WORKMEN COMPENSATION RESERVE TREATMENT ON DISSOLUTION

Workmen Compensation Reserve is a reserve created out of firm’s profits to meet possible liability to pay compensation to employees, if it arises. It means, a claim may or may not arise. It also means that claim may be higher than amount of reserve. This Reserve represented by compensation payable to workers is an external liability and the balance of amount left, if any, is an internal liability payable to partners. Workmen Compensation Reserve Treatment In Dissolution is of closing the reserve account by settling the claim and distributing the rest to partners.

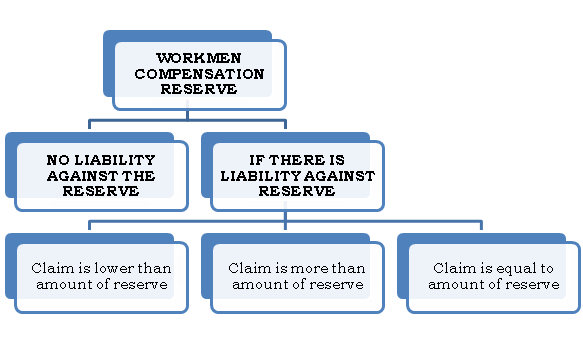

WORKMEN COMPENSATION RESERVE TREATMENT ON DISSOLUTION

IF NO LIABLITY OR CLAIM EXIST AGAINST WORKMEN COMPENSATION RESERVE

In such a case, entire amount of Workmen Compensation Reserve is transferred to the Partner’s Capital/ Current Accounts in their profit-sharing ratio.

| Workmen Compensation Reserve A/c Dr. To Old Partner’s Capital/ Current A/cs (Being the amount of Workmen Compensation Reserve credited to Partner’s Capital Accounts in their profit sharing ratio) |

IF CLAIM FOR WORKMEN COMPENSATION EXIST

In such a situation, treatment of Workmen Compensation Reserve depends on the amount of liabilities. There can be three possible situations:

If the claim is less than the amount of Workmen Compensation Reserve: The amount of estimated claim is transferred to Realisation Account and excess Workmen Reserve over the Workmen Compensation Claim is credited to partners in their profit sharing ratio. The journal passed is:

| Workmen Compensation Reserve A/c……………………………………….Dr. To Realisation A/c To partner’s Capital/ Current A/cs (Being the claim made and balance transferred to Partner’s Capital Accounts in their profit sharing ratio) |

If the claim is equal to the Workmen Compensation Reserve: Workmen Compensation Reserve is transferred to Realisation Account and no amount is left for distribution among the partners.

| Workmen Compensation Reserve A/c……………………………………………Dr. To Realisation A/c (Being paid for Workmen Compensation Claim) |

If the claim is higher than the amount of Workmen Compensation Reserve: The amount of Workmen Compensation reserve is transferred to Realisation Account.

The journal entries passed are:

| Workmen Compensation Reserve A/c……………………………………Dr. To Realisation A/c (Being the amount of claim recorded in Realisation Account) |

EXAMPLE

A and B were partners sharing profits in the ratio of 3:2. Give the journal entries for following:

CASE 1: WCR stood at ₹75,000 and there was no claim or liability towards WCR.

CASE 2: WCR stood at ₹60,000 and liability for it was ascertained at ₹35,000.

CASE 3: WCR stood at ₹60,000 and liability towards it was ascertained at ₹75,000.

CASE 4: WCR stood at ₹60,000 and liability towards it was estimated at ₹60,000.

CASE 5: No WCR is there and firm had to pay ₹15,000 as compensation to workers.

SOLUTION: CASE 1:

| WCR A/c Dr. 75,000 To X’s Capital A/c 45,000 To Y’s Capital A/c 30,000 (Being the balance of WCR transferred to Partner’s Capital Accounts in the profit sharing ratio) |

SOLUTION: CASE 2:

| WCR A/c Dr. 35,000 To Realisation A/c 35,000 (Being WCR to the extent of liability transferred to Realisation Account) |

| WCR A/c Dr. 25,000 To X’s Capital A/c 15,000 To Y’s Capital A/c 10,000 (Being surplus of WCR transferred to Partner’s Capital Accounts in their Profit Sharing Ratio) |

| Realisation A/c Dr. 35,000 To Bank A/c 35,000 (Being the liability on account of Workmen Compensation paid) |

SOLUTION: CASE 3:

| WCR A/c Dr. 60,000 To Realisation A/c 60,000 (Being balance of WCR transferred to the Realisation Account) |

| Realisation A/c Dr. 75,000 To Bank A/c 75,000 (Being the liability on account of Workmen Compensation paid) |

SOLUTION: CASE 4:

| WCR A/c Dr. 60,000 To Realisation A/c 60,000 (Being balance of WCR transferred to the Realisation Account) |

| Realisation A/c Dr. 60,000 To Bank A/c 60,000 (Being the liability on account of Workmen Compensation paid) |

SOLUTION: CASE 5:

| Realisation A/c Dr. 15,000 To Bank A/c 15,000 (Being the liability on account of Workmen Compensation paid) |