Question: Discuss the nature and scope of Financial Accounting?

Accounting is art of recording, classifying, summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of financial character and interpreting the results thereof. The Nature of Accounting can be defined in two ways:

- Quantitative Attributes of Accounting

- Qualitative Attributes of Accounting

QUALITATIVE ATTRIBUTES OF ACCOUNTING

The fundamental nature of financial statements is to provide true and fair view of the state of affairs and profit or loss for the period. Qualitative attributes simplifies and expands on the financial figures to ensure easy understanding and comparability of results. The Qualitative Attributes that describe the Nature of Accounting are as follows:

RELIABILITY

Reliability implies that the information must be factual and verifiable. The accounting information has said to have verifiability if such information can be verified from source documents such as cash memos, purchase invoices, sales invoices, correspondence, agreement, property deeds and other similar documents.

In order to be relied upon, the financial information requires the following attributes:

- Neutrality

- Substance over form i.e. accounting should be based on financial reality and not merely on legal form.

- Prudence

- Completeness

RELEVANCE

Accounting information depicted by financial statements must be relevant to the objectives of enterprise. Unnecessary and irrelevant information should not be included in financial statements. The INTERNATIONAL ACCOUNTING STANDADRDS BOARD (IASB) says that information is relevant “When it influences the economic decisions of users by helping them evaluate past, present or future events or confirming or correcting their past evaluations.”

The relevance of information is affected by its nature and materiality. If an item or event is material, it is probably relevant to the users of financial statements.

For Example: The information regarding the rate of dividend paid by a company in previous years is relevant information for the investors since it provides a basis for forecasting future dividends.

UNDERSTANDABILITY

Accounting information should be presented in such a simple and logical manner that they are understood easily by their users such as investors, lenders, employees etc. A person who does not have any knowledge of accounting terminology should also be able to understand them without much difficulty.

This can be done by giving relevant explanatory notes to explain the information given in financial statements. General topics which can be included in the explanatory notes are Method of depreciation, method of valuation of inventory, description of contingent liabilities, explanation of reserves, disclosure of events occurring after balance sheet date etc, These explanatory notes make the financial statements more useful and understandable.

COMPARABILITY

Comparability is very useful quality of the accounting. The financial statements should contain the figures of previous year along with the figures of current year so that the current performance can be compared with the past performance. Similarly, the financial statements should be prepared in such a way that the profitability and financial position of the concern may be compared with the other concerns of the similar type.

Comparison reveals the strong and weak points of the business entity. Comparison is possible when the different firms in the same industry adopt the same accounting principles from year to year.

For Example: If diminishing balance method of charging depreciation is selected, it should not be changed from year to year. Similarly, the method of valuation of stock should also be consistently the same from year to year.

FAITHFUL REPRESENTATION

Accounting aims at preparing those financial statements that depict the true and fair view of profitability, liquidity and solvency position of an enterprise. Application of appropriate Accounting Standards normally results in financial statements portraying true and fair view of information of an enterprise.

QUANTITATIVE ATTRIBUTES OF ACCOUNTING

The Quantitative attributes explaining Nature of Accounting are as follows:

ACCOUNTING IS AN ART AS WELL AS SCIENCE

Accounting is an Art of recording, classifying, summarizing, analyzing and interpreting the accounting records with a view to ascertain the net profit/ loss and financial position of the business.

Accounting as a Science is an organized body of knowledge that contains some underlying principles and rules that are followed while maintaining accounts. However, Accounting is not a pure science as it does not establish cause and effect relationship.

RECORDING OF FINANCIAL TRANSACTIONS ONLY

Accounting records only those transactions and events that are expressed in monetary terms or in quantitative form. For instance, the transactions like sale of goods for ₹5,000 will be recorded in the books of accounts.

However, there are so many events which are very important for business but cannot be recorded in the books of accounts because such events cannot be expressed in quantitative or monetary form. For example: Loyalty of Employees, Resignation by an able and experienced manager, Strike by employees, Quarrel between employee and employer etc. but these events have a large impact and direct bearing on the business of the firm.

RECORDING IN TERMS OF MONEY

The accounting records only those transactions which can be expressed in terms of money only. It implies that a business man will not record the purchase of 5 chairs and 5 tables, he will record the purchase of 5 chairs costing ₹2,500 and 5 tables costing ₹5,000.

Also the recording is done in the book of the journal which is the primary book of recording the transactions in the chronological order.

In small business houses, the recording of transactions is generally done in the book of Journal whereas in big business houses the recording of transactions is done in the subsidiary books such as:

- Cash Book

- Purchase Book

- Sales Book

- Purchase Return Book

- Sale Return Book

- Bills Receivable Book

- Bills Payable Book

- Journal Proper

The number of subsidiary books to be maintained depends upon the nature and size and needs or requirements of the business.

CLASSIFYING THE TRANSACTIONS

One of the Features of Accounting is that it classifies all the transactions recorded in the book of the Journal. Classification refers to grouping the transactions of same nature at one place, in a separate account. Classification of transactions is done in the books of ‘Ledger’. All the accounts related to creditors, debtors, capital, assets, liabilities, incomes and expenses are separately opened in the Ledger Book. Example: Wages Account, Ram Account, Advertisement Account, Cash Account, Bank Overdraft Account etc.

SUMMARISING THE TRANSACTIONS

Summarizing is the art of presenting the classified data in a manner which is understandable and useful to management and other users of such data. It involves:

- Balancing of Ledger Accounts

- Preparation of Trial Balance

- Preparation of Trading and Profit & Loss A/c

- Preparation of Balance Sheet

Trial Balance is a summary of all the ledger accounts and is maintained to check the arithmetical accuracy of accounts. Trading Account is prepared to find out the Gross Profit or Gross Loss while Profit & Loss Account helps in knowing Net Profit or Net Loss. Balance Sheet prepared at the end of accounting year helps in knowing the financial position of the concern. It shows the Profitability, Solvency as well as Liquidity position of the business.

