LIMITED LIABILITY PARTNERSHIP

Limited Liability Partnership enterprise has been introduced in India by enacting the Limited Liability Partnership Act, 2008. LIMITED LIABILITY PARTNERSHIP Act was notified on 31.03.2009.

A Limited Liability Partnership, popularly known as LLP combines the advantages of both the Company and Partnership into a single form of organization. Limited Liability Partnership (LLP) is a new corporate form that enables professional knowledge and entrepreneurial skill to combine, organize and operate in an innovative and proficient manner.

It provides an alternative to the traditional partnership firm with unlimited liability. By incorporating an LLP, its members can avail the benefit of limited liability and the flexibility of organizing their internal management on the basis of a mutually-arrived agreement, as is the case in a partnership firm.

SALIENT FEATURES OF LIMITED LIABILITY PARTNERSHIP

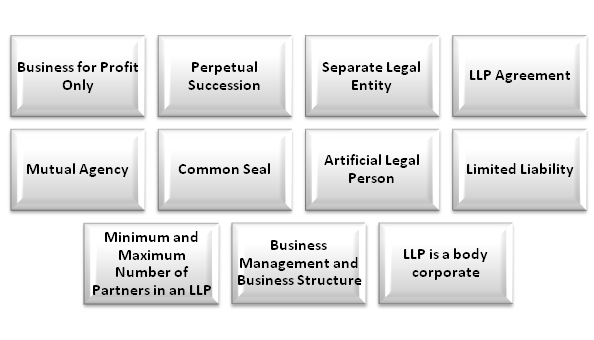

LLP is a body corporate

According to Section 3 of the Limited Liability Partnership Act (LLP Act), 2008, an LLP is a body corporate formed and incorporated under the Act. It is a legal entity separate from its partners.

Perpetual Succession

Unlike a general partnership firm, a limited liability partnership can continue its existence even after the retirement, insanity, insolvency or even death of one or more partners. Further, it can enter into contracts and hold property in its name.

Separate Legal Entity

Just like a corporation or a company, it is a separate legal entity. Further, it is completely liable for its assets. Also, the liability of the partners is limited to their contribution in the LLP. Hence, the creditors of the limited liability partnership are not the creditors of individual partners.

Mutual Agency

In an LLP independent or unauthorized actions of one partner do not make the other partners liable. All partners are agents of the LLP and the actions of one partner do not bind the others.

LIMITED LIABILITY PARTNERSHIP Agreement

The rights and duties of all partners are governed by an agreement between them. Also, the partners can devise the agreement as per their choice. If such an agreement is not made, then the Act governs the mutual rights and duties of all partners.

Artificial Legal Person

For all legal purposes, an LLP is an artificial legal person. It is created by a legal process and has all the rights of an individual. It is invisible, intangible and immortal but not fictitious since it exists.

Common Seal

If the partners decide, the LLP can have a common seal [Section 14(c)]. It is not mandatory though. However, if it decides to have a seal, then it is necessary that the seal remains under the custody of a responsible official. Further, the common seal can be affixed only in the presence of at least two designated partners of the Limited Liability Partnership.

Limited Liability

According to Section 26 of the Act, every partner is an agent of the LLP for the purpose of the business of the entity. However, he is not an agent of other partners. Further, the liability of each partner is limited to his agreed contribution in the Limited Liability Partnership. It provides liability protection to its partners.

Minimum and Maximum Number of Partners in an LLP

Every Limited Liability Partnership must have at least two partners and at least two individuals as designated partners. At any time, at least one designated partner should be resident in India. There is no maximum limit on the number of maximum partners in the entity.

Business Management and Business Structure

The partners of the Limited Liability Partnership can manage its business. However, only the designated partners are responsible for legal compliances.

Business for Profit Only

Limited Liability Partnerships cannot be formed for charitable or non-profit purposes. It is essential that the entity is formed to carry on a lawful business with a view to earning a profit.

Investigation

The power to investigate the affairs of a Limited Liability Partnership resides with the Central Government. Further, they can appoint a competent authority for the same.

Compromise or arrangement

Any compromise or arrangement like a merger or amalgamation needs to be in accordance with the Act.

Conversion into LLP

A private company, firm or an unlisted public company can convert into an LLP in accordance with the provisions of the Act.

E-filing of documents

If the entity is required to file any form/application/document, then it needs to be filed in an electronic form on the website www.mca.gov.in. Further, a partner or designated partner has to authenticate the same using an electronic or digital signature.

INCORPORATION OF LIMITED LIABILITY PARTNERSHIP

For forming an LLP, some of the important steps and matters are given below:

Partner:

There should be at least 2 persons (natural or artificial) to form an LLP. In case any Body Corporate is a partner, then he will be required to nominate any person (natural) as its nominee for the purpose of the LLP. Following entities and/or persons can become a partner in the LLP:

(a) Company incorporated in and outside India

(b) LLP incorporated in and outside India

(c) Individuals resident in and outside India.

Process of Formulation of LLP

Capital Contribution:

In case of LLP, there is no concept of any share capital, but every partner is required to contribute towards the LLP in some manner as specified in LLP agreement. The said contribution can be tangible, movable or immovable or intangible property or other benefit to the limited liability partnership, including money, promissory notes, and other agreements to contribute cash or property, and contracts for services performed or to be performed.

In case the contribution is in intangible form, the value of the same shall be certified by a practising Chartered Accountant or by a practising Cost Accountant or by approved value from the panel maintained by the Central Government. The monetary value of contribution of each partner shall be accounted for and disclosed in the accounts of the limited liability partnership in the manner as may be prescribed.

Designated Partners:

Every limited liability partnership shall have at least two designated partners to do all acts under the law who are individuals and at least one of them shall be a resident in India. ‘Designated Partner’ means a partner who is designated as such in the incorporation documents or who becomes a designated partner by and in accordance with the LLP Agreement.

In case of a limited liability partnership in which all the partners are bodies corporate or in which one or more partners are individuals and bodies corporate, at least two individuals who are partners of such limited liability partnership or nominees of such bodies corporate shall act as designated partners.

Designated Partner Identification Number (DPIN):

Every Designated Partner is required to obtain a DPIN from the Central Government. DPIN is an eight digit numeric number allotted by the Central Government in order to identify a particular partner and can be obtained by making an online application in Form 7 to Central Government and submitting the physical application along with necessary identity and Address proof of the person applying with prescribed fees.

However, if an individual already holds a DIN (Director Identification Number), the same number could be allotted as your DPIN also. For that the users while submitting Form 7 needs to fill their existing DIN No. in the application.

It is not necessary to apply Designated Partner Identification Number every time you are appointed partner in a LLP, once this number is allotted it would be used in all the LLP’s in which you will be appointed as partner.

Digital Signature Certificate:

All the forms like e Form 1, e Form 2, e Form 3 etc. which are required for the purpose of incorporating the LLP are filed electronically through the medium of Internet. Since all these forms are required to be signed by the partner of the proposed LLP and as all these forms are to be filed electronically, it is not possible to sign them manually. Therefore, for the purpose of signing these forms, at least one of the Designated Partner of the proposed LLP needs to have a Digital Signature Certificate (DSC).

The Digital Signature Certificate once obtained will be useful in filing various forms which are required to be filed during the course of existence of the LLP with the Registrar of LLP.

LLP Name:

Ideally the name of the LLP should be such which represents the business or activity intended to be carried on by the LLP. LLP should not select similar name or prohibited words.

LLP Agreement:

For forming an LLP, there should be agreement between/among the partners. The said Agreement contains name of LLP, Name of Partners and Designated Partners, Form of Contribution, Profit Sharing Ratio, and Rights and Duties of Partners.

In case no agreement is entered into, the rights and duties as prescribed under Schedule I to the LLP Act shall be applicable. It is possible to amend the LLP Agreement but every change made in the said agreement must be intimated to the Registrar of Companies.

Registered Office:

The Registered office of the LLP is the place where all correspondence related with the LLP would take place, though the LLP can also prescribe any other for the same. A registered office is required for maintaining the statutory records and books of Account of LLP. At the time of incorporation, it is necessary to submit proof of ownership or right to use the office as its registered office with the Registrar of LLP.

EXTENT OF LIMITATION OF LIABILITY OF LLP AND PARTNERS

The extent of limitation of liability of LLP and partners is as follows:

SECTION 26, LIMITED LIABILITY PARTNERSHIP ACT – PARTNER AS AN AGENT

As per this section, every partner in an LLP is an agent for the purposes of business but is not the agent of any other partner. (Section 26, Limited Liability Partnership Act, 2008)

This section segregates the liability of one partner from that of other partners. While any act of the partner would bind the LLP as a body corporate, it would not bind a partner in his individual capacity. The provisions of agency as per the Indian Contract Act (Chapter X, Section 184-220, Indian novel Act, 1872) shall be applicable, subject to Section 71 of the LLP Act (Section 71 – Application of other laws not barred: The provisions of this Act shall be in addition to, and not in derogation of, the provisions of any other law for the time being in force.)

Indian Partnership Act, also confers the role of an agent for the purpose of partnership to its partners. They too are made agents of the partnership business and not the other partners. In case of any discrepancy, the liability arising from the act of the partner shall be discharged, firstly from the firm’s assets, and if that falls short then from the erring partner’s individual assets.

SECTION 27 – EXTENT OF LIABILITY OF LIMITED LIABILITY PARTNERSHIP

This section lays down the limitation of the liabilities incurred by the partners or the LLP as a whole. They can be classified as below:

- Liability of person not authorised to act.

- Liability of LLP if partner has incurred liability due to wrongful act or omission.

- Obligations of LLP as an entity.

- Discharge of liability of LLP.

1. Liability of Person not Authorised to Act

Section 27(1)(a) provides that LLP is not bound by anything done by a partner in his dealings with a person if the partner, in fact, has no authority to do so, and the person, he is dealing with knows that he has no authority to act so or does not know him to be a partner.

This somewhat curtails the open authority given to the partners under section 26. It is important that no form of authority- express or implied is conferred upon the partner in relation to that act. If the LLP removes itself from the liability to be incurred, it will obviously have to be discharged by the partner in his individual capacity. The conditions to be satisfied for the LLP to be absolved of all liability are:

- The partner has not been conferred the authority with respect to his dealings with a person.

- The person is aware of the partner’s lack of authority.

- The person has no knowledge or does not believe the partner’s association with the LLP.

2. Liability of LLP if Partner has Incurred Liability due to Wrongful Act or Omission

Section 27(2) holds the partners and the LLP responsible if the partners incur liability of a third person by his wrongful act or omission in course of the business and in exercise of his authority. This section clearly derives its substance from Section 26 of the Indian Partnership Act which also holds the firm liable for the partner’s misconduct.

The liability, however, remains concentrated to the LLP as a whole and the erring partner and does not attach itself to other partners individually. The aggrieved party may proceed in a suit against the partner and the LLP, holding them jointly and severally liable, but may not proceed against them singly.

Since the wrongful conduct/omission was carried out by the partner in course of the LLP’s business and in exercise of his lawful authority, the ultimate liability shall fall on the LLP. In case the partner has to pay the aggrieved party from his assets, he shall be accordingly reimbursed by the firm.

For an LLP to incur liability under the Act, the following conditions must be satisfied:

- Wrongful act or omission by partner.

- Act/omission in course of LLP’s business or under LLP’s authority.

- Wrongful act/omission must incur liability of third party.

3. Obligation of LLP as a Whole

Section 27(3) provides that any liability incurred by the LLP shall be its liability as a whole and shall not confer individually upon the partners. The LLP being an independent body corporate is eligible to enter into contracts and if such contract is vitiated, the liability rests on the LLP as a whole acting through its agents, partners etc.

For instance, if the obligation is of a pecuniary nature it has to be met by the assets of the LLP and not the individual assets of the partners.

4. Discharge of LLP’s liabilities

Section 27(4) provides that the liabilities of an LLP shall be discharged from the LLP’s assets alone. This is an extension of section 27(3) which separates the liability of the LLP from that of the partners. Since an LLP is an independent entity, the liabilities incurred by it in such capacity shall be discharged from the assets of the LLP alone.

SECTION 28 – EXTENT OF LIABILITY OF PARTNERS

According to Section 28, a partner shall not be obligated as per Section 27(3) in his individual capacity merely because he’s a partner in the LLP. However, he cannot escape responsibility for any wrongful conduct done in his individual capacity, outside the ambit of his lawful authority.

Furthermore, the LLP and the partner are jointly and severally liable under section 27(2), since the wrongful act done by partner was originally commissioned by the LLP, making it responsible for any loss.

The LLP can be help responsible for any loss suffered by the counterparty and both LLP and the partner can be held liable for any misdeed done by partner in the course of business-but in no event can the liability be shifted on to other partners of the LLP, the burden has to be borne by the individual partners/LLP or both but not by the other partners who had nothing to do with the act.

SECTION 29 – HOLDING OUT

Section 29 lays down that any person who holds out, or allows himself to be held out as a partner of an LLP shall be held liable to the person who on faith of such representation gives credit to the LLP. This means that the partner holding out shall be bound by estoppel and prevented from escaping the liability incurred on account of any financial aid received by him or the LLP.

This makes the LLP bound to the third party to the extent of the financial benefits received by them. But, that is the only liability which binds the partner by holding out and the LLP, the estoppel does not operate in a way which makes the partner by holding out partake in the LLP’s business activities. It’s only the rule of estoppel that binds the partner by holding out.

SECTION 30 – UNLIMITED LIABILITY IN CASE OF FRAUD

Section 30 is an exception to the principle of limited liability since it imposes unlimited liability on its partners and the LLP if,

- LLP intends to defraud its creditors

- LLP is made to carry on fraudulent activities.

In such a scenario the liability of all the partners is unlimited for all or any other debts of the LLP. But even in such an event the personal assets of the partners are not to be exhausted to fulfil such other debts, but the liability extends only to the extent of the fraudulent activity carried out.

The LLP can escape liability if it establishes that the fraud was carried out by the partners without the LLP’s knowledge. This would absolve the LLP of all liability and only the partner will be held liable for the fraudulent activity. Any such activity being carried out shall be punishable with imprisonment for two years and a fine. It is the responsibility of the LLP and the partner to reimburse the third party against any damages caused due to such activity.

SECTION 31 – WHISTLE BLOWING

This section provides reprieve (postponement or delay) from the imposition of fine or imprisonment on the partner if such partner decides to come forward and contribute valuable information about the fraud committed against which the investigation is being conducted leading to conviction of the guilty party. No partner or employee of any LLP may be discharged, demoted, suspended, threatened, harassed or in any other manner discriminated against the terms and conditions of his limited liability partnership or employment. This section, therefore tries to bring forth the fraudulent activity as expeditiously as possible.

CONCLUSION

The liability imposed on the partners and the LLP is mostly joint and several. The extent of such liability is determined by the nature of activities carried out by the LLP and the partners. Fraudulent activities would give rise to unlimited liability and punishment and fines. However, informing the investigating authority of the misdeeds of the company would absolve that partner of any liability and also protect his stature in the LLP.