON DEBIT SIDE: Trading Account records the Opening Stock, Net purchases and Direct Expenses on the debit side of the account. Opening Stock is the stock with the firm at the beginning of the year. Net purchases are the purchases less returns. Direct expenses are those expenses that are directly related to the Purchase, production or Factory. Direct Expenses includes Wages and Salaries, Carriage, Freight, Octroi Duty, Fuel and power, Motive power, Factory rent etc.

ITEMS ON CREDIT SIDE: This Account records the Net sales and closing stock at the credit side of the account. Net sales are calculated by deducting the amount of returns from the sales. Closing stock is the stock remained with the firm at the end of the year. It may be called as unsold stock.

BASIS OF PREPARATION: This Account becomes a base for preparation of Profit and Loss Account. This account is a part of Profit and Loss Account and prepared before it and the gross profit or gross loss resulting out of the trading profit becomes the base for preparation of profit and loss account or Income Statement.

DETERMINE COST OF GOODS SOLD: Trading Account helps in determining the cost of goods sold. It can be calculated as:

COST OF GOODS SOLD= Opening Stock+ Net Purchases+ Direct Expenses- Closing Stock.

OR

COST OF GOODS SOLD= Net sales- Gross Profit.

FORMAT OF TRADING ACCOUNT

*Net Purchases= Purchases- Return Outwards or Purchase Return

*Net Sales= Sales – Return Inwards or Sale Return

IMPORTANCE/ ADVANTAGES OF TRADING ACCOUNT

The following are benefits or relevance of trading account:

HELPS IN DETERMINING GROSS PROFIT OR GROSS LOSS

Trading Account helps in determining Gross Profit or Gross Loss. It helps in finding out the two amounts by comparing the debit side with credit side. Increase of debit over credit results in Gross Loss and increase of credit over debit results in Gross Profit.

Debit< Credit= Gross Profit

Debit> Credit= Gross Loss

HELPS IN DETERMINING THE TRADING PERFORMANCE

Trading Account makes the records of the goods purchased and sold and also records the amount of goods unsold during the year. This helps in determining whether the company has performed better in selling goods or not i.e. the trading performance of the business.

HELPS IN CALCULATING THE COST OF GOODS SOLD

It helps in determining the cost of goods sold. It can be calculated as:

COST OF GOODS SOLD= Opening Stock+ Net Purchases+ Direct Expenses- Closing Stock.

OR

COST OF GOODS SOLD= Net sales- Gross Profit.

HELPS IN STUDYING THE TREND OF SALES

The trading account prepared for the year is compared with the trading account of the previous year. This helps in studying about the trend of sales over a period of time. The increase in sales or decrease in sales is easily captured from the trading account.

HELPS IN COMPARISON

The trading account allows the comparison of the unsold stock, amount of purchases, expenses on purchases, goods sold over a period of time. This comparison forms the basis of future planning.

HELPS IN CONTROLLING EXPENSES

The trading account records all the expenses related to the purchase, production or factory. These expenses include Factory rent, wages and salaries, power and fuel, motive power, octroi duty, carriage on purchases etc. It becomes easy to keep an eye on the unnecessary expenses by preparing this account and to control the over expenditure.

HELPS IN FORECASTING FUTURE

Trading Account gives the current view of the purchases, sales and unsold stock. By studying this, future targets can be set regarding

• Sales to be made

• Amount of goods to be purchased

• Minimum level of stock that must be maintained, etc.

PROFIT AND LOSS ACCOUNT

Profit and Loss Account is an account prepared by the trading organizations to know about the net profit or net loss of the firm. This account records all the incomes on credit side and expenses on debit side of a particular year. This account is prepared at the end of the year.

ACCORDING TO RN CARTER

“A profit and loss account is an account into which all gains and losses are collected. If the gains exceed the losses, the excess is the net profit, if the losses are greater than the gains the difference is the net loss.”

ACCORDING TO JR BATLIBOI

“The function of the profit and loss account is to enable a trader to ascertain the net profit or net loss resulting from business transactions during a given period.”

This account is prepared after the preparation of Trading Account and starts with the balance i.e. Gross Profit or Gross Loss of Trading Account.

FEATURES OF PROFIT AND LOSS ACCOUNT

The following are the features this account:

NATURE OF ACCOUNT

It is a nominal account. All the expenses are recorded on the debit side and all the incomes are recorded on the credit side. The rule applies to this account is:

“DEBIT ALL EXPENSES AND LOSSES

CREDIT ALL INCOEMES AND GAINS”

PREPARED ON ACCRUAL BASIS

This account is prepared on the accrual basis. It means all the items relating to the current year are recorded in this account. This leads to adjustments of the accrued income, income received in advance, outstanding expenses, prepaid expenses. No item related to past or next year is recorded in this account.