ANALYSING

Analyzing is concerned with the establishment of relationship between the various items or groups of items taken from Income Statement or Balance Sheet or both. Purpose of analysis is to identify he financial strengths and weaknesses of the enterprise. It provides the base for analysis.

INTERPRETATION OF RESULTS

Another feature of accounting is interpretation of results. Interpretation of results is concerned with explaining the meaning and significance of the relationship so established by the analysis. Interpretation of results requires high degree of knowledge and skills. The accountant should answer:

- What has happened?

- Why is happened?

- What is likely to happen under specified conditions?

COMMUNICATING THE RESULTS

Accounting is so featured that it will provide the analyzed and interpreted results to its users such as Management, Employees, Creditors, Research Scholars, Debtors, Financial Institutions, Competitors, Bankers, Income Tax Authorities etc. The results are communicated by preparing final accounts, ratios, graphs, diagrams, charts, fund flow statement, cash flow statement etc.

SCOPE OF ACCOUNTING

The scope of accounting is wide and extends in business, trade, government, financial institutions, individuals and families and every other avenues.

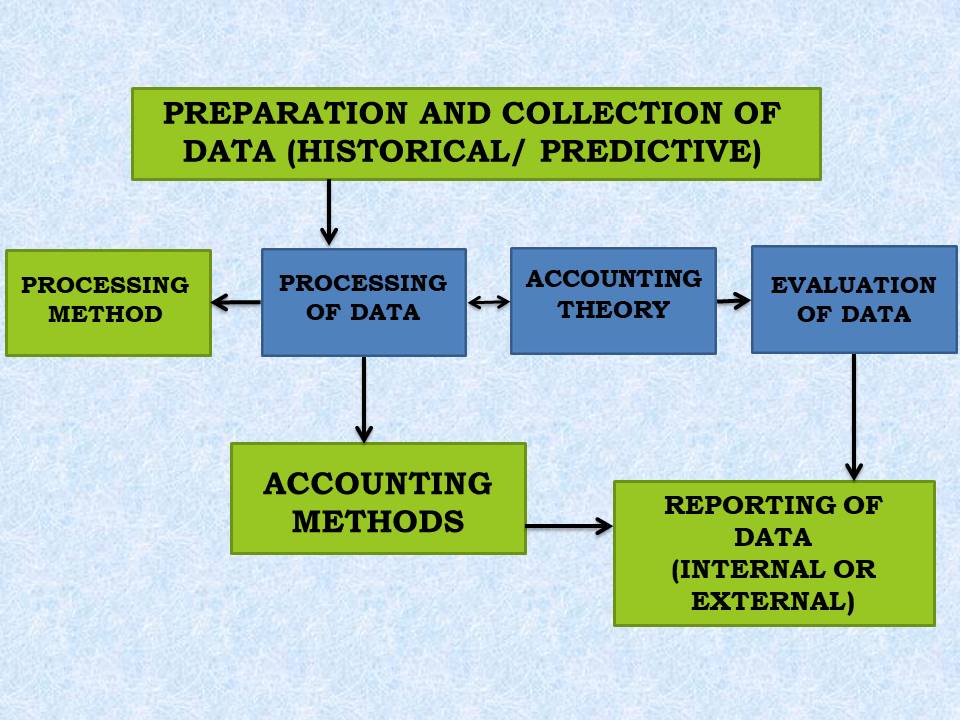

ACCORDING TO RJ BULL

The scope is as follows:

The above diagram makes it clear that accounting data is prepared and processed by using various methods of accounts. In a later stage, the report is prepared to evaluate accounting data. The report is prepared for external and internal users.

SCOPE OF ACCOUNTING IN PERSONAL LIFE

The financial transactions which occur in the individual life of a person are recorded properly in the books of accounts with a view to ascertain receipts, payments and liabilities.

SCOPE OF ACCOUNTING IN BUSINESS ORGANISATION

The accounting is rightly called ‘Language of Business’. The prime objective of business is to earn profits. Financial transactions of a business concern are recorded in the books of accounts to ascertain operating results and financial position.

SCOPE OF ACCOUNTING IN NON-TRADING OR NON-PROFIT ORGANISATIONS

Accounting has its place in non- profit organisations also. The non- profit organisations make the record of all the donations received, subscription given by members and all the expenditure. For this purpose Receipt and Payment Account, Income and Expenditure Account and Balance Sheet are prepared. All the accounts are prepared as per the rule of Accounting.

SCOPE OF ACCOUNTING IN GOVERNMENT ORGANISATIONS OFFICES

The system of accounts is prevalent in government offices, courts and state owned organisations to determine income, expenditure and proper running of administration. In the preparation of national planning and budget, accounting information is needed and reason for national progress and regress can be known through interpretation and evaluation of accounting data.

SCOPE OF ACCOUNTING FOR PROFESSIONALS

Professionals like doctors, engineers, advocates/ lawyers, actors and actresses also maintain their accounts. They maintain their accounts to keep a check on their income and expenditure and also the income tax liability is determined from the same.

CONCLUSION

From the above discussion, it is very much clear that the field of accounts are very wide and it spreads in every walk of social life. Trade and commerce are rapidly changing and developing with the changes of everything in this dynamic world. The application of accounting has achieved anew shape with the development of technology. The advancement of accounting is continuing with the multifarious development of science and technology, factory and industry and trade and commerce.