QUESTION: Discuss important Accounting Concepts?

Accounting Concepts are the foundation of the accounting. These concepts are the assumptions which are generally accepted and followed while performing the recording of transactions and preparation of final accounts. The accounting concepts help in conveying the financial information in a same meaning to the various users of the accounting. By following the concepts, one can select the appropriate methods to be used in particular situation.

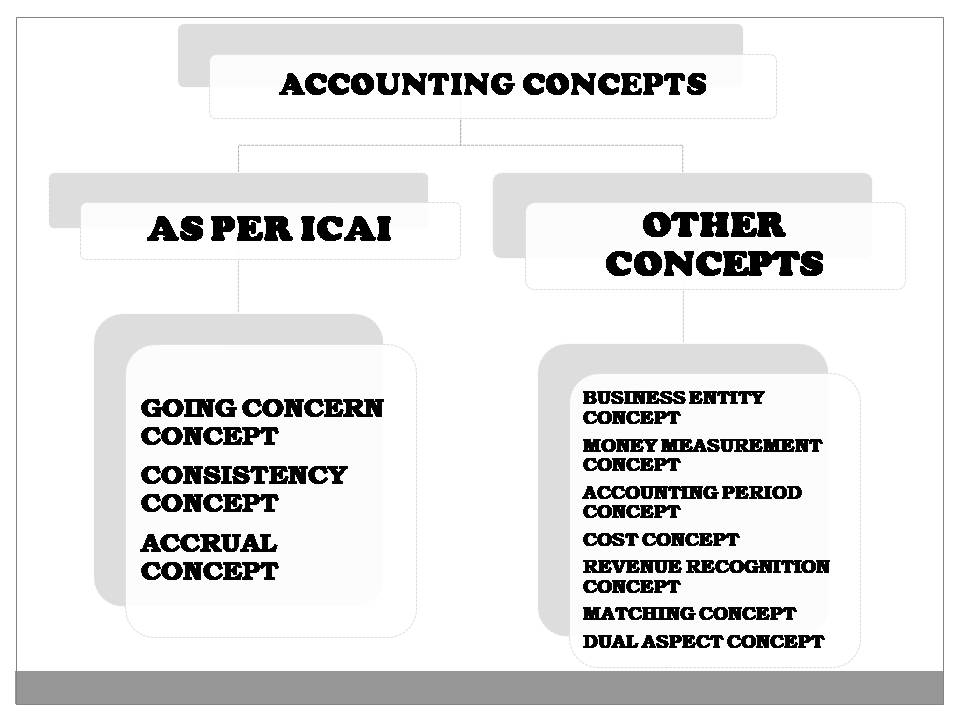

The various accounting concepts are as follows:

GOING CONCERN CONCEPT

As per this concept, it is assumed that business will continue to operate for the indefinite period of time in future. The transactions are recorded in the books of accounts assuming that the business is a continuing enterprise.

IMPLICATIONS OF GOING CONCERN CONCEPT

- Assets are to be recorded at a cost price or original price.

- Depreciation is to be provided on assets.

- Identification of short term assets or long term assets and long term liabilities or short term liabilities as different.

- Because of this concept, the outside parties enter into long term contracts with the enterprise, give loans and purchase the debentures and shares of the enterprise.

EXAMPLE: The prepaid expenses of the firm which have no realizable value are recorded in the books of accounts of the business enterprise as benefit of such expenses will be received in the future.

CONSISTENCY CONCEPT

The consistency concept states that the principles, methods and techniques of accounting should be used uniformly over the years. In simple words, the method used in one year should be applied similarly in next year and in coming future years also.

But this does not mean that the improved modes and techniques of accounting cannot be adopted. It can be adopted by the accountants provided that the changes should be communicated to the users by the way of present footnotes or explanatory notes accompanying the final accounts.

IMPLICATIONS OF CONSISTENCY CONCEPT

- The financial statements prepared for an accounting year is consistent to the financial statements prepared in the past.

- The following of this concept makes the final accounts comparable.

EXAMPLE: A firm can choose any one of the several methods of depreciation, i.e., straight line method, written down method or any other method. But it is expected that the method once chosen will be followed consistently year after year. Likewise, the method of stock valuation or make provision for likely bad debts should remain consistent with the previous years otherwise the decisions taken on the basis of accounts will be misleading.

ACCRUAL CONCEPT

Accrual concept states that all the accounting records are to maintained by taking into consideration the current year incomes and expenditures. It states that income and expenditure of a particular year is to be recorded in the book of accounts and it is immaterial whether the amount for the same is paid or received or not. It means:

- Record the income of the year whether is it received or not.

- Record the expense of the year whether it is paid or not.

IMPLICATIONS OF ACCRUAL CONCEPT

- It is similar to matching concept.

- It truly depicts the accurate profit and loss of the firm for a year.

- It gives rise to the adjustments like:

- Prepaid Expenses

- Accrued Incomes

- Income received in advance

- Outstanding Expenses

- It differentiates the cash transactions and credit transactions.

- It shows the true financial position of the concern.

EXAMPLE: Credit purchase of goods, Rent paid in advance for the next year, Interest due but not yet received.

BUSINESS ENTITY CONCEPT

According to the business entity concept, the owner and business are considered as separate entities. It states that the owner has a separate legal entity and the business house has separate legal entity. This concept is applicable to Joint Stock companies. Because of this, the personal property, personal investments, personal income and expenditure of the owner is kept out of the books of accounts of the business.

IMPLICATIONS OF BUSINESS ENTITY CONCEPT

- The books of accounts are maintained from the business point of view.

- The owner of the business is the creditor to the business.

- The capital invested by the owner is the internal liability for the business.

- The interest on capital is considered as an income for the business that increases its profits.

- The interest on drawings is considered as an expense for the business that decreases its profits.

EXAMPLE: The goods used form the stock of the business for business purposes are treated as business expenditure but similar goods use by the proprietor i.e. owner for his personal use are treated as his drawings.

MONEY MEASUREMENT CONCEPT

Money is the common denominator to measure all the transactions and events. The money measurement concept states that all those transactions are recorded in the books of accounts which can be expressed in the terms of money. In India the common money denominator is ₹ (Rupees).

It means no qualitative information should be recorded in the books of accounts. It is immaterial how important that information is.

IMPLICATIONS OF MONEY MEASUREMENT CONCEPT

- Only monetary transactions and events are recorded in the books of accounts.

- No qualitative information is recorded in the books of accounts.

EXAMPLE: The accountants will not record the strike of the employees as it is a qualitative aspect and does not involve any kind of monetary figure. However the strike of the employees hampers the production.

Similarly, the purchase of 5 chairs and a table will not be recorded in the books of accounts instead purchase of 5 chairs for ₹1,000 and a chair for ₹1,500 will be recorded.

ACCOUNTING PERIOD CONCEPT

The going concern concept states that business will continue for an indefinite period of time. The accounting period concept states that to determine the profitability, solvency and liquidity position of the firm at the regular intervals, the life of the firm should be divided into a time period of 12 months i.e. a year.

IMPLICATIONS OF ACCOUNTING PERIOD CONCEPT

- The accounts are prepared for a year starting from 1st April ending 31st March.

- The financial position can be determined at regular intervals.

HISTORICAL COST CONCEPT OR COST CONCEPT

According to this concept, the assets should be recorded at the cost of its purchase or acquisition. The cost of asset is known as Historical cost. But this does not mean that same value should be appeared again and again in the balance sheet. The value of the asset is reduced by the amount of depreciation provided.

IMPLICATIONS OF COST CONCEPT

- The asset is shown at the cost less depreciation.

- No asset is recorded if nothing is paid for it like goodwill will not be recorded in the books of accounts if nothing is paid for it.

EXAMPLE: If the cost of the machinery purchased is ₹1,00,000 and its market value is ₹1,05,000, the machinery will be recorded at the figure of ₹1,00,000 only as per the historical cost concept.

MATCHING CONCEPT

According to the matching concept, the revenues or incomes of a particular year is compared with the expenses of that particular year. For matching the costs with the revenues, the revenues should be recognized as well as costs incurred to generate these revenues should also be recognized.

IMPLICATIONS OF MATCHING CONCEPT

- Only current year incomes and expenditure is taken into account,

- The current year profitability and financial position can be ascertained with accuracy.

EXAMPLE: The incomes are matched against the expenses to find out the net profit or loss of the business.

The assets are matched against the liabilities to find out the solvency position of the business.

DUAL ASPECT CONCEPT

According to this concept, every business transaction has two aspects: DEBIT or CREDIT. It means any transaction will affect at least two accounts. The effect on two accounts will be the same.

IMPLICATIONS OF DUAL ASPECT CONCEPT

- For every Debit, there is corresponding Credit.

- The total of both sides of balance sheet should be equal.

- The system of accounting based on this concept is called ‘Double Entry system.’

- The Accounting equation followed is:

ASSETS= CAPITAL + LIABILITIES

EXAMPLE: X started business with ₹5,00,000 in cash that includes ₹1,00,000 as loan. The equation will be:

ASSETS= LIABILITIES + CAPITAL

5,00,000= 1,00,000+ 4,00,000

REVENUE RECOGNITION OR REVENUE REALISATION CONCEPT

According to this concept, the revenue is recognized when the transaction is entered into. This concept states that no anticipated revenue should be taken into account. The revenue is considered as realized when we make a sale or earned the money by giving services. It does not matter whether the money is received for the same or not.

IMPLICATIONS OF REVENUE RECOGNITION CONCEPT

- The revenue recognition concept follows the convention of conservatism.

- The accountant must not record the anticipated profits.