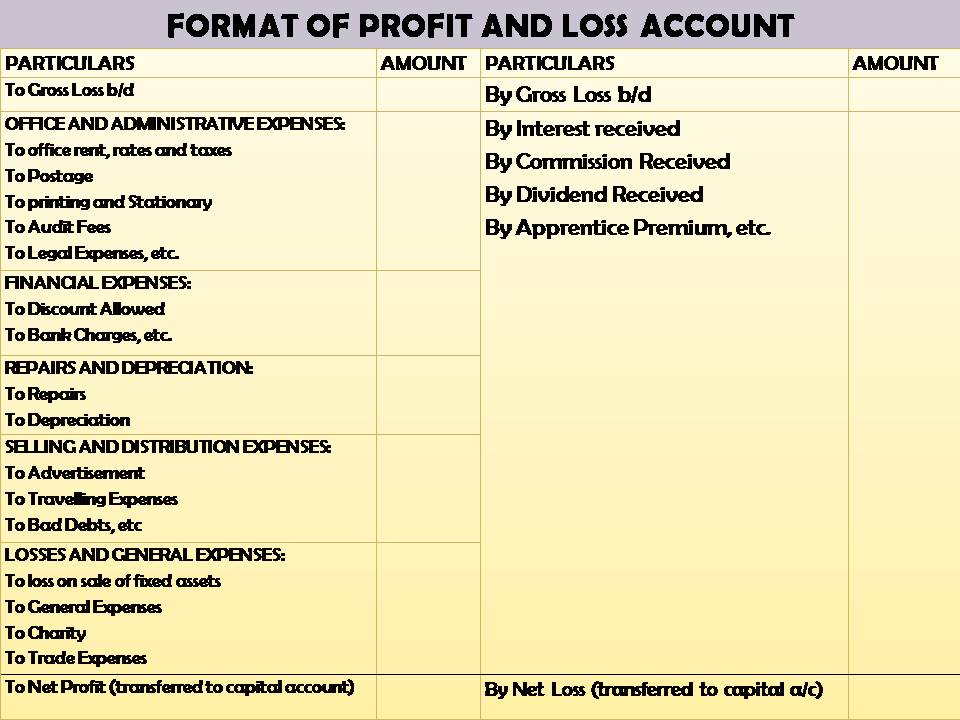

ITEMS ON DEBIT SIDE

This account records all the expenses on the debit side. The items on the debit side are divided into 5 main heads:

• Office and Administrative expenses– office rent, rates and taxes, postage, salaries etc.

• Financial Expenses– discount allowed, bank charges, interest on loan, interest on capital etc.

• Repairs and Depreciation– Depreciation and Repairs.

• Selling and Distribution Expenses– Advertisement, travelling expenses, carriage outward, commission etc.

• Losses and General Expenses– Loss on sale of fixed assets, general expenses, charity, trade expenses etc.

ITEMS ON CREDIT SIDE

This account records all the incomes of the current year on the credit side like discount received, commission received, dividend received, apprentice premium, miscellaneous receipts etc.

TIME OF PREPARATION

It is prepared at the end of the year i.e. as at 31st March, 20__. It is prepared after preparing Profit and Loss Account and before preparing Balance Sheet.

RESULT

It shows the result of Net Profit or Net Loss by comparing the both sides Debit and Credit. Increase of debit over credit results in Net Loss and increase of credit over debit results in Net Profit.

Debit< Credit= Net Profit

Debit> Credit= Net Loss

BASIS OF PREPARATION

Profit and Loss Account is prepared on the basis of Trading Account balance. The balance of trading account i.e. Gross Profit or Gross Loss serves as starting point of preparation of Profit and Loss Account.

FORMAT

IMPORTANCE/ NEED/ ADVANTAGES OF PROFIT AND LOSS ACCOUNT

KNOWLEDGE OF NET PROFIT/LOSS

The profit and loss account is prepared to find out the true net profit or net loss of the firm for a current year. The net profit or net loss is transferred to the capital item in the balance sheet. Net profit is added to capital whereas the net loss is deducted out of the capital on the liabilities side of balance sheet.

COMPARISON OF PROFITS/ TRENDS OF PROFITS

The account prepared for the current year is compared with the profit and loss account of the past years to find out the trend of the profit or losses incurred. The management analyses the trends of profits and plan accordingly for the future.

CONTROL OVER EXPENSES

This account also helps in comparing the expenses of the current year with the past years. The increase or decrease in particular kind of expenses can be ascertained and step will be taken to control the expenses of the firm.

PROVIDE PROFITABILITY POSITION OF THE CURRENT YEAR

As this account is prepared on the accrual basis and all the adjustments regarding accrued incomes, income received in advance, outstanding expenses and prepaid expenses are made in this account. So, this account shows a fair view of the profitability position of the current year.

FORECAST FUTURE PERFORMANCE

On the basis of the expenses, incomes, profits or losses disclosed of the current year, future performance can be forecasted easily.

HELPS IN DETERMINING TAX LIABILITY

The taxes are always charged on the amount of income or profits earned. The profit of the firms is ascertained by preparing this account. So this account helps in determining the tax liability of the firm.

HELPFUL IN PREPARATION OF BALANCE SHEET

The net profit or net loss disclosed by this account is posted to the balance sheet on the liabilities side. The net profit is added to the capital and net loss is deducted out of the capital. In this way, it helps in preparation of balance sheet.