ACCOUNTING FOR INCOMPLETE VOYAGE

Voyage Accounting is done in case of Shipping Companies. To know the results of the marine business voyage accounts are prepared. It is prepared to know the profit or losses on each voyage or shipment undertaken by the shipping company. Sometimes the accounting year of shipping company has come to an end, but the voyage is still in progress. That voyage is termed as Incomplete Voyage. Accounting for Incomplete Voyage is done on the basis of matching concept. It means expenses of current year are compared with the incomes of current year. So the amount related to incomplete voyage must be carried forward to the next year.

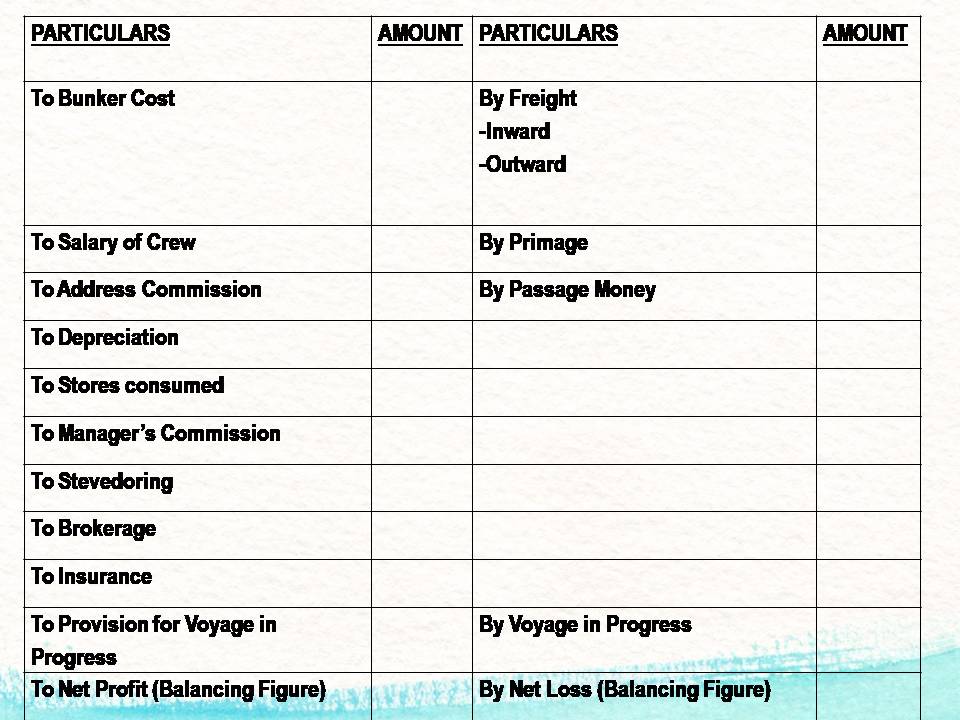

- The expenses on incomplete voyage are shown as ‘VOYAGE IN PROGRESS’ on Credit side.

- The incomes on incomplete voyage are shown as ‘PROVISION FOR VOYAGE IN PROGRESS’ on Debit side.

Under this voyage account is prepared as follows:

The description of the items is as follows:

Address commission: This is the commission which is paid to the agents who book the freight for the shipping companies. It is calculated as a percentage of freight and primage.

Address Commission= (Freight+ Primage)* Rate/100

Port Charges: The charges which are paid to the port authorities to use the port for loading and unloading the cargo from the ship.

Insurance: Expenses of premium paid to Insurance Company for the insurance of ship and freight are also debited to Voyage Account. But its premium is paid for a year. It should be adjusted according to the period of voyage.

Depreciation: Depreciation is the decrease in the value of the ship due to its use during the voyage. It is a non-cash expense and posted on the debit side of the voyage account.

Stores: Stock of store is purchased during the year for the use during the period of voyage. Stores consumed is calculated as:

(Opening stock+ Net Purchases- Closing Stock)

Stevedoring: Stevedoring are the charges of loading and unloading of the cargo on and from the ship. It is calculated usually on the unit basis. Example: If the stevedoring charges are Rs. 2 and units loaded are 1,000, then stevedoring is 10,000*2= Rs. 20,000.

Freight: Freight is the amount earned by the shipping companies on the cargo delievered. Freight is of two types:

- Freight Inward: Earned on return journey.

- Freight Outward: Earned on outgoing journey.

Primage: Primage is also known as surcharge. It is the additional freight collected as a percentage of the amount of the freight. It is calculated as:

Primage= Freight*Rate/100

Passage money: The ships also carry some passengers along with the cargo on every voyage. The amount charged from the passengers on board is known as passage money.

ASCERTAINMENT IN DIFFERENT CASES

The different cases are as follows:

CASE 1: The expenses which are related to freight, need to be carried forward in a proportion to return freight inward. It is calculated as:

(Return freight/ Total freight*Expenses)

EXAMPLE: If the freight is Rs. 25,00,000 out of which return freight is Rs. 12,00,000 and the total expenses to be 5,00,000 to be carried forward to the next accounting year, will be 2,40,000:

(12,00,000/25,00,000*5,00,000)

CASE 2: In case of standing expenses, if return journey is incomplete, ½ of the standing charges is to be carried forward.

CASE 3: In case when return journey is halfway back and the expenses of the voyage is given, ½ of total expenses is to be carried forward.

CASE 4: When the return journey is halfway back and the expenses till date are given, 1/3rd of the expenses is to be carried forward.

CASE 5: When one round of trip is complete and on his half way back for single way and total expenses of voyage are given then 1/3rd expenses are to be carried forward.

CASE 6: When one round trip is completed and on his half way back for single way and expenses till date are given then 1/5th of expenses are to be carried forward.

So, the amount of incomplete voyage is adjusted by using the above rules.

CONCLUSION

Voyage Account is specially designed for shipping companies. The voyage account is just like profit and loss account which fulfills the purpose of delivering the incomes or expenses and profit or loss of the shipping company for the particular year.