Difference between Accounting Concepts and conventions

Before understanding the Difference between Accounting Concepts and Conventions, the both concepts should be known.

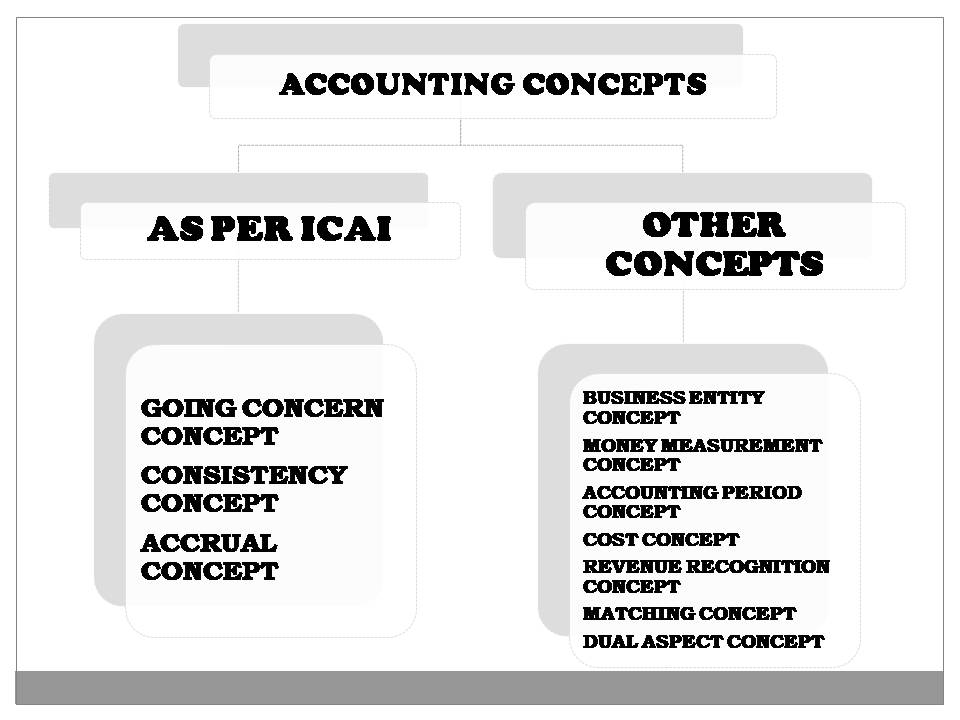

ACCOUNTING CONCEPTS

The Accounting Concepts are the foundation of the accounting. These concepts are the assumptions which are generally accepted and followed while performing the recording of transactions and preparation of final accounts. The accounting concepts help in conveying the financial information in a same meaning to the various users of the accounting. By following the concepts, one can select the appropriate methods to be used in particular situation.

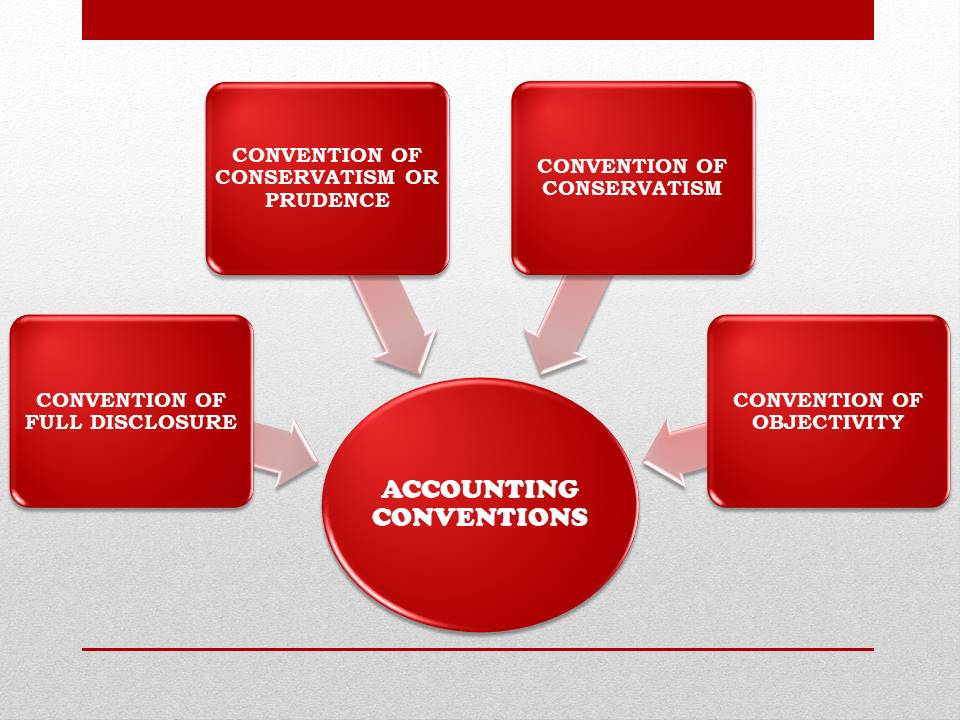

ACCOUNTING CONVENTIONS

The Accounting conventions are the guidelines based upon custom or usage or general agreement. The accounting conventions are used while maintaining the financial statements by the common consent of the accountants. In the adoption of accounting conventions, the personal judgment plays an important role. There is some kind of logic behind the usage of the conventions. Also there is no uniformity in the adoption of accounting conventions in various business enterprises.

EXAMPLE: The use of ‘TO’ on Debit side with expenses and the use of ‘BY’ on the credit side with incomes is a convention followed in India, UK and other countries but not in the USA.

DIFFERENCE BETWEEN ACCOUNTING CONCEPTS AND CONVENTIONS

| BASIS OF DIFFERENCE | ACCOUNTING CONCEPTS | ACCOUNTING CONVENTIONS |

| MEANING | Accounting concepts are the assumptions that guide how the transactions should be recorded and reported. | Accounting convention may be defined as a custom or generally accepted practice which is adopted either by general agreement or common consent among accountants. |

| LEGAL POSITION | Accounting concepts have legal acceptance. | Accounting conventions are guidelines based upon custom or usage or general agreement. |

| RECORDING VS. FINANCIAL STATEMENTS | Accounting concepts are the basic assumptions on the basis of which transactions are recorded and accounts are maintained. | Accounting conventions are followed in preparing the Profit and loss account or Income Statement and Balance sheet or Position Statement. |

| SIGNIFICANCE | Accounting concepts are uniform set of rules followed in the recording of transactions. | Accounting conventions are not so important as accounting concepts. |

| ROLE OF PERSONAL JUDGMENT | There is no role of personal judgment or individual bias in the following of accounting concepts. | Personal judgments play an important role in the adoption of accounting conventions. |

| UNIFORM ADOPTION | There is uniform adoption of accounting concepts in different business enterprises. | There is no adoption of accounting conventions in various business enterprises. |