GST SUVIDHA PROVIDER

GSP stands for GST Suvidha Provider. GST Suvidha Providers are the special entities who have been authorized to develop a platform to enable the taxpayer to do the GST compliances. A GSP enables a GST taxpayer to comply with all the procedural provisions of the GST law through its web platform. A GSP provides innovative methods or means of an effective interactive platform for taxpayers to access GST portal services ranging from registration and invoicing to completion of GST return filing.

EXAMPLE

ABC Ltd is a private multinational company, which is running operations on SAP ERP. All records with respect to purchases and sales are maintained in it. At the end of each month, reports are generated from ERP and utilised to prepare and generate tax returns. Thereafter, returns are uploaded on the government’s portal.

Our government is now aiming for single and automated workflow wherein these ERP companies can build an interface with government’s portal and all the GST related compliance can be done directly through their software.

GSP need not be only ERP companies but can be startups or financial technology companies having expertise in building web applications for filing GST return.

GST SUVIDHA PROVIDER – A BRAINCHILD OF GOODS AND SERVICES TAX NETWORK

GSP is a term coined by GSTN (Goods and Service Tax Network), the private non-government entity that owns and maintains the GST portal.

It is in-line with the ‘Digital India’ initiative that advocates a paperless tax compliance regime that enables transparency and reliability in doing business across India.

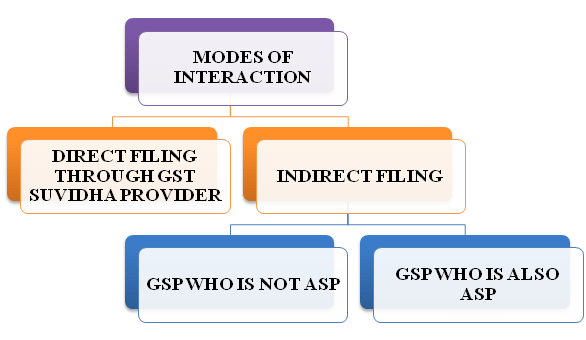

MODES OF INTERACTION WITH GST PORTAL

FILING DIRECTLY ON THE GST PORTAL

A GST taxpayer will usually access the website directly for availing various services offered on the website such as registration, GST return filing, refund application, and other similar GST compliances. However, for services such as GST return filing, a taxpayer may not be technically equipped to file online. Hence, they may find it difficult to collate sales and purchase data from his ERP system or accounting software in the required GSTN format. A lot of manual efforts may go into preparing the GST returns. Hence, a GST Suvidha Provider is an indirect means yet an easy platform to access the GST portal saving time and efforts.

FILING THROUGH INDIRECT MODES

Under indirect means, there are two types of intermediaries between the taxpayer and the GST portal. They are as follows:

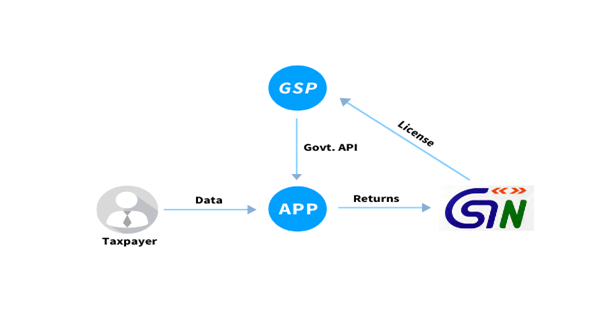

ASP who is not a GSP

These entities provide the requisite third-party applications for GST compliance. They have user interfaces via various modes such as desktop, mobile or any other interfaces for taxpayers just like any other Application Service Provider (ASP). Such an application developer can connect with the GST portal via a secure GST system Application Programming Interface (APIs) accessed with the help of GST Suvidha Providers.

The below diagram will show the two ways of how the taxpayers can access the GST portal indirectly through an ASP who is Non-GSP:

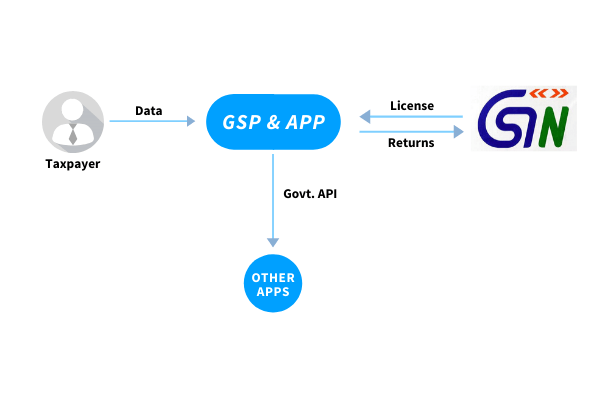

ASP who is also a GSP

A government-approved application service provider is the most reliable mode of completing GST compliances. They provide the application and are also authorised to provide an interactive platform to access the GST portal. Such an ASP who is also a GST Suvidha Provider can connect seamlessly with the GST portal and helps avoid; any third-party dependency, thereby increasing the speed of processing of data. Also, an ASP which has access to multiple GSPs will ensure higher uptime availability and scalability for the user.

The below diagram will show the two ways of how the taxpayers can access the GST portal indirectly through an ASP who is also a GSP:

Interaction of a taxpayer with the GST portal can, therefore, take place via either of the three routes as follows:

Benefits of being an ASP who is also a GSP

- Allows an end-to-end integration with any ERP system or accounting software so that data can be fetched automatically.

- Improved and faster performance compared to any other ASP not being GST Suvidha Provider.

- The integration with the GSTN can allow a smooth flow of data between the application and the GST portal avoiding any third-party dependency.

- A single login is needed to access different locations (GSTIN) instead of login and logout each time from different locations.

- Better security ensured as all security standards are met and approved by GSTN.

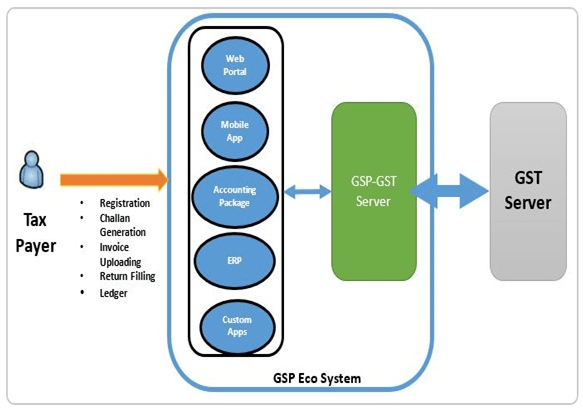

GST SUVIDHA PROVIDER (GSP) ECO-SYSTEM

GSP providers are allowed to create GST application themselves or allow third-party application developers to access the GSTN through them. Also, taxpayers are free to choose an Application Providers or GSP of his/her choice, irrespective and independent to the other. Thus a taxpayer , can choose a set of services from one GSP and the rest from other GSPs. For example, a tax payer can obtain GST registration through one GSP or ASP, while filing GST return through another GSP or ASP.

GST SUVIDHA PROVIDER (GSP) LICENSE – ELIGIBILITY CRITERIA

Companies registered in India in the Information Technology, Information Technology Enabled Services, Banking, Financial Services and Insurance sector are eligible for a GSP license. All GST Suvidha Provider applicants must meet strict eligibility criteria. GSP applicants meeting the eligibility will be required to sign a contract with GSTN to become an authorised GSP. On signing the contract, the GST Suvidha Provider is allocated an unique license key for accessing the GST system.

Eligibility Criteria: 1

The first set of GST Suvidha Providers were required to meet the following standards for obtaining GSP license:

Financial Strength

- Paid up / Raised capital of at least Rs. 5 crores and

- Average turnover of at least 10 Crores during last 3 financial years

Demonstration of Capabilities

- Invoice upload by tax payers

- GST Return #1 and #2 preparation and filing

- Reconciliation of downloaded GSTR2 with Purchase Register

- Multiple GSTIN Ids mapped to a single user account

- Multiple roles mapped to single GSTIN

- E-sign / DSC integration for signing of returns

- Mobile interface

- Alert generation to tax payers

- Security design

Technical Capabilities

- Backend infrastructure, such as servers, databases etc., required specifically for the purpose of GSP work shall be based in the territory of India, and

- IT Infrastructure owned or outsourced to carry out minimum of 1 Lakh GST transaction per month, and

- Data Privacy policy to protect beneficiary privacy, and

- Data security measures as per the IT Act.

Eligibility Criteria: 2

Following the onboarding of the first Batch of GST Suvidha Providers, the GSTN relaxed the eligibility criteria and invited the second batch. The revised eligibility criteria is as under:

Financial Strength

- Paid up / Raised capital of at least Rs. 2 crores and

- Average turnover of at least 5 Crores during last 3 financial years (2014-15, 2015-16, 2016-17)

Demonstration of Capabilities

- Invoice upload by tax payers

- GST Return #1 and #2 preparation and filing

- Reconciliation of downloaded GSTR2 with Purchase Register

- Multiple GSTIN Ids mapped to a single user account

- Multiple roles mapped to single GSTIN

- E-sign / DSC integration for signing of returns

- Mobile interface

- Alert generation to tax payers

- Security design

- Technical Capability of GSP (Handling Large Load, Experience in handling large application, Managing Sizable Application Infrastructure, Experience in developing complex application etc.)

Technical Capabilities

- Backend infrastructure, such as servers, databases etc., required specifically for the purpose of GSP work shall be based in the territory of India, and

- IT Infrastructure owned or outsourced to carry out minimum of 1 Lakh GST transaction per month, and

- Data Privacy policy to protect beneficiary privacy, and

- Data security measures as per the IT Act.

ROLE OF GST SUVIDHA PROVIDER

A variety of taxpayers including SMEs, large enterprises, micro enterprises require different kinds of facilities. The GSPs provide following services to the taxpayers to help meet the GST compliance effortlessly:

- Upload invoice data (B2B and large value B2C).

- Upload GSTR-1 (return containing supply data), which will be created based on invoice data and some other data provided by the taxpayer.

- GSTR-2A download and reconciliation with purchase data accounted on ERP.

- File GSTR-3B based on the GSTR-1 filed, purchase data on record and GSTR-2A information available.

- Similarly, there are other returns for other categories of taxpayers like casual taxpayer or composition taxpayers.

- Help in maintaining individual business ledgers including sales and purchases ledger.

QUESTION COVERED

State the meaning of GST Suvidha Provider